Demand is a central concept in economics that plays a foundational role in understanding how markets work. If we ask, “What is demand?” the answer goes beyond mere desire. In economics, demand is defined as the quantity of a good or service that consumers are willing and able to buy at various prices during a given time period. The emphasis is on three key factors: the desire for a product, the ability to purchase it (usually with income or credit), and the willingness to spend that money. All three factors must be present for demand to exist. This article will explain the full scope of demand, including demand meaning, formal definitions, its features, types, graphical representation through the demand curve, factors that influence demand, real-life examples, and how understanding demand helps businesses design better strategies.

What is Demand?

Demand is not just about wanting something. In economics, demand requires purchasing power and the intention to buy. This section answers the core question, “What is demand?” with detailed explanation.

Demand Meaning in Economics

In economics, demand means the total amount of a product or service that consumers are ready to buy at different prices in a specific time frame. This definition implies several things:

- Demand always relates to a price point.

- It exists within a defined time period.

- It refers to a certain quantity of goods or services.

- It must be supported by buying power.

Key Components of Demand

- Desire: The consumer must have the wish to own a product.

- Ability to Pay: The consumer must have the resources (cash, credit, income).

- Willingness to Pay: The consumer must decide to spend that money.

If any one of the above is missing, demand does not exist. For example, thousands of students may wish to buy an iPhone, but only a few who can afford it and are willing to pay will create actual demand.

Example

If a bakery sells 100 loaves of bread daily at Rs. 40 each, and when the price is reduced to Rs. 30, daily sales rise to 150 loaves, the increase reflects a change in demand due to a change in price.

Demand vs Quantity Demanded

- Demand: Refers to the entire relationship between price and quantity demanded.

- Quantity Demanded: Refers to the specific amount demanded at a specific price.

Understanding this difference is vital in economic analysis, especially when drawing the demand curve.

Demand Definition by Economists

Many economists have defined demand in specific terms that highlight its role in the economic system. These definitions add depth to our understanding of what constitutes demand.

Alfred Marshall’s Definition

“The amount demanded of a commodity is the amount which will be bought at a given price in a given period.”

Marshall emphasized two points:

- The relation between price and quantity.

- A specified period, like a day, week, or month.

Marshall’s theory introduced the concept of elasticity of demand and consumer surplus, which are based on this core definition.

Paul Samuelson’s Definition

“Demand is a schedule of the quantities of a good that will be purchased at various prices at a given time.”

Samuelson introduced the idea of a demand schedule, which later becomes the foundation of demand curves. It shows how quantity demanded varies with changes in price.

Prof. Benham’s Definition

“The demand for anything at a given price is the amount of it which will be bought per unit of time.”

Benham focuses on per-unit-time measurement, which helps in estimating production requirements and revenue projections.

Features of These Definitions

- All definitions treat demand as a function of price.

- They underline that demand only exists if the consumer is ready to pay.

- Demand is always considered within a specific time frame.

These academic definitions form the basis for all further study of microeconomics, market behavior, and business strategy.

Features of Demand

To understand demand thoroughly, we must look at its unique characteristics. These features differentiate demand from just consumer wants.

1. Price Dependency

Demand always depends on price. If all other conditions remain the same, any change in price will cause a corresponding change in quantity demanded. For instance, if the price of onions rises from Rs. 20/kg to Rs. 60/kg, household consumption typically drops significantly.

2. Quantity Specificity

Demand must refer to a specific quantity. A statement like “I want to buy rice” is not valid in economics unless the consumer specifies the quantity and the price at which they want it.

3. Time-Bound Nature

Demand must relate to a specific time period. It is incorrect to say, “India’s demand for smartphones is high” without stating whether it’s monthly, yearly, or during the festival season.

4. Utility-Driven

Utility, or the satisfaction derived from consumption, drives demand. If a product does not offer value or utility, people will not demand it, regardless of price.

5. Marginal Utility and Demand

Each additional unit of a product gives less satisfaction to the consumer. This law of diminishing marginal utility affects demand, especially for items like food or beverages.

