Cross currency swaps are essential rather than financial establishments as an agreement that enables one country’s commercial party to exchange principal amounts into different currencies and thereby even interest rates for another country’s commercial party to hedge against unfavourable movements in exchange rates. The currency fluctuation risks that may arise from certain transactions are sought to be covered by such a hedge.

Cross Currency Swap Hedge

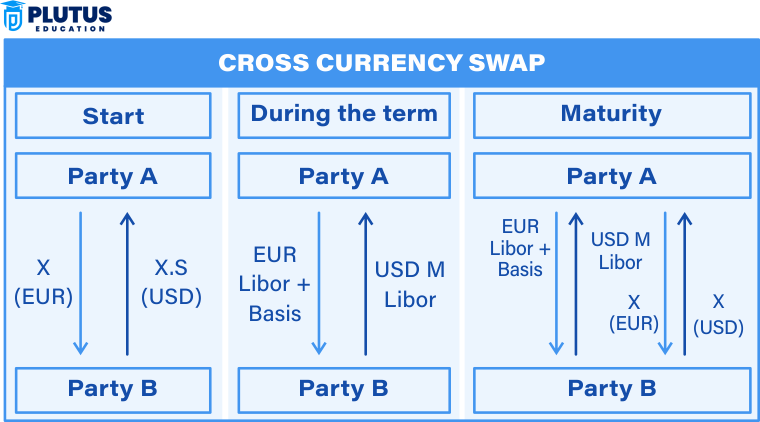

Thus, a standard cross-currency swap hedge is an instrument under which the parties engage mutually to exchange dissimilar principal amounts in their currency and make periodic interest payments to one another. Thus, it makes international trade and investment more predictable since it reduces the effect of currency fluctuations on a business or an institution. The swap is made at a previously agreed exchange rate and usually involves lending, and a final settlement of the amount exchanged being restored to the parties involved. Cross-currency swaps have been widely popular among corporations for risk management. However, the real benefits arise when the company has foreign currency assets or liabilities. A classic example would be an Indian company borrowing in U.S. dollars that uses a cross-currency swap hedge to fix its repayment costs in Indian Rupees.

Advantages of Cross-Currency Swap Hedge

Now look at the many reasons that make different companies cross-currency swap hedges:

- Zero risk: Zero risk associated with changes in the foreign exchange rate. Changes in the prices of foreign currencies normally crash the performance of an entity’s finances. Under cross-currency swap hedging, each side has fixed payments on any exchange, thus reducing the uncertainty.

- Reduced directional interest rate risks: Different interest rates exist in different countries, which might enable a company to choose a fixed rate in one country to equate to the variable one in another so that its borrowing is at constant costs.

- Access to cheaper financing: Most companies borrow at a low interest rate and convert their borrowings into local currencies to achieve lower financing costs.

- Long-Term Stability. In contrast to spot or forward contracts, cross-currency swap contracts may be structured on an open-ended basis, allowing scrutiny to persist over long periods. Therefore, they are best suited for significant investments.

Risks Associated with Cross Currencies Swaps

However, there are many risks linked with these agreements.

- Exchange Risk: The efficient exposure could be bent if the swap is not appropriately defined.

- Credit Risk: An event of default to one party can result in losses incurred by the other party.

- Liquidity Risk: Insufficient liquidity in the cross-currency swap market may render it unfriendly to exit a position. Companies must consider these risks when entering a cross-currency swap agreement before starting effective or successful hedging.

- Interest Rate Risk: The movement of interest rates will affect swap payments, leading to uncertainty.

- Regulatory Risk: Different jurisdictions would have different rules regarding cross-currency swaps, which impact the execution of the contract.

Proper risk management strategies such as diversifying counterparties and using collateral agreements would help mitigate stupid risk from cross-currency swaps.

Cross Currency Swap vs Interest Rate Swap

Firms and investors often compare cross-currency and interest-rate swaps to decide which method best manages their financial risk. Both derivatives protect investors against interest-rate and currency risks, but mainly for different purposes. The cross-currency swap derivative entails exchanging principal and interest payments on the same loan in other currencies, while interest-. Meanwhile, apps only deal with the exchange of interest payments in the same currency. Understanding key differences helps them in selecting the right hedging strategy.

