Commercial banks play a pivotal role in modern economies by facilitating financial intermediation between savers and borrowers. These banks accept deposits, provide loans, and offer a range of financial services, thereby fueling economic activities and supporting trade, investment, and consumption. They operate under strict regulations, ensuring the safety of deposits and maintaining economic stability. Modern commercial banks have embraced technological advancements, offering online banking, mobile apps, and digital payment solutions. Their functions extend beyond financial transactions to include wealth management, foreign exchange services, and economic advisory, making them integral to personal and corporate financial planning.

Commercial Bank Meaning

Commercial banks are financial institutions that make up the heart of modern economies by providing important financial services to individuals, businesses, and governments. The commercial bank’s meaning lies in its main role as accepting deposits from the public and offering loans to facilitate economic activity. These banks offer payment processing, wealth management, and advisory services. They connect the savers to the borrowers and thus stimulate the formation of capital as well as liquidity flows in the market. Investment banks differ from commercial banks in that they have added emphasis on securities and capital markets. Commercial banks offer regular, everyday banking services to people and businesses. They work in a heavily controlled manner as it is about protecting public deposits and overall financial stability.

Functions of Commercial Banks

The functions of a commercial bank include primary and secondary kinds. These form the twin supporting pillars to undergird economic activities. These functions also lead to economic stability. Of greater interest is that these functions enhance economic growth through the activity in trade, entrepreneurship, and resource allocation. This means banks are enablers of the utilization of capital by savers and borrowers. These have as an ultimate objective, efficient use of capital. Banks in an attempt to offer their monetary system stability functions come as providers of a critical service that helps establish credits by creating liquidity.

Principal Functions

The principal functions of commercial banks form the foundation of their operations. These include mobilizing deposits, granting loans, and creating credit, which directly fuel economic growth and ensure the efficient allocation of resources.

- Accumulation of Deposits: Commercial banks attract savings through providing various deposit accounts to various customers:

- Saving Deposits: This encourages saving for persons earning some interest therefrom, hence enriching the savings culture.

- Checking Deposits: This is a deposit for business institutions that require ample liquidity to allow their operating system.

- Time Deposits: These are offered at a higher rate to encourage people and corporations to block funds for longer periods.

Aggregating deposits, banks garner significant amounts of money that can be utilized productively.

- Loans: Banks provide loans to cater to various financial requirements of different industries. Loans are availed in several forms:

- Personal Loans: It is used to meet emergencies, education, or personal expenses to enhance living standards.

- Business Loans: Support expansion, enabling companies to buy inventories, buy equipment, or expand operations.

- Agricultural Loans: Support the rural sector through financing farming and other rural development activities.

In this way, banks directly energize economic activity, encourage entrepreneurship, and create jobs.

- Creating Credit: Commercial banks expand the economy by granting credit. They lend more than the deposits received from them, but they leave a small portion as a reserve. This boosts the money supply in the economy. The process raises the purchasing power of the people, promotes investment, and stimulates economic growth.

Secondary Functions

Secondary functions complement the primary roles of commercial banks, enhancing customer convenience and supporting financial systems. These include offering agency services, general utility services, and investment options to cater to diverse financial needs.

- Agency Services: Commercial banks offer other basic services that make the management of their customers’ finances much easier:

- Receipt of dunning, dividends, and insurance premiums

- Utility collection on behalf of account holders such as electricity, water,r and gas bills, and subscription services.

These services enable customers to save time and have convenience with respect to which results in strengthening confidence in the banking system.

- General Utility Services: The following high-values utilities, are provided by the banks to improve customer satisfaction and assistance in international trade:

- Safe deposit lockers for safe storage of valuable items

- Letter of credit and traveler’s cheque for cash transactions.

- Foreign exchange services to enable international trade and travel.

- Investment Services: Banks make sure that reserves are used appropriately by investing their excess in government securities and other low-risk instruments. These investments generate income for the banks, ensure liquidity, and contribute to the national financial stability.

These comprehensive functions make commercial banks financial lifelines that ensure smooth economic operations and promote inclusive growth. They create a secure financial environment where individuals and businesses can thrive.

Role of Commercial Banks

Commercial banks are organizations that, in addition to traditional banking, play an extremely central role in their work. They catalyze growth in economics, social advancement, and financial security. In so many ways, they are involved in activities that benefit people, business houses, and the government through a vibrant structure of sustainable development. On a country’s road to development, commercial banks offer very vital services and support in financial access. It is important to note that commercial banks and investment banks differ, as the former focuses on deposit-taking and lending, while the latter specializes in securities, capital markets, and large-scale investments.

Economic Growth

Commercial banks are vital drivers of economic growth by mobilizing savings and channeling funds into productive investments. They support industries, infrastructure, and entrepreneurship, creating jobs and fostering innovation to enhance national prosperity.

