Short term sources of finance are an important means by which companies control their immediate and short-term financial needs. Such finances are generally secured for less than a year to be used to pay operational costs, cover cash gaps, and solve any pressing expenditures. It plays a crucial role in business continuation and smooth operations during unstable periods of economic fluctuations. Through short-term financing, companies guarantee that liquidity is maintained without being bound by long-term financial obligations.

Short-term financing provides businesses with the agility to respond quickly to unexpected challenges and opportunities. Whether it’s managing seasonal demand, addressing delayed receivables, or covering urgent expenses like salaries and utility bills, short-term finance acts as a financial safety net. These sources are particularly beneficial for small and medium enterprises (SMEs), which may lack access to large capital reserves. By utilizing instruments such as trade credit, bank overdrafts, and factoring, businesses can maintain operational stability, enhance their cash flow, and navigate periods of uncertainty with confidence.

Short Term Sources of Finance Meaning

Short-term finance refers to funds acquired to solve short-term financial needs and operational costs. These funds are typically borrowed for less than one year and are crucial for ensuring that businesses maintain their day-to-day operations without disruptions. They help bridge gaps caused by delayed payments from customers, seasonal fluctuations in demand, or unforeseen expenses. With short-term financing options like trade credit, bank overdrafts, and short-term loans, businesses can address immediate cash flow challenges while staying financially agile. These sources not only support operational continuity but also allow businesses to take advantage of time-sensitive opportunities without being tied down to long-term commitments.

Definition of Short-Term Financing

This is short-term finance, which is the mechanism of raising finance for a tenure of less than one year to service the immediate needs of the business. Therefore, in use, it is mostly applied for working capital purposes like inventory purchases, payment of wages, or temporary inadequacy of cash flow. The goal of short-term finance is to provide liquidity free of the long-term burden of financial liability. This makes the business operate within continuity and operational efficiency.

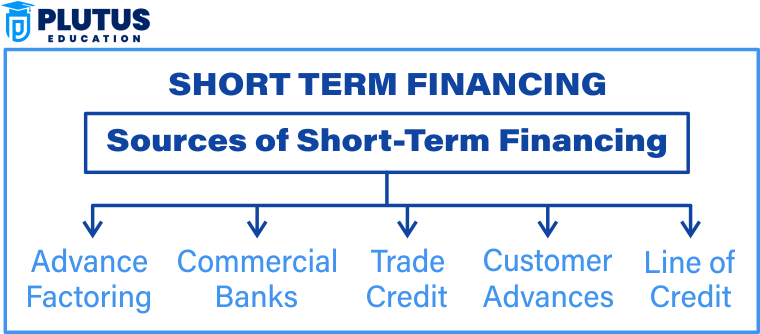

What are the Sources of Short Term Finance?

Short-term sources of finance provide businesses with funds to manage immediate operational expenses and address short-term liquidity needs. These sources are essential for maintaining cash flow, covering unforeseen costs, and supporting daily operations. Options such as trade credit, bank overdrafts, and short-term loans ensure businesses can function smoothly without long-term financial commitments. Each source offers unique benefits tailored to specific financial requirements.

Trade Credit

It refers to the terms where the seller permits the buyer to buy products or services from the seller, promising to pay back at a later date. Such a source is significantly used because the arrangement is easy and with a nil interest rate payment. The benefits of trade credit for business concern firms that purchase frequently are that they keep stock without any advance cash outgoings. For example, a wholesaler may sell inventory to a retailer on 30 30-day payables term and not expect an immediate cash flow stress on the latter’s business operations.

Bank Overdraft

A bank overdraft enables a business to withdraw money over and above that available in the account up to an agreed limit. This provides a flexible and rapid way to overcome temporary cash shortages. Overdrafts are simple to arrange and can be drawn upon many times, as long as the limit is not exceeded. For instance, a small business facing a delayed payment from a client may draw down on an overdraft facility to cover payroll or supplier obligations.

Short Term Loans

These are loans from financial institutions with a less than one-year repayment tenure. They are usually disbursed to finance inventories, service costs, or short-term requirements. There are well-formulated short-term loans that tend to have fixed repayment schedules and interest charges. Businesses usually opt for such loans when they have a specific need for a certain amount of cash for a specific, defined objective like replenishment of seasonally sensitive inventory.

Commercial Paper

Commercial paper is an unsecured promissory note issued by large firms to meet the short-term obligation. It is largely used by companies with excellent credit ratings to raise funds at a lower interest rate than that of traditional loans. Commercial papers are ideal for businesses that need large sums for the short term, like settling year-end tax liabilities or covering account receivables gaps.

Factoring

Factoring involves the selling of accounts receivable to a third party known as a factor at a discount. This means that businesses will have immediate cash flow, thus not having to wait for customers to pay. Factoring is highly beneficial to SMEs since clients may take extended periods to pay. The factor takes over the collection of payments, thus saving time and resources for the business.

