The Structure of Commercial Bank is the organized framework within which the banks operate and their types, functions, and the regulatory framework that ensures the proper allocation of resources, safe custody of deposits, and provision of credit to individuals, businesses, and government. It’s essential to know this framework to know how the banks contribute to economic development. The Structure of a Commercial Bank represents the hierarchical and functional framework that defines how banks operate and deliver services. It categorizes banks based on their regulatory adherence, ownership, and scope of operations. This structure plays a crucial role in ensuring the effective mobilization of savings, provision of credit, and financial stability in an economy. Broadly, commercial banks are classified into scheduled and non-scheduled banks, with further divisions like public sector, private sector, foreign banks, and cooperative banks. This organized framework helps cater to the diverse financial needs of individuals, businesses, and industries, promoting inclusive growth and economic stability.

Commercial Bank

Commercial banks are financial institutions that accept deposits from the public and provide loans to individuals, businesses, and industries. They operate under strict regulations to maintain economic stability.

Features of Commercial Banks

- Accept Deposits: Commercial banks accept deposits from the public, offering interest rates to encourage savings.

- Lending Loans: They grant loans to the customers and generate revenue by taking interest.

- Facilitating Payments: Issuing cheques, demand drafts, and electronic transfers.

- Providing Credit Facilities: Offering overdraft and cash credit facilities for short-term requirements.

- Agency Services: Acting as agents for clients in fund transfers, utility bill payments, and tax remittances.

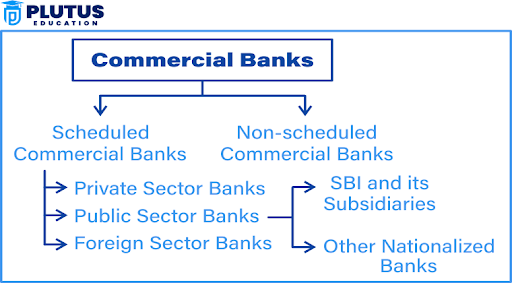

Scheduled Commercial Bank

A scheduled commercial bank is provided under the Second Schedule of the RBI Act, 1934. Scheduled banks are entitled to borrow from the RBI and thus provide liquidity and stability. These banks form the backbone of the banking sector, ensuring financial stability and economic growth. By meeting specific criteria such as maintaining a minimum capital reserve and adhering to RBI regulations, scheduled commercial banks gain access to privileges like borrowing from the RBI and participation in the country’s monetary policy implementation.

Features of Scheduled Commercial Bank

Listed under the Second Schedule of the Reserve Bank of India (RBI) Act, 1934, these banks adhere to strict operational standards set by the RBI. Their features ensure stability, liquidity, and widespread financial inclusion across the country.

- Regulation Compliance: It strictly follows the regulatory guidelines of the RBI.It operates in states and territories with an all-India network of branches.

- Capital Requirements: They will have capital and reserve requirements stipulated by the RBI

Scheduled Commercial Banks Examples

- Public Sector Banks: State-owned banks where the government owns the majority shares, for instance, the State Bank of India.

- Private Sector Banks: Banks that are owned by the private sector, including HDFC Bank and ICICI Bank.

- Foreign Banks: International banks with a presence in India, for example, Citibank and HSBC.

Non-Scheduled Commercial Bank

A non-scheduled commercial bank does not appear in the Second Schedule of the RBI Act. Non-scheduled banks are generally much smaller and exert less influence compared to scheduled banks. These banks typically serve localized or niche markets, focusing on specific community needs. While they lack access to RBI’s liquidity support and clearinghouse facilities, they play an essential role in providing financial services in underserved areas.

Features of Non-Scheduled Commercial Bank

Exclusion from RBI’s Second Schedule: These banks are not listed in the Second Schedule of the RBI Act and do not qualify for certain privileges like borrowing directly from the RBI.

Limited Access to RBI Support: Unlike scheduled banks, non-scheduled banks cannot avail of RBI’s liquidity facilities such as rediscounting or short-term financial assistance.

Focus on Localized Banking: Non-scheduled banks primarily operate in specific regions, catering to the financial needs of local communities and small businesses.

Difference Between Scheduled and Non-Scheduled Commercial Bank

Scheduled and non-scheduled commercial banks form integral parts of India’s banking system. These banks differ in their structure, operational frameworks, and the regulatory guidelines they follow under the Reserve Bank of India Act, of 1934. The distinction lies in whether a bank is included in the Second Schedule of the Reserve Bank of India (RBI) Act, 1934, which determines its classification.

| Scheduled Banks | Non-Scheduled Banks |

| Backed by RBI support | No RBI liquidity support |

| Operate Nationwide | Operate locally or regionally |

| Strict compliance standards | Flexible regulations |

Types of Commercial Bank

Commercial banks are financial institutions that act as intermediaries between savers and borrowers, contributing to economic growth by efficiently managing funds. Based on ownership, scope, and area of operation, commercial banks can be classified into different types. Each type of commercial bank has a distinct role in fulfilling the varied financial needs of individuals, businesses, and governments.

Public Sector Banks

Public sector banks are owned and operated by the government, wholly or with a majority stakeholding. These focus on mass-banking and facilitating the government’s project in every respect.

Functions of Public Sector Banks:

- Provide cost-effective banking services like savings and fixed deposit accounts.

- Lend to priority sectors like agriculture, small-scale industries, and infrastructural * projects.

Private Sector Banks

Private sector banks are privately owned and operated entities. Their agenda is profit with customer satisfaction using competitive and modem banking services

Functions of Private Sector Banks :

- Provide quality customer services in personal banking, wealth management, and credit facilities.

- Examples: HDFC Bank, ICICI Bank, and Axis Bank.

Foreign Banks

Foreign banks are international banks operating in a country and providing specialized financial services with global expertise.

- It enables international trade by providing foreign exchange services and trade financing.

- Examples: Citibank, HSBC, and Standard Chartered Bank.

Regional Rural Banks (RRBs)

These are government-promoted banks catering to the rural and semi-urban areas in terms of banking activities, mainly agriculture and small-scale industries.

Features of RRBs

- Provide agricultural credit to farmers to be used on crop production, irrigation, and equipment.

- Increase savings and thrift among the people in rural areas through deposit schemes.

Cooperative Banks

Cooperative banks are those financial organizations which are instituted by a cooperative society under the Cooperative Societies Act. It emphasizes the serving of the finance of its members.Cooperative banks are unique financial institutions that operate on the principles of mutual benefit and democratic governance

Cooperative banks are owned by their members, who are also their customers. Each member has an equal say in decision-making, regardless of the capital contributed.

Structure of Commercial Bank FAQs

What is the primary role of a commercial bank?

A commercial bank is primarily a receiving and granting bank, which collects deposits from the public and grants loans to augment economic growth and stability.

What are scheduled and non-scheduled banks?

Scheduled banks are those banks that are included in the Second Schedule of the RBI Act and have the support of RBI. Non-scheduled banks operate independently without any RBI liquidity facilities.

How are cooperative banks different from commercial banks?

Cooperative banks are owned by members, and their aim is to provide credit at an affordable rate to their members. Commercial banks serve a wider market with a range of financial products.

Can non-scheduled banks be scheduled banks?

Yes, the non-scheduled banks can get scheduled bank status by fulfilling the capital and operational requirements specified by RBI.

Why are scheduled commercial banks important?

Scheduled commercial banks are important for economic development because they ensure safe banking practices, provide large-scale credit and support financial stability.