The business structure adopted when starting an enterprise plays a significant role in the operation of such an enterprise. There are two main types of businesses: proprietorship and partnership. The defining factors regarding the differences between proprietorship and partnership are ownership, liability, decision-making, and profit-sharing. In other words, a sole proprietorship is a business owned and managed by one person, and in a partnership, the duties, profits, and liabilities are shared among two or more people.

A sole proprietorship is the simplest business and does not need high registration formalities. The owner controls everything and stands to lose everything. The other hand carries partnerships, which share responsibilities and resources in maintaining a business. The main difference between a sole proprietorship and a partnership is the number of owners. One person owns a sole proprietorship, while two or more people own a partnership. The partnership shares the financial burden and operational tasks but also requires mutual trust and legal agreements. The choice of one or the other structure depends on factors like business aim, input of capital, supposed liability, and authority of decision makers.

Partnership Definition

A partnership is a business relationship where two or more parties agree to run a jointly owned business in tandem with profits and losses. Whereas a sole proprietorship is run by one person solely, the successes and failures, as well as the joint financial input of different partners, come into play in a partnership.

In a partnership, all partners share a legal agreement drafted according to their partners’ names, roles identified in the agreement, profit-sharing ratio, and any other responsibilities that may be referenced in the partnership agreement. The collection of partners’ working interests is a point of departure to speak of partnership; that is, one legal document whereby all partnership members focus on that common interest, namely the business development. The profit-sharing ratio may be split or shared according to the partners’ agreement.

Establishing a partnership is common, and many people come together to form a business and pool their expertise, skills, and resources. This makes the partnership structure a more stable business model in that no single individual bears the totality of the financial risks involved.

Partnership Deed

A partnership deed is a legal document that states the rights, duties, and profit-sharing ratio of the partners engaged in a business. The agreement is thus proof of their agreement and shall help avoid disputes amongst the partners later.

A partnership deed contains information on:

- Name and address of the partnership firm

- Names and addresses of all partners

- Nature of business

- Capital contribution from each partner

- Profit and loss sharing ratio

- Duties and responsibilities of each partner

- Rules for admission and exit of partners

- Dispute resolution mechanism

Terms for Dissolution of the Partnership

A proper partnership deed guarantees the business will flow smoothly, incurring a minimum of wear and tear throughout its course. Without a partnership deal, misunderstandings may arise into full-blown legal complications. Such a document binds all partners equally concerning responsibilities.

Types of the Partnership

The partnership may be classified into different kinds based on the level of liability and active participation. Knowing the types of partnerships is crucial before forming a partnership firm.

General Partnership

In a general partnership, every partner is equally responsible for the day-to-day operations of the business and the liabilities that arise therefrom. Each partner has an equal input to the decision-making with everyone being liable without limits to all debts.

Limited Partnership (LP)

Limited partnerships have both general and limited partners. General partners have unlimited liability for the partnership’s actions, and they are in control of the business’s normal operations. Limited partners contribute capital and have limited liability.

Limited Liability Partnership (LLP)

A limited liability partnership protects all partners against liability. A partner’s liability is limited to the extent of his investment; he cannot be held responsible for any misconduct by another partner.

Joint Venture Partnership

A joint venture partnership is established for a particular project or a limited time. After the completion of the stated objective, the partnership shall be dissolved.

Define Sole Proprietorship

A sole proprietorship is a business with one owner, which is a single-person business. This is the simplest business structure, where the owner has complete control over operations, finances, and profits. Because no partners are involved, decisions in a sole proprietorship are made fairly quickly, and the owner has full authority over business activities.

A sole proprietorship is not legally separate from its owner. Therefore, the owner is liable for all business debts and legal obligations. Sole proprietorships are easy to establish but pose financial risks by unlimited liability.

Sole Proprietorship Registration

Sole proprietorship registration provides a very simple process with no legal formalities. As we find in partnerships or corporations, no such advanced registrations are involved with sole proprietorships.