The cash-flow exchange component in cross-currency swaps consists of cash flows in different currencies. Cross-currency swaps can be fixed-fixed, fixed-floating, or floating-floating, depending on the peculiarities of the parties involved. The U.S.-based company agrees to a two-sided swap with a European firm in which dollars are exchanged for euros. Under this arrangement, the U.S. company obtains euros to finance its European operations, while the European company obtains dollars to fund its operations in the U.S.

In contrast, interest rate swap pairs allow two parties to exchange interest rate payments denominated in that currency. One party typically pays a fixed interest rate, while the other pays a floating rate. The principal amount remains unchanged, making interest rate swaps easier than cross-currency.

| Feature | Cross Currency Swap | Interest Rate Swap |

| Currency Exchange | Yes | No |

| Principal Amount | Exchanged at the beginning and end | No exchange of principal |

| Interest Payments | Paid in different currencies | Paid in the same currency |

| Use Case | Hedging exchange rate and interest rate risks | Hedging only interest rate risk |

| Complexity | Higher due to currency and interest rate risk analysis | since it involves only interest rates cross-currency |

It analyses their needs before selecting between cross-currency and interest rate swaps to ensure optimal financial management.

Accounting for Cross-Currency Swaps

Cross-currency swap accounting shall not be easy under international financial reporting standards. The swaps would thus be recognised on the company balance sheet, and the pertinent details would be disclosed in the financial statements.

How Cross Currency Swaps Are Accounted For?

A cross-currency swap accounting entry involves recognising the fair value of the swap agreement. The following rules will apply:

- Initial Recognition: Swap is entered when valued relatively at the point of contract entry.

- Periodic Adjustments. Interest payments and exchange rate shifts will move the valuation of the swap and, therefore, require updates periodically.

- Final Settlement: The exchanged principals are recorded on the swap’s maturity.

Any company under IFRS or GAAP must fully comply while reporting cross-currency swaps in their financial statements. Good accounting will prevent mistakes and promote financial report transparency.

Relevance to ACCA Syllabus

Cross-currency swap hedge is a key topic under ACCA’s Financial Manais, which is crucially needed in Financial Management (AFM) papers. It plays a vital role in risk management, hedging foreign exchange exposure, and managing interest rate risk. ACCA students must understand how these swaps work, how they are accounted for under IFRS 9 (Financial Instruments), and their role in corporate finance strategies. The ability to interpret and apply cross-currency hedging techniques is vital for making informed financial decisions in multinational organisations.

Cross Currency Swap Hedge ACCA Questions

Q1: Which IFRS standard governs the accounting treatment of cross-currency swaps?

A) IFRS 9

B) IFRS 15

C) IFRS 16

D) IFRS 7

Ans: A) IFRS 9

Q2: What is the primary objective of using a cross-currency swap hedge in corporate finance?

A) To speculate on foreign exchange rates

B) To convert a loan from one currency company while managing interest rate risk

C) To increase a company’s exposure to currency risk

D) To eliminate all financial risks in an international transaction

Ans: B) To convert a loan from one cross-currency other while material

Q3: In a cross-currency swap, which cash flows are typically exchanged between two parties?

A) Only the interest payments

B) The principal and interest payments

C) Only the principal payments at the start

D) Fixed interest rate for a floating interest rate in the same currency

Ans: B) The principal and interest payments

Q4: Which risk does a company aim to mitigate using a cross-currency swap?

A) Liquidity risk

B) Foreign exchange and interest rate risk

C) Credit risk

D) Operational risk

Ans: B) Foreign exchange and interest rate risk

Q5: How are gains or losses across currency swaps reported under IFRS?

A) Directly in the income statement

B) Through other comprehensive income if designated as a hedge

C) Only at the time of maturity

D) Ignored for accounting purposes

Ans: B) Through other comprehensive income if designated as a hedge

Relevance to US CMA Syllabus

The US CMA syllabus emphasises financial risk management, including derivative instruments like cross-currency swaps. This topic is covered under Part 2: Financial Decision Making, where candidates must understand hedging techniques to mitigate currency and interest analyses. Cross-currency kings in multinational corporations must analyse cross-currency swaps for effective treasury management and financial planning.

Cross Currency Swap Hedge US CMA Questions

Q1: How does a cross-currency swap differ from a regular interest rate swap?

A) It only swaps interest rates between two parties

B) It involves an exchange of principal and interest payments in different currencies

C) It is used only for short-term risk management

D) It eliminates all currency risks

Ans: B) It involves an exchange of principal and interest payments in different currencies

Q2: In a cross-currency swap hedge, which party benefits when the foreign currency appreciates against the home currency?