Bill Discounting

Bill discounting enables businesses to sell their trade bills to a bank or financial institution at a discount value to enjoy cash immediately. This option thus assists businesses to effectively manage their working capital because it converts their credit sales to cash. The manufacturer selling to a distributor at credit can easily discount the bill with a bank to enjoy liquidity immediately.

Advantages of Short Term Sources of Finance

There are many advantages of short-term financing, and it is therefore the most commonly used method to meet the immediate requirements of a business.

- Flexibility: Short-term financing options are highly flexible, allowing the change of borrowing to current requirements by a business. They give a business the ability to react rapidly to any unanticipated financial demand or market opportunity without being burdened by long-term obligations. Such flexibility is highly useful for those industries facing seasonal variations in demand.

- Prompt Availability: Most short-term sources of finance, such as a bank overdraft or trade credit, are highly accessible. With relatively less paperwork and processing time, companies can get funds when real. In such cases of emergencies or at times when payment is delayed leading to disruption of cash flow, such immediate availability is very essential.

- Lower Costs: Generally, in terms of interest, short-term financing is cheaper as compared to long-term loans because the taken time to repay is short. The firm will reduce interest costs as it pays off its obligations. For example, a three-month loan may pay a smaller interest compared to a five-year loan for the same amount.

- Cash Flow Management Integration: Short-term financing covers short-term cash flow gaps and ensures that operations continue without interruptions. It allows companies to pay for payroll, utility bills, or raw material purchases without delay. For example, a company can use a bank overdraft to pay for expenses while waiting for client payments.

Disadvantages of Short-Term Finance

Even though short-term financing offers quick solutions, it also has some limitations that businesses must consider carefully.

- Over-Reliance Risk: It can, however, form a habit or dependency that’s hard to work with. Sometimes, businesses fall into a cycle of borrowing and subsequent repayment, putting pressure on financial stability. Overdrafts become a problem for a company depending too much on them, making it hard for the company to repay when revenues happen to decline overnight.

- High Repayment Pressure: Often short-term funding has a time constraint for the re-payment date, which puts pressure on the business entity to produce adequate cash flow within an interval. Missed deadlines could attract some punitive measures and downgrade the company’s credit score.

- Interest Rate Risk: Some of the short-term funds, like bank overdrafts, have fluctuating interest rates. Market-related fluctuation in the interest rate will increase the costs of loans without significant notice, leaving uncertainty in the corporate financial plan.

- Amount of Limited Funding: The amount of short-term financing is generally smaller compared to long-term loans. This could be insufficient for businesses that require large sums for expansion or huge projects.

Short-Term Sources of Finance Examples

Short-term sources of finance are diverse and cater to immediate financial needs, helping businesses manage cash flow and operational expenses effectively. Examples include trade credit, bank overdrafts, short-term loans, and factoring, each offering quick access to funds for addressing short-term obligations. These options are vital for ensuring business continuity during financial fluctuations.

- Trade Credit: A supplier offers 30-day payment terms for goods purchased.

- Bank Overdraft: A business withdraws ₹1,00,000 over its account balance to pay utility bills.

- Short-Term Loan: A company borrows ₹5,00,000 for six months to restock inventory.

- Commercial Paper: A large corporation issues promissory notes to raise ₹50 lakhs for short-term liquidity.

- Factoring: A business sells ₹10,00,000 in accounts receivable to a factoring company for immediate cash.

- Bill Discounting: A trader sells a ₹2,00,000 trade bill to a bank at a discount for early payment.

- Payday Loans: Employees receive advances on their paychecks to handle urgent personal expenses.

- Credit Card Advances: A business owner uses a credit card to pay for raw materials.

Short Term Sources Of Finance FAQs

What are the primary sources of short-term finance for small businesses?

Trade credit, factoring, and bank overdrafts are the most common sources of short-term finance for small businesses. These are easily accessible and can be used to meet the day-to-day requirements of running a business.

What is the difference between bill discounting and factoring?

In bill discounting, firms sell trade bills to a bank at a reduced price, and in factoring, they sell their accounts receivables to a factor. Both give a business immediate cash flow but with different purposes.

What are the short-term sources of finance in financial management?

In financial management, the short-term tools of finance range from trade credits and bank overdrafts to commercial paper tools the enterprises use when having immediate short-term liquidity or addressing operational expenses.

Why is Short-Term financing imperative for new starters?

Short-term financing helps startups manage their cash flow, cover initial operational costs, and address unexpected expenses without committing to long-term debt.

Can interest rate volatility affect short-term financing options?

This increases the cost of borrowing, especially in terms of options like overdrafts in banks or short-term loans with variable rates. The business expects such an outcome.