- Capital Mobilization: Industrial banks absorb surplus savings and re-allocate to productive investment in the form of fund transfer towards industries, agricultural, and infrastructural sectors, thus ensuring rational utilization of capital and promoting a moving economy. Banks form long-term growth on large-scale construction of roads and bridges and constructing energy plants.

- Empowering trade and commerce: Banks permit the provision of basic credit facilities such as cash credit, overdraft, and trade finance that enable a business to run efficiently. Such credit facilities maintain continued access of enterprises to working capital and thus help in promoting trade and maintaining the circulation of goods and services in an economy.

- Promoting Entrepreneurship: Commercial banks facilitate innovation and job creation as they provide financing for new firms and small companies. Therefore, the ideas of entrepreneurs will become a sustainable enterprise, and this is an inducement toward diversification of the economy and employment opportunities.

Monetary Stability

Commercial banks ensure monetary stability by regulating money supply and maintaining liquidity in the economy. Through credit control mechanisms and compliance with central bank policies, they help curb inflation and stabilize economic fluctuations.

- Control of Money Stock: The most critical function of regulating liquidity is carried out by the banks through repo rates, statutory reserve requirements, and open market operations. In doing this, they stabilize inflation, check economic overheating, and regulate balanced monetary flow.

- Payment Systems: Banks provide sound and secure transaction platforms, from cheque clearing to the more modern forms of digital payment. Such forms of payment permit the reduction in cash dependency with greater transparency; they have, therefore, formed a more formal economy for more financial integrity and betterment.

Promoting Social welfare

Commercial banks contribute to social welfare by enhancing financial inclusion and offering accessible banking services in underserved areas. They promote savings, support community development, and engage in corporate social responsibility initiatives for education, health, and sustainability.

- Social Welfare and Financial Inclusion: Thus, opening up the marginalized areas through branch and zero-balance account services allows the unbanked population to join its fold. It makes them empowered through the facility to save and invest as well as engage them in all types of economic activities.

- Corporate Social Responsibility (CSR): Commercial banks have been very aggressive with CSR initiatives through financing programs on education, health, environmental sustainability, and rural development. This increases living standards while promoting holistic growth in society.

- Promotion of Savings and Investment: Commercial banks encourage saving through the culture developed and provide safe options for investment by offering interest rates. This contributes to wealth creation among individuals as well as bank resources for investment in the economy.