A) The payer of the foreign currency

B) The receiver of the foreign currency

C) Both parties equally

D) The central bank

Ans: B) They receive cross-currency currency

Q3: Why might a company enter into a cross-currency swap?

A) To increase exposure to exchange rate risk

B) To hedge against currency fluctuations and interest rate changes

C) To speculate on currency movements for profit

D) To reduce working capital requirements

Ans: B) To hedge against currency fluctuations and interest rate changes

Q4: Which financial metric is most impacted by cross-currency swap hedging?

A) Net Profit Margin

B) Cost of Capital

C) Inventory Turnover Ratio

D) Gross Profit

Ans: B)cross-currency

Q5: What is the role of the counterparty in a cross-currency swap?

A) To provide loans to businesses

B) To facilitate the exchange of cash flows in different currencies

C) To act as a financial advisor

D) To eliminate financial risks completely

Ans: B) To facilitate the exchange of cash flows in different currencies

Relevance to US CPA Syllabus

The US CPA exam covers cross-currency swaps under financial instruments, particularly in the Financial Accounting and Reporting (FAR) and Business Environment and Concepts (BEC) sections. CPAs must understand the reporting, valuation, and disclosure requirements for these derivatives under US GAAP and IFRS, making this topic essential for corporate accountants and auditors.

Cross Currency Swap Hedge US CPA Questions

Q1: Under US GAAP, how should a cross-currency swap hedge be classified?

A) Operating lease

B) Derivative instrument

C) Capital lease

D) Revenue contract

Ans: B) Derivative instrcompany’s How are cross-currency swaps typically recorded on a company’s financial statements?

A) As contingent liabilities

B) As financial liabilities or assets at fair value

C) As non-operating revenue

D) As a capital expenditure

Ans: B) As financial liabilities or assets at fair value

Q3: Which accounting principle dictates the treatment of cross-currency swaps in financial statements?

A) Historical cost principle

B) Fair value measurement principle

C) Revenue recognition principle

D) Matching principle

Ans: B) Fair value measurement cross-currency Which regulatory body oversees the reporting of cross currency swaps in the United States?

A) SEC (Securities and Exchange Commission)

B) IRS (Internal Revenue Service)

C) IMF (International Monetary Fund)

D) OECD (Organisation for Economic Co-operation and Development)

Ans: A) SEC (Securities and Exchange Commission)

Q5: What disclosure is required for cross-currency swaps under ASC 815?

A) No disclosure is required

B) Only qualitative descriptions of the swap

C) The fair value, notional amount, and risk management objective

D) Only realised gains and losses

Ans: C) The fair value, notional amount, and risk management a cross-currency

Relevance to CFA Syllabus

Cross-currency swaps are extensively covered in the CFA curriculum under Derivatives, Fixed Income, and Risk Management topics. CFA candidates must analyse how these swaps impact interest rates, foreign exchange risks, and portfolio hedging strategies. The CFA program emphasises valuation techniques, risk mitigation, and their role in global financial markets.

Cross Currency Swap Hedge CFA Questions

Q1: What is the primary advantage of using a cross-currency swap for investors?

A) It allows direct equity investments in foreign markets

B) It enables borrowing in foreign currency at a lower interest rate

C) It eliminates market risk entirely

D) It increases exposure to exchange rate fluctuations

Ans: B) It enables borrowing in foreign currency at a lower interest rate

Q2: Which type of interest rate structure is commonly used across currency swaps?

A) Floating-to-floating and fixed-to-fixed

B) Only fixed-to-fixed

C) Only floating-to-floating

D) No interest payments are exchanged

Ans: A) Floating-to-floating and fixed-to-fixed

Q3: Why might a fund manager use a cross-currency swap in portfolio management?

A) To reduce foreign exchange exposure

B) To increase transaction costs

C) To create speculative opportunities

D) To eliminate the need for hedging

Ans: A) To reduce foreign counterparty’sure

Q4: How does a rise in interest rates in the counterparty’s country impact a cross-currency swap agreement?

A) It has no effect

B) It increases the cost of borrowing in that currency

C) It decreases the interest payments in both currencies

D) It forces the termination of the swap

Ans: B) It increases the cost of borrowing in that currency

Q5: What is the most common valuation method for cross-currency swaps?

A) Cost method

B) Discounted cash flow (DCF) method

C) Straight-line amortisation

D) Net realisable value

Ans: B) Discounted cash flow (DCF) method