Different organizations typically carry out audits on various processes, but one of these audits is internal auditing. Internal auditing has a couple of disadvantages, which any organization should consider. The disadvantages of internal audit are biased findings, costs, independence, and employee resistance. The advantages accruable to internal auditing in efficiency, compliance, etc., are balanced with its shortcomings, which may inhibit the achievement of the intended purpose. Most organizations are usually stringent on issues that have to do with internal audit credibility and scope. An internal audit is more informative but may put unnecessary pressure, leading to conflicts.

What is Internal Audit?

An internal audit is an independent review of a company’s processes, controls, and financial statements. Organizations perform internal audits to check the compliance of their operational practices with laws, rules, and internal policies. The main goal of internal auditing is identifying risks, inefficiencies, and suggestions for improvement. Unlike external audits, an internal audit is performed by employees or contracted professionals within the organization. Companies have adopted the practice of conducting internal audits to improve decision-making and fraud prevention. Internal auditors will check financial records, operational processes, and compliance frameworks, and they look for anomalies.

Advantages and Disadvantages of Internal Auditing

Internal audits are done to verify and boost the transparency and efficiency of an organization’s finances and operations. At the same time, internal auditing is both an advantage and a disadvantage to organizations. The advantages and disadvantages of internal audits are critical factors determining whether this tool will remain operational; they include compliance with regulations, the incidence of non-fraud acts, and internal performance. The internal audit, however, is quite expensive, often biased, and not independent.

Advantages of Internal Audit

With internal audits, organizations can determine incorrect activity in their financial transactions and other company records before they become serious issues. The auditors ensure that the activities will be within defined procedures and ethical standards. The advantages of internal audit are:

Improves Efficiency and Productivity

Internal audits will increase an organization’s regular efficiency. They will uncover inefficiencies and provide constructive suggestions regarding improved resource management. The company can improve workflow and waste by following audit recommendations.

Technically Useful to the Application of Laws

They help an organization to follow laws by industry and international standards, as well as internal policies. It ensures that the company will be in a position never to incur legal penalties or reputational damages for non-compliance with all rules.

Facilitates Decision Making

Internal audits enhance the delivery of accurate reports concerning the financials and operations of an organization, in which the management can make important decisions to enhance the company’s overall performance.

Investors’ Confidence

Regular internal audits build investors’ confidence through induced transparency and enhanced accountability. Internal audits ascertain the worthiness of a company’s internal controls. Any weakness identified is subjected to remediation for fraud prevention and financial mismanagement.

Reduced Operational Risks

Risk identification and reduction serve the competitive advantage of a business. Internal audits document likely risks to processes, supply chains, and financial transactions and open avenues to actionable preventive strategies/testing measures.

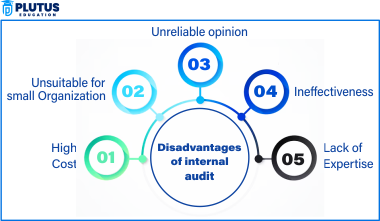

Disadvantages of Internal Audit

Although internal audits provide many advantages, they also have their disadvantages. Indeed, these limitations reduce the accuracy and efficiency of internal audits. Understanding the drawbacks of the internal audit will help organizations make the appropriate decisions regarding audit strategies.