6. Subject to Change

Demand is dynamic and changes with economic factors like income, inflation, and technological progress. For instance, the demand for 4G phones dropped as 5G models became more affordable.

7. Consumer-Specific and Market-Wide

Demand can be calculated at both individual and market levels. While a single buyer may demand 2 notebooks, the entire student population may create a market demand for 2 crore notebooks.

Understanding these features helps economists and businesses make more accurate forecasts, policies, and strategies.

Types of Demand in Economics

Demand is not a single-dimensional concept. Economists have classified it into different types based on its nature, behavior, and influencing factors. Each type provides unique insight into how the economy functions.

1. Price Demand

This is the most basic form. It refers to the change in quantity demanded due to a change in price. For example, the demand for mangoes increases in summer when prices drop.

2. Income Demand

This shows how demand changes with a change in income.

- Normal Goods: Demand increases as income rises.

- Inferior Goods: Demand decreases as income rises (e.g., people shift from local soap to branded soap).

3. Cross Demand

This involves demand for one product based on the price of another related product.

- Substitute Goods: Tea and coffee. If tea prices rise, coffee demand increases.

- Complementary Goods: Pen and ink. If ink prices rise, pen demand may also fall.

4. Joint Demand

When two goods are used together, they are in joint demand. For example, smartphones and chargers.

5. Composite Demand

When a product is used for multiple purposes, it faces composite demand. Milk is a classic example in India—it is used for drinking, sweets, tea, and religious rituals.

6. Direct and Indirect Demand

- Direct Demand: For goods consumed by consumers (e.g., food, clothes).

- Indirect Demand: For goods used to produce other goods (e.g., raw materials).

7. Individual vs Market Demand

- Individual Demand: Demand from a single consumer.

- Market Demand: Total demand from all consumers.

Each type of demand helps businesses and policymakers understand consumer behavior more accurately and make better economic decisions.

Law of Demand and Demand Curve

The Law of Demand is a fundamental concept in economics that describes how price influences consumer behavior. It establishes an inverse relationship between the price of a product and the quantity demanded. This principle is universal across most goods and services.

The Law of Demand

The Law of Demand states:

“Other things being equal, as the price of a good increases, the quantity demanded decreases; and as the price decreases, the quantity demanded increases.”

This law assumes that factors like consumer income, preferences, and the prices of related goods remain constant.

Key Assumptions of the Law of Demand

- No Change in Consumer Income

- No Change in Prices of Related Goods

- No Change in Consumer Preferences

- No Change in Population Size

If any of these factors change, the law may not hold.

