Commercial banks play a pivotal role in modern economies by facilitating financial intermediation between savers and borrowers. These banks accept deposits, provide loans, and offer a range of financial services, thereby fueling economic activities and supporting trade, investment, and consumption. They operate under strict regulations, ensuring the safety of deposits and maintaining economic stability. Modern commercial banks have embraced technological advancements, offering online banking, mobile apps, and digital payment solutions. Their functions extend beyond financial transactions to include wealth management, foreign exchange services, and economic advisory, making them integral to personal and corporate financial planning.

Commercial Bank Meaning

Commercial banks are financial institutions that make up the heart of modern economies by providing important financial services to individuals, businesses, and governments. The commercial bank’s meaning lies in its main role of accepting deposits from the public and offering loans to facilitate economic activity. These banks offer payment processing, wealth management, and advisory services. They connect the savers to the borrowers and thus stimulate the formation of capital as well as liquidity flows in the market. Investment banks differ from commercial banks in that they have added emphasis on securities and capital markets. Commercial banks offer regular, everyday banking services to people and businesses. They work in a heavily controlled manner as it is about protecting public deposits and overall financial stability.

History of Commercial Banks in India

Commercial banks in India have their roots in the British era. The history of commercial banks goes way back to when the British were in India. It was in this period that banks were established which eventually paved the way for modern banking in India.

Origin and Growth of Commercial Banks in India

The journey of commercial banking in India began with the establishment of the Bank of Hindustan in 1770. After this, the Presidency Banks, that is, the Bank of Bengal, the Bank of Bombay, and the Bank of Madras came into existence during the early years of the 19th century. The clients for these banks were primarily European enterprises and government departments.

Presidency Banks merged to become the Imperial Bank of India in 1921 and later, in 1955, was amalgamated with the State Bank of India. RBI was established in 1935 as an apex banking control and regulatory institution with guidelines for the orderly development of commercial banking. In post-independence India, in 1969, 14 major banks were nationalized by the government to bring banking nearer to the common man, and a further six in 1980. Like this, we could see the growth of commercial banks in India.

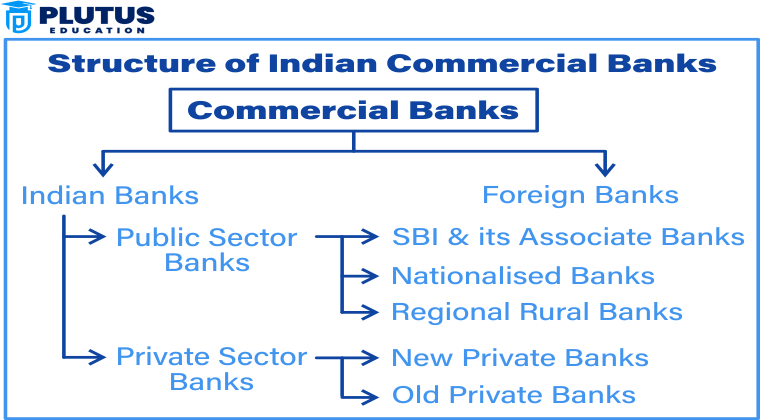

Structure of Commercial Banks in India

Commercial banks provide the backbone for the Indian financial system, which comprises structures through which commercial banks are accessible to the citizens to serve the diversified needs of society concerning financial demands. As there is their planned arrangement and specific functions enable them to reach different segments of the economy from the leading urban companies to the poor rural farm owners. Following are some detailed discussion about the categories of commercial banks in India, their functions, and examples:

Scheduled Commercial Banks in India

Scheduled commercial banks are those types of banks enlisted in the Second Schedule of the Reserve Bank of India Act, of 1934. To achieve scheduled bank status, banks have to pass through various stringent tests like reserve requirements and observance of RBI rules and regulations. In return, scheduled banks benefit through, among others, financial support from RBI and clear settlement through clearing houses. These are the largest numbers of institutions in India’s banking network and therefore hold a central place in development programs.

Types of Scheduled Commercial Banks in India

Scheduled commercial banks can be broadly classified into the following:

- Public Sector Banks: Public sector banks are financial institutions where the majority of the government holding is more than 50%. Such institutions are very much focused on public interest in order to ensure financial inclusion besides supporting the Government’s very many initiatives. They constitute the largest component of the Indian banking industry in terms of outreach, branch distribution, and customer base.