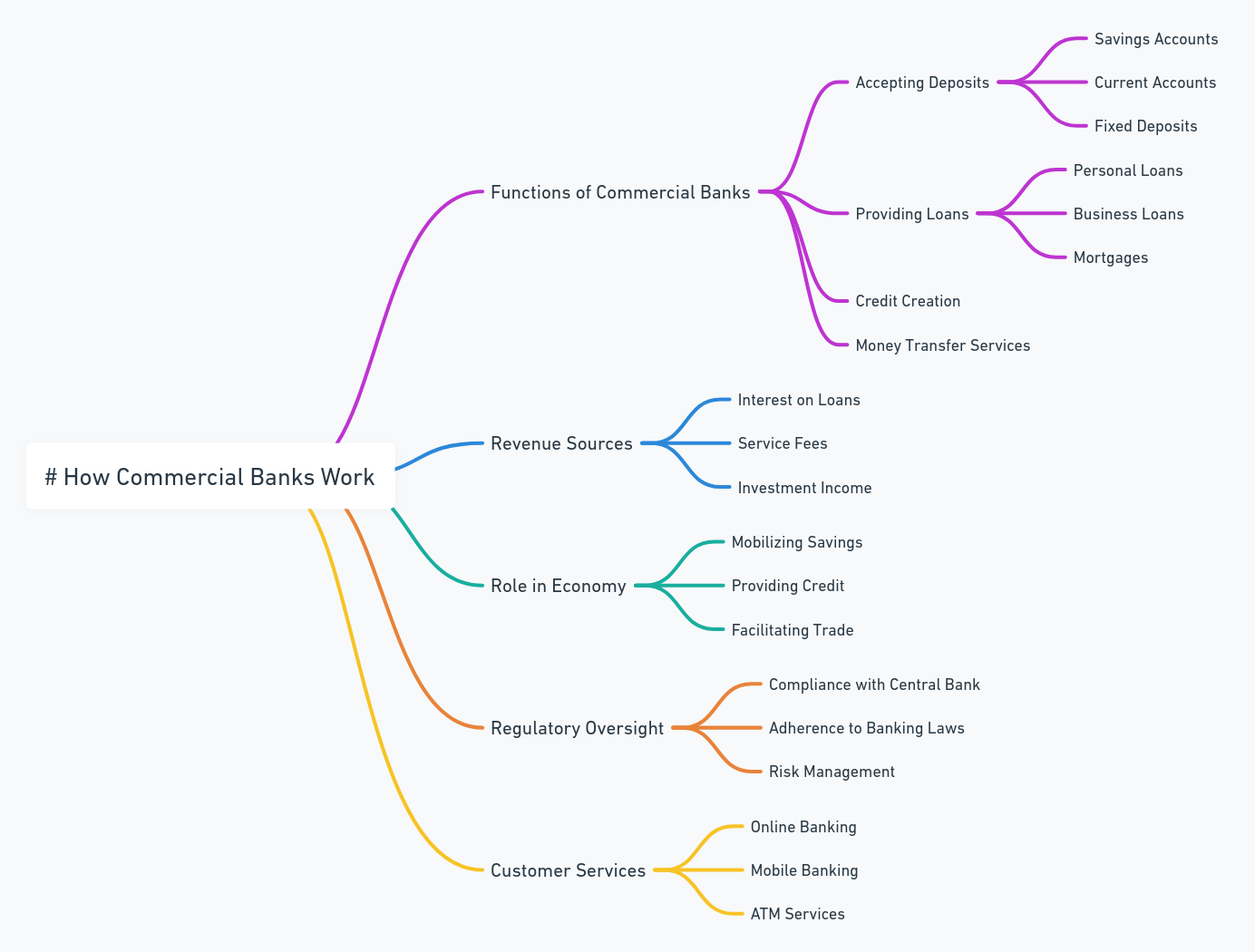

How Do Commercial Banks Work?

Commercial banks play a critical role in the financial sector because they facilitate the allocation of resources, which positively affects economic growth. They link the saver to the borrower, increase investment, and ensure liquidity, thus offering a stable business and individual environment. These operations involve mobilizing deposits, lending, credit creation, and other financial services regulated by law and supervised by central banks for the lawfulness and provision of security for finances. However, commercial banks face limitations such as dependency on economic conditions, exposure to credit risk, and restricted reach in rural or underserved areas.

Deposit Mobilization

Commercial banks encourage depositors to save and deposit money by providing different account options for depositors’ requirements.

- Savings Accounts: A savings account, where the account holder saves his money while earning interest. Example: a savings account where an individual deposits ₹10,000 monthly with an annual interest of 4%.

- Current Accounts: Current accounts suit businesses that have high turnover volumes. For example, a trader deposits ₹50,000 per day in a current account for carrying out business expense management.

- FDs: This gives relatively higher interest rates with a fixed tenure for locking up the funds. For instance, a person has invested ₹1,00,000 in a one-year FD which will earn ₹7,000 at the end of the maturity date.

By putting all these deposits together, banks have prepared a good corpus for their lending business as well as securing the deposited money.

Lending

The money put in banks is used to disburse loans which are disbursed after checking the creditworthiness of the person borrowing.

Example: A person takes a loan of ₹5,00,000 for higher education, to be repaid in monthly installments for five years.

- Business Loans: A small business owner borrows ₹10,00,000 to buy new machinery to expand the business and increase its production.

- Mortgages: A person buys a house for ₹40,00,000 through a home loan that would be repaid over 20 years, securing housing for an extended period.

For example, banks earn income by charging interest on these loans, 10% on a personal loan, but pay a lesser rate of interest on deposits, thus earning a net interest margin that is vital for their profitability.

Credit Creation

Credit creation is one other feature of commercial banks that enhances the money supply of the economy.

- For instance: Suppose a bank gets ₹1,00,000 in deposits and it has to keep 10% of it in reserve with the central bank. Then that bank will hold ₹10,000 as reserve and lend ₹90,000. Now if that ₹90,000 deposited by this other party is lodged back into the banking system, then this particular bank can lend 90% of it, namely ₹81,000, after keeping reserves.

- This cycle continues to multiply the money supply while keeping enough reserves.

- This process encourages investment, increases purchasing power, and accelerates economic growth.

Commercial Bank FAQs

What is the commercial bank meaning?

A commercial bank is a financial institution that accepts deposits, provides loans, and offers financial services to support commerce and trade.

How do commercial banks contribute to economic growth?

By mobilizing savings, granting loans, and creating credit, commercial banks fund industrial and business growth, leading to economic development.

What are the main functions of commercial banks?

The main functions of commercial banks are accepting deposits, providing loans, and creating credit. Utility and agency services are secondary functions.

Why are commercial banks important for individuals?

They provide safe deposit facilities, easy access to credit, and convenient payment systems, which simplify financial management for individuals.

What is the difference between commercial banks and investment banks?

Commercial banks differ from investment banks in that the former deal with day-to-day banking needs, while the latter deal with securities and capital markets.