Sole Proprietorship Registration

Registration as a sole proprietorship is easy. Because it is not a legal entity, business proprietors are not required to subject themselves to long, tedious legal procedures for commencing their business operations. However, registration may be necessary based on the type of industry, location, or nature of business.

- Decide on a Business Name: The first step in setting up a sole proprietorship after selecting a name is to ensure that it is not only distinctive but also a legitimate name. Some states demand that business names be registered to prevent duplicity.

- Obtain Licenses and Permits: Depending on the particular business, the owner might be required to procure licenses or permits of every kind, which entitles the holder to carry on business activities. These may include health permits, trade licenses, or professional entitlement.

- Tax Registration: These include getting a TIN (Tax Identification Number) or GST registration if applicable as per local regulations.

- Open Business Bank Account: Holding a separate business bank account is not required; however, it will separate business finances from personal ones.

- Get Business Insurance: It’s not required in all situations, but it protects sole proprietorship against loss from liability claims or unforeseen circumstances.

- Conform with Local Requirements: This might also be the case for occasional filings or compliance reports that must be submitted.

Features of Sole Proprietorship

The features of sole proprietorship make it an ideal and simple business formation. The most important conditions of this business model are the following:

Unipersonal Ownership

A sole proprietorship is owned and controlled by one person. The owner will have complete control over any matter affecting the conduct of the business, such as decision-making, finance, or operation of the firm. No partners or shareholders exist, so the owner gets all the profits.

No Separate Entity

Legally, there is no distinction between the sole proprietorship and the owner. In other words, whatever you owe or are indebted for in the business events’ names is solely on your shoulders. There is no separation of personal liabilities and assets from the business.

Full Control Over Operations

The owner decides how to run the business. He/she has the sole control over all crucial matters such as pricing, products, marketing, and other aspects dealing with customers without having to get permission from anyone, be it partners or a board of directors.

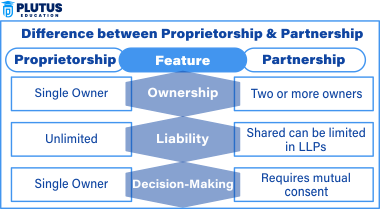

Explain the Differences Between Proprietorship and Partnership

Understanding the difference between a proprietorship and a partnership will assist owners in considering which structure is best for their firm. A sole proprietorship is good for a person who wants to keep control and have easy operational procedures, while a partnership allows for the division of responsibilities and financial strength.

| Feature | Proprietorship | Partnership |

| Ownership | Single Owner | Two or more owners |

| Liability | Unlimited | Shared can be limited in LLPs |

| Decision-Making | Quick and independent | Requires mutual consent |

| Registration | Simple, less formalities | Requires a legal agreement |

| Profit Sharing | Single owner gets all profit | Profit is shared among partners |

| Risk Factor | High personal risk | Shared risk |

| Business Continuity | It ends with the owner’s death | Can continue with new partners |

| Taxation | Taxed as personal income | Partnership taxation applies |

| Funding Options | Limited to personal savings | More funding options due to multiple partners |

| Legal Formalities | Minimal legal requirements | Requires partnership deed and agreements |

| Growth Potential | Limited due to single ownership | Greater due to combined resources and expertise |

Proprietorship Vs Partnership FAQs

1. What is the main difference between proprietorship and partnership?

The main difference between a proprietorship and partnership is that a sole proprietorship has one owner that controls everything in the business. In contrast, a partnership has multiple owners who share responsibilities and profits.

2. How can I register a sole proprietorship?

To register a sole proprietorship, choose a business name, apply for any required licenses, register for taxation, open a business bank account, and ensure compliance with other local regulations.

3. What are types of partnership?

Partnerships can be general partnerships, limited partnerships, limited liability partnerships (LLP), and joint ventures.

4. What are some examples of sole proprietorships?

Typical sole proprietorship examples include freelancers, local retail stores, small cafés, tutoring services, or home-based businesses.

5. Can a sole proprietorship be converted to a partnership?

A sole proprietorship can be converted into a partnership by adding partners and establishing a partnership deed outlining each partner’s responsibilities and ratios of profit-sharing.