Price is assigning monetary value to a product or service that a purchaser pays, and a seller gets in exchange. To understand how to define price, one must know the basics of economic theory and real business activity, determine how markets function, and allocate resources. Price is not a number but reflects perceived value, underpriced costs, and the market’s wide economic conditions. Concepts like price elasticity, price discrimination, and pricing policy would also go with these accusations to better understand their consequences in business and economic terms.

Define Price with Example

Understanding how businesses price their products and services reveals an important part of the economy. Some other examples are provided in the later sections: A longer and more involved example of the price determination is shown here in a table format that demonstrates how cost plus added and then selling price connects with it. The selling price will include both production and other costs. This example refers to the strategies for pricing consideration.

| Product/Service | Price (Rs) | Market Influence |

| Apple (1 kg) | 3 | Affected by seasonal demand and supply |

| Mobile Phone | 800 | Determined by brand, technology, and features |

| Car (Sedan) | 20,000 | Affected by economic conditions and competition |

| Internet Subscription | 50/month | Driven by service providers and technology |

| Movie Ticket | 10 | Set based on location and consumer preference |

Define Price Discrimination

Price discrimination is referred to as the charging of different prices to different segments of a market for the same product or service. This is revenue-maximizing because of the variation in willingness to pay of the different segments of customers. For example, an airline charges different ticket prices depending on when you have booked the flight, your preferred seat, and the circumstances of purchasing the ticket.

Define Price Elasticity of Demand

Price elasticity of demand, therefore, measures the responsiveness of demand for a given commodity to changes in its price. A high elasticity indicates large swings in demand corresponding to small price changes. This measurement assists in determining possible shifts in sales volume once price adjustments are made.

Define Minimum Support Price

This is price intervention from governments so that producers (farmers in this case) could get a minimum price for their produce that covers production costs and, therefore, protects them from losses due to unfavourable fluctuations in market prices.

Define Pricing Policy

A pricing policy is the strategic framework under which a company prices its products or services. These policies consider market demand, production costs, competitor pricing, and overall business goals.

Role of Price in the Market

Price assumes several roles in the market: communicator, balancer, and incentive, among others. Each of these roles is important in the functioning of micro and macroeconomic systems.

- Signalling: Prices send important signals to consumers and producers about the value of goods and market demand.

- Balancing Supply and Demand: Prices are matched to the quantity of goods supplied with the amount demanded to achieve equilibrium within the market.

- Resource Allocation: Having been established, prices allow resources to be efficiently allocated over the economy, ensuring that goods and services are produced where consumers most value them.

- Incentive for Economics: It draws up the curves of demand as higher prices have the economic incentive for producers to increase their sales and discourage them from overproduction as the prices decrease.

- Income Distribution: Pricing determines how income is distributed among different economic sectors, thus impacting equality in the internal economy.

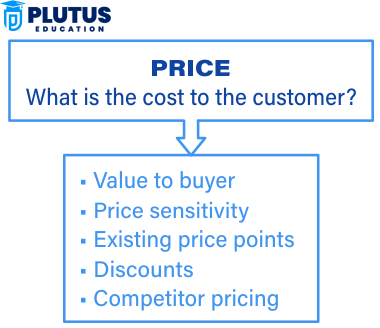

Factors Affecting Pricing

Many factors influence price settings, with every factor important for pricing strategy. Price determination also ensures that economic realities meet business prerogatives.

- Cost Of Production: Direct costs associated with producing goods, like materials and labour, would most importantly determine base prices.

- Market Demand: Demand level sets a price for the product, with higher demand leading the price upwards while less demand pulls a price downwards.

- Competition: The more intense the competition in a market, the more elastic the pricing methods are, with more competitors driving prices lower for all. Government Policies include laws, taxes, and subsidies from government organs that can affect pricing.

- Economic Conditions: Macroeconomic trends like inflation or depression can build or break the pricing decision.

Market Structure

The market structure fundamentally determines prices, affecting consumer behaviour and business profits.

- Perfect Competition: In a perfect competitive market, many small sellers and buyers cannot individually influence price, so the market determines the equilibrium price.

- Monopolistic Competition: Firm differentiation gives the firms a slight price control.

- Oligopoly: These markets are dominated by a few large firms that can act jointly in setting prices to the detriment of consumers.

- Monopoly: The monopolist is usually a single seller with much freedom in setting prices, often at the buyers’ expense.

- Contestable Markets: Here, barriers to entry and exit are minimal, allowing limited competition to enforce pricing discipline.

Types of Prices

Companies use different pricing models to best respond to market demands and multiply revenues.

- Market Price: The price at which goods and services are offered in the market relative to the current supply and demand.

- Cost-Plus Pricing: A relatively simple method whereby a certain margin is added on top of cost; the resulting figure becomes the selling price.

- Penetration Pricing: Designed to gain market share quickly, this practice sets low initial prices to lure buyers away from established competitors.

- Price Skimming: A more widely used procedure for the launch stage of a new product, in which extortionate prices are charged initially before being lowered gradually in response to market resistance.

Different Pricing Strategies

As pricing strategies become more advanced, they must be integrally concerned with the company’s specific market circumstances and business objectives, optimizing profitability and maximizing market share.

- Premium Pricing: This involves setting a price above that of comparable products to signify that they are better quality and more exclusive.

- Economy Pricing: The firm minimizes its expenditure on the marketing and production of the product so that it can sell those products at very low prices, appealing to price-conscious consumers.

- Bundle Pricing: The offer of several products or services bundled at a price lower than the total of the individual item prices.

- Psychological Pricing: Set any price that appears nominally lower, such as INR 9.99 instead of INR 10, so that the customer appreciatively reacts to such a price psychologically.

- Promotional Pricing: Price decreases for a limited period, which helps to increase sales and clear inventory substantially.

Price FAQs

What does define price discrimination imply?

Price discrimination is when different prices are charged for the same product across various market segments to maximize revenues by capitalizing on the discrepancies.

How do you define price elasticity of demand?

Price elasticity of demand is the extent to which demand for a product will change with a price change. Where demand is said to be elastic, it indicates a situation whereby small price changes lead to significant changes in demand.

What is meant by define Minimum Support Price?

Minimum Support Price is a government policy to save producers from volatile market prices by imposing a minimum price, enabling the producers to at least cover their cost of production.”

What does define pricing policy consist of?

Pricing policy is how a company approaches setting prices for its products and services, considering cost, competition, and market demand.

Define price?

Putting it simply, defining price means giving a monetary value to a particular product or service, wherein the cost of production, demand and supply in the market, and competition come into play regarding the price a customer will pay and a business will receive.