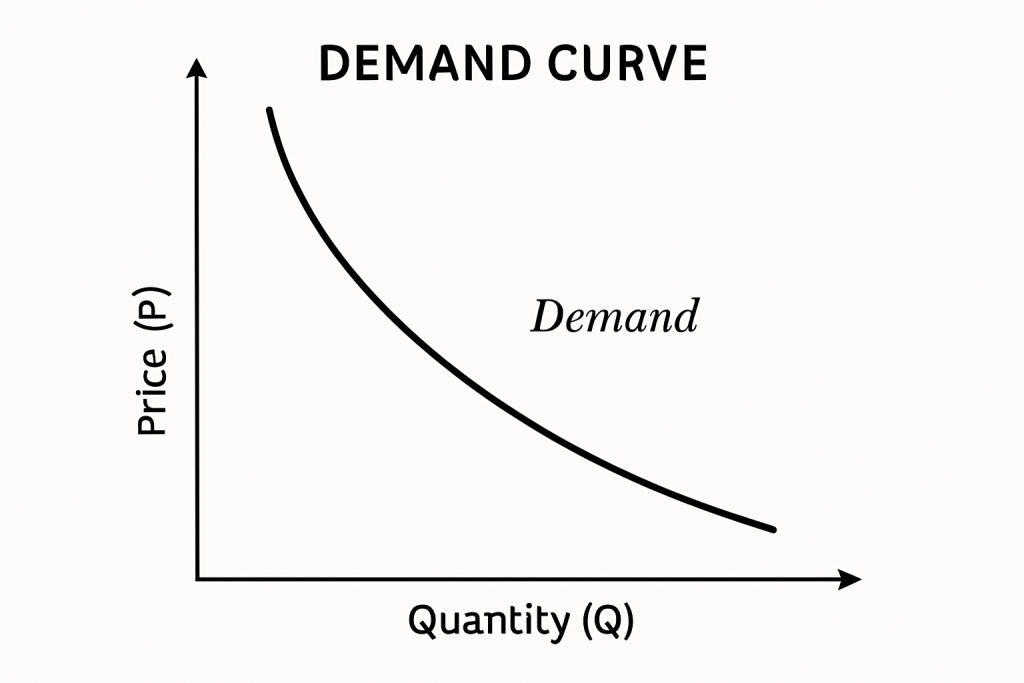

Demand Curve

The demand curve is a graphical representation of the Law of Demand. It plots price on the Y-axis and quantity demanded on the X-axis. The curve usually slopes downward from left to right.

Why the Demand Curve Slopes Downward

- Substitution Effect: Consumers shift to cheaper alternatives.

- Income Effect: A lower price increases real income, allowing consumers to buy more.

- Diminishing Marginal Utility: Each additional unit consumed offers less satisfaction, so consumers are only willing to buy more at a lower price.

Exceptions to the Law of Demand

- Giffen Goods: Inferior goods that poor households consume more of when prices rise.

- Veblen Goods: Luxury goods where demand increases with price due to status symbol.

- Necessities: Essential goods may have inelastic demand despite price changes.

Understanding the Law of Demand and the demand curve is essential for pricing decisions, sales forecasting, and policy-making.

Factors Affecting Demand

Several factors influence consumer demand, making it a dynamic concept. Understanding these helps in market analysis and demand forecasting.

1. Price of the Product

The most direct factor. Generally, higher prices lead to lower demand and vice versa. For example, a rise in petrol prices often reduces non-essential travel.

2. Consumer Income

- Normal Goods: Demand rises with income (e.g., branded clothes).

- Inferior Goods: Demand falls with income (e.g., local rice).

In India, rising middle-class incomes have shifted demand toward premium products.

3. Prices of Related Goods

- Substitutes: Price increase in one leads to demand increase in the other (e.g., Coke and Pepsi).

- Complements: Price increase in one leads to demand drop in the other (e.g., printer and cartridge).

4. Consumer Preferences and Trends

Cultural changes, advertising, social media, and peer influence play huge roles. For example, demand for plant-based milk has increased among health-conscious Indians.

5. Population Size and Composition

A younger population boosts demand for electronics and education services. India’s demographic dividend plays a big role in high aggregate demand.

6. Season and Climate

Umbrellas and raincoats peak in monsoon, while woollens spike in winter. Demand is often seasonal for items like ACs, fans, and beverages.

7. Future Price Expectations

If consumers expect prices to rise soon, they purchase more now. For example, during pre-GST rollouts, demand for electronics surged.

8. Government Policies and Taxes

Subsidies, tax relief, or higher duties affect demand. For example, GST cuts on EVs helped increase their demand.

Understanding these factors allows policymakers and companies to fine-tune their decisions for better outcomes.

Examples of Demand in Real Life

Examples from day-to-day life make the concept of demand easier to understand. Demand is visible in every sector and at all income levels.

1. Festive Season Shopping

During Diwali or Eid, consumers increase spending on clothes, electronics, and sweets. The sudden spike in demand during these times helps businesses clear inventory and increase turnover.

2. Petrol and Diesel Consumption

When fuel prices increase, people reduce car usage and rely more on public transport or carpooling. This demonstrates the price-demand relationship clearly.

