Cash management bills are short-term borrowings that the government raises as an instrument to manage liquidity. It provides for a temporary adjustment of mismatches in government cash flows. They do not follow a fixed schedule like treasury bills. Instead, it is issued by the Reserve Bank Of India (RBI) as and when needed. The maturity period for cash management bills is comparatively less than that of treasury bills; hence, they are preferred for immediate adjustments in cash flow. The minimum investment order value is ₹10,000, multiples of ₹10,000 thereafter. The settlement of CMBs occurs on a T+1 basis.

Cash management bills are generally for the short-term financial needs of the governments and do not raise long-term debt. Using these instruments, the government finances itself for a short period, usually less than 91 days. Borrowing through cash management bills guarantees that the government would meet its liabilities while ensuring fiscal stability.

What is Cash Management Bills?

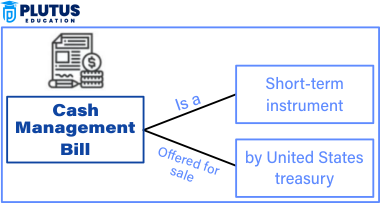

Cash management bills are short-term debt instruments issued by the central bank on behalf of the government to resolve short-term mismatches in cash flow. The maturity period of cash management bills is lesser than that of treasury bills, usually for a few weeks. Cash management bills are issued depending on the government’s financial requirements and are not scheduled like the regular treasury bills.

Cash management bills are issued at a discount and redeemed at face value. Thus, investors buy them for less than their worth and return the total amount on maturity. Therefore, the interest earned differs between the purchase price and redemption value.

Cash Management Bills: Key Highlights

Cash management bills issued by the Reserve Bank of India (RBI) in India are used to Manage Short-Term Liquid Cash. Cash management bills have a maturity of Fewer than 91 days. Cash management bills have a Minimum amount of Rs. 1 lakh

| Feature | Details |

| Cash management bills issued by | Reserve Bank of India (RBI) |

| Cash management bills in India | Used to manage short-term liquidity |

| Cash management bills have a maturity of | Less than 91 days |

| Cash management bills a minimum amount | Rs. 1 lakh |

Cash Management Bills Examples

Cash management bills are then issued depending on immediate financial necessities. The following explains the functioning of cash management bills: Assume that the Indian government needs Rs. 5,000 crore for some unforeseen expense. Instead of long-term securities, it directs the RBI to issue cash management bills. The RBI conducts auctioning where banks and financial institutions bid. The highest bidders receive the bills at a discounted rate. The government then repays this amount plus interest within about 30-50 days, ensuring smooth cash flow management for the government.

How Cash Management Bills Work?

The RBI conducts an auction to issue cash management bills.

Cash management bill auctions in India are conducted using a competitive bidding format. The RBI would issue these bills depending on the government’s financial needs. Investors who buy these bills could be banks, finance companies, or even big corporations. They are liquid because they are backed by the government, making them very safe investments.

- Systematic procedure: Announcement: Given the government’s requirements, the RBI announces the issue of cash management bills.

- Auction: Competitive bidding is involved in the auction of the bills. Banks and financial institutions submit bids.

- Discounted purchase: Investors buy the bills at a discount to their face value.

- Maturity and redemption: On maturity, the government pays the full face value to the investors.

- Calculation of interest: The gain made by the investor is said to be the difference between the purchase price and face value.

Features of Cash Management Bills

While we restrict ourselves to these Cash Management Bills, they will primarily be held by banks, mutual funds, and large companies. Their very high minimum investment makes them an unattractive proposition for retail investors. One can note some specific characteristics that differentiate Cash Management Bills from other financial instruments:

Short maturity

Cash Management Bills generally mature in less than 91 days to make these government securities the shortest maturity. Their short tenure allows the government to raise quick funds and ensures guaranteed liquidity without long-term commitments.

Issue at Discount

It is bought for less than its face value. It does not carry any explicit interest rate. The difference between purchase and redemption value is for the investor’s earnings.

Unlike treasury bills, which are scheduled for issuance at a particular time, the government issues cash management bills whenever there is a specific and urgent need for funds.

Backed by Government

Bills would be considered riskless because, while issuing bills, the RBI does it on behalf of the government. Sovereign backing would make it a highly secured investment option for institutional investors.

Liquidity- High

These bills have a very short maturity period, providing efficient liquidity and forming the best investment option for financial institutions seeking rapid retrieval. Cash management bills are allotted through competitive auctions that assure transparency in pricing and market-driven yield determination.

Fill Funding Gap

The government has used the bills as a temporary solution for short-term financial gaps and is not employed as a long-term borrowing option. Cash management bills are the most efficient instruments in temporary cash flow mismatch management, acting significantly on the state’s capacity to fund obligations without affecting the long-term fiscal strategy.

History of Cash Management Bills in India

The definition brought cash management bills in India for the government to manage the short-term liquidity gap. The first cash management bills were issued by the RBI in 2010. Before this, the government relied only on Treasury bills issued in fixed periods and lacked flexibility regarding short-term requirements.

Over the years, cash management bills have played an important role in fiscal planning. They are used, therefore, by the Indian government to facilitate the smooth flow of cash without impacting the longer-term budgetary structure. Hence, cash management bills offer a flexible borrowing instrument that does not disrupt the functioning of financial markets.

Cash Management Bills vs Treasury Bills

Cash management bills and treasury bills are the same in many respects. However, they differ in some aspects, as indicated in the below table. Treasury bills are regularly borrowed from the government, while cash management bills offer the government ignorance in urgent liquidity. Both are used to maintain financial stability but serve different purposes.

| Feature | Cash Management Bills | Treasury Bills |

| Maturity Period | Less than 91 days | 91, 182, and 364 days |

| Issuance Frequency | As per need | Fixed schedule |

| Purpose | Temporary cash management | Regular government funding |

| Discounted Rate | Market-driven | Pre-determined |

| Risk Factor | Low (government-backed) | Low (government-backed) |

Cash Management Bills FAQs

1. Who issues cash management bills?

The Reserve Bank of India (RBI) issues cash management bills for the Government of India. The RBI decides on the issuance of the bills according to the government’s short-term requirement for cash.

2. What is the minimum investment amount in cash management bills?

The minimum amount in cash management bills starts at Rs. 1 lakh. The investors may bid in multiples of Rs. 1 lakh, participating in auctions held by the RBI.

3. What is the maturity period of cash management bills?

Cash management bills have a maturity period of less than 91 days. Maturity is usually within 30-50 days, depending on the government’s cash requirement.

4. What are the differences between cash management and treasury bills?

Cash management bills are meant for short-term liquidity, while treasury bills are issued to meet longer-term cash needs. While treasury bills follow a consistent issuing timetable, cash management bills are issued only when needed.

5. Can retail investors invest in cash management bills?

Banks and financial institutions mainly subscribe to cash management bills; high-net-worth individuals and corporate investors can participate in auctions through their banks.