Key Features of Public Sector Banks:-

- Ownership: The government holds the majority stake.

- Objectives: They prefer to serve the public and support the economic development process rather than striving for profit maximization.

- Availability: Their healthy network allows them to stretch the banking facilities up to rural and semi-urban areas.

- Activities: They endorse government projects such as Jan Dhan Yojana, Mudra Loans, and rural credit facilities.

- Private Sector Banks: Private sector banks are owned and operated privately and controlled by private persons or shareholders. The private sector focuses on innovation, customer satisfaction, and profitability. They have provided modern banking techniques in India such as digital banking, mobile applications, and products that are customer-centric.

Characteristics of Private Sector Banks:-

- Ownership: Private sector banks are owned by private individuals or shareholders.

- Techno-enabled: The private sector uses the latest and most modern technology that can give faster, quicker, and more efficient services to customers.

- Profit-oriented: Private sector banks pursue high profitability and work efficiently in managing operations.

- Customer Service: This sector is preferred for its excellent personal services as well as time-efficient grievance redressal.

- Foreign Banks: Foreign banks are international banks operating their branches in India and offering multiple services related to finance for enterprises and individuals. Generally, they offer services to multinational companies, high-net-worth individuals, and specialized financial services.

Critical Features of Foreign Banks:-

- Global Banking Expertise: They have global banking practice and expertise experience in India.

- Specialized Services: Trade finance, treasury services, and corporate banking.

- Limited Networks: They have a network mainly in big metropolitan cities.

- Regulation: RBI monitors their operations strictly to ensure conformity with the Indian legal framework.

- Regional Rural Banks: Regional Rural Banks were formed to meet rural areas’ financial needs; that is, agricultural and small-scale industries. It is sponsored by joint investments of the central government, state governments, and the sponsoring public sector banks.

Key Features of Regional Rural Banks:-

- Ownership: Government with public sector bank ownership pattern.

- Target Group: Reaches out to farmers, small-scale entrepreneurs, and rural families.

- Tailor-made Service Delivery: crop loaning services, saving accounts, microfinance.

- Developmental Role: They play an extremely important role in the development of rural economies due to financial inclusion.

Functions of Commercial Banks

The functions of a commercial bank include primary and secondary kinds. These form the twin supporting pillars to undergird economic activities. These functions also lead to economic stability. Of greater interest is that these functions enhance economic growth through the activity in trade, entrepreneurship, and resource allocation. This means banks are enablers of the utilization of capital by savers and borrowers. These have as an ultimate objective, efficient use of capital. Banks in an attempt to offer their monetary system stability functions come as providers of a critical service that helps establish credits by creating liquidity.

Principal Functions

The principal functions of commercial banks form the foundation of their operations. These include mobilizing deposits, granting loans, and creating credit, which directly fuel economic growth and ensure the efficient allocation of resources.

- Accumulation of Deposits: Commercial banks attract savings through providing various deposit accounts to various customers:

- Saving Deposits: This encourages saving for persons earning some interest therefrom, hence enriching the savings culture.

- Checking Deposits: This is a deposit for business institutions that require ample liquidity to allow their operating system.

- Time Deposits: These are offered at a higher rate to encourage people and corporations to block funds for longer periods.

Aggregating deposits, banks garner significant amounts of money that can be utilized productively.

- Loans: Banks provide loans to cater to various financial requirements of different industries. Loans are availed in several forms:

- Personal Loans: It is used to meet emergencies, education, or personal expenses to enhance living standards.

- Business Loans: Support expansion, enabling companies to buy inventories, buy equipment, or expand operations.

- Agricultural Loans: Support the rural sector through financing farming and other rural development activities.

In this way, banks directly energize economic activity, encourage entrepreneurship, and create jobs.

- Creating Credit: Commercial banks expand the economy by granting credit. They lend more than the deposits received from them, but they leave a small portion as a reserve. This boosts the money supply in the economy. The process raises the purchasing power of the people, promotes investment, and stimulates economic growth.

Secondary Functions

Secondary functions complement the primary roles of commercial banks, enhancing customer convenience and supporting financial systems. These include offering agency services, general utility services, and investment options to cater to diverse financial needs.

- Agency Services: Commercial banks offer other basic services that make the management of their customers’ finances much easier:

- Receipt of dunning, dividends, and insurance premiums

- Utility collection on behalf of account holders such as electricity, water,r and gas bills, and subscription services.

These services enable customers to save time and have convenience with respect to which results in strengthening confidence in the banking system.

- General Utility Services: The following high-values utilities, are provided by the banks to improve customer satisfaction and assistance in international trade:

- Safe deposit lockers for safe storage of valuable items

- Letter of credit and traveler’s cheque for cash transactions.

- Foreign exchange services to enable international trade and travel.

- Investment Services: Banks make sure that reserves are used appropriately by investing their excess in government securities and other low-risk instruments. These investments generate income for the banks, ensure liquidity, and contribute to the national financial stability.

These comprehensive functions make commercial banks financial lifelines that ensure smooth economic operations and promote inclusive growth. They create a secure financial environment where individuals and businesses can thrive.

List of Commercial Banks in India

India’s banking system constitutes several commercial banks that cater to the financial needs of individuals, businesses, and industries. These banks are divided into public sector banks, private sector banks, foreign banks, and regional rural banks. Further down the article is a list of commercial banks in India, including information on the biggest, oldest, and newest banks.

- Public Sector Banks: State-owned banks account for the majority of India’s banking market.

- State Bank of India: It was founded in 1806 as the Bank of Calcutta; and merged with Imperial Bank of India in 1955 to become the State Bank of India . It has a Strong network of over 22,000 branches and myriad digital banking products and services. It is the oldest and largest commercial bank in India.

- Bank of Baroda: Founded in 1908. It has Presence across more than 20 countries and strong corporate banking

- Canara Bank: Founded in 1906. It is known for Financial inclusivity initiatives, including schemes for rural banking.

- Punjab National Bank (PNB): Its Year of Establishment was 1894. It is Known For Affordable credit options for small businesses and agriculture.

- Private Sector Banks: Private sector banks are known for their customer-centric approach and technological advancements.

- HDFC Bank – Largest Private Sector Bank in India.Year of Establishment: 1994.Known For: Leading in digital banking and offering a wide range of personal banking services.

- ICICI Bank: Year of Establishment: 1994.Known For: Comprehensive retail banking and innovative financial products.

- Axis Bank: Year of Establishment: 1993. Known For: Corporate banking and strong digital presence.

- Kotak Mahindra Bank – Newest Private Sector Bank in India. Year of Establishment: 2003. Known For: Personalized financial solutions and rapid growth in retail banking.

- Foreign Banks Operating in India: Foreign banks serve international and high-net-worth clients with specialized financial services.

- HSBC: Year of Establishment in India: 1853. They are known for: Comprehensive trade finance solutions, serving international business.

- Standard Chartered: The year they came to India: 1858. Known for: Long-standing competencies in treasury and investment banking

- Deutsche Bank: The year it came to India: was 1980. Known for: Specialized wealth management and institutional banking

- Citibank: The year it came to India: was 1902. Known for: Innovations in credit cards and corporate bank services

- Regional Rural Banks (RRBs): RRBs are known to provide better access to financial products in the rural markets, especially for agricultural and small-scale industries.

- Uttar Bihar Gramin Bank: Year of Setup: 2008.Mainly Known: For offering bank and credit facilities to the households of rural villages in Bihar

- Andhra Pradesh Grameena Vikas Bank: Year of Setup: 2006. Mainly known: For Agriculture and self-help groups in the state of Andhra Pradesh.

Commercial Banks in India FAQs

What are commercial banks and what are their roles in India?

Commercial banks are those institutions that provide facilities for deposits and credits to promote economic growth and ensure financial inclusion.

How can commercial banks be classified in India?

They fall under the following heads: Public Sector Banks, Private Sector Banks, Foreign Banks, Regional Rural Banks (RRBs), and Cooperative Banks.

What are the major business activities of commercial banks in India?

They accept deposits, advance and collect payments, and conduct foreign exchange, besides financial inclusion.

How are the commercial banks regulated in India?

They are regulated by the Reserve Bank of India through licensing, audits, capital norms, and compliance monitoring.

What are the problems of commercial banks in India?

The major issues confronting the banking sector are mounting NPAs, adapting to new technology, financial inclusion, regulating entities, and competencies from fintechs.