3. Online Sales and Discounts

Platforms like Flipkart and Amazon see massive sales during events like Big Billion Days. Lower prices create high demand for electronics, clothing, and home appliances.

4. Weather-Based Demand

Demand for cold drinks peaks in summer, while demand for heaters and geysers rises in winter. Umbrella demand increases during monsoon. These are clear cases of seasonal demand.

5. COVID-19 Pandemic

There was an unexpected surge in demand for health products like sanitizers, masks, thermometers, and oximeters. Demand for remote work tools like laptops and webcams also skyrocketed.

6. Educational Products and Courses

After the pandemic, online learning became common. This boosted demand for smartphones, tablets, and platforms like BYJU’s, Vedantu, and Unacademy.

7. Gold and Investment Products

During inflation or geopolitical tension, Indian families tend to buy more gold. Gold demand often acts as a hedge against rising prices and uncertainty.

8. Real Estate and Home Loans

A fall in interest rates leads to an increase in demand for home loans. Developers often offer deals during such times, creating a positive cycle in real estate demand.

Each of these real-world cases reflects one or more features of demand, showing how prices, income, expectations, and external conditions influence what people buy.

Importance of Understanding Demand in Business Strategy

Understanding demand is not optional for businesses — it’s critical for survival and success. Companies base their entire planning and operations around current and future demand patterns.

1. Pricing Strategy

Businesses adjust prices based on demand elasticity. For example, Ola and Uber use surge pricing algorithms that reflect real-time demand.

- High demand = Higher prices

- Low demand = Discount offers

Pricing decisions based on demand data help in maximizing revenue without losing customers.

2. Product Planning and Development

Consumer demand data guides product features, sizes, packaging, and even design. For instance, Parle-G introduced mini packs priced at Rs. 2 after observing rural demand for smaller, affordable options.

3. Inventory and Supply Chain Management

Forecasting demand helps companies avoid overproduction or stockouts. E-commerce platforms like Amazon use predictive algorithms to ship goods to warehouses before orders are placed, based on demand trends.

4. Marketing and Promotion

Marketing teams use demand insights to run targeted campaigns. For example, a spike in demand for healthy foods has led brands to market sugar-free, gluten-free, and organic options aggressively.

5. Financial Planning and Budgeting

Sales forecasts based on demand allow businesses to plan budgets, cash flow, and investments. It ensures they are neither over-capitalized nor under-resourced.

6. Expansion Decisions

Businesses expand into new geographies only after demand feasibility studies. For example, retail chains like D-Mart or Reliance Trends open stores in cities where demand projections show profitability.

7. Risk Mitigation

Demand dips are early warning signs. Businesses track these signs to adjust production, reduce expenses, or launch promotions to maintain revenue.

In conclusion, demand is not just an academic concept — it is a practical business tool. Whether a company is launching a new product, setting prices, or planning an expansion, demand analysis is a necessary first step.

FAQs on Demand

1. What does demand mean in economics?

Demand in economics refers to the quantity of a product or service that consumers are both willing and able to purchase at different price levels over a specific period. It requires purchasing power and willingness to pay.

2. Which is the best definition of demand?

The best definition of demand is given by Alfred Marshall: “The amount demanded of a commodity is the amount which will be bought at a given price in a given period.”

3. What is demand in short answer?

Demand is the ability and willingness of consumers to buy a product at a specific price within a specific time.

4. Why does the demand curve slope downward?

The demand curve slopes downward because of the inverse relationship between price and quantity demanded. Reasons include the substitution effect, income effect, and diminishing marginal utility.

5. What are the 4 types of demand?

The four key types of demand are:

- Price Demand

- Income Demand

- Cross Demand

- Joint Demand

These types show how demand changes with price, income, or related goods.

6. What is a demand example?

If a student buys 10 pens when the price is Rs. 5 per pen and only 6 pens when the price increases to Rs. 10, this is an example of demand reacting to price change.

7. What is the law of demand?

The law of demand states that, all other things being equal, the quantity demanded of a good falls when the price rises, and rises when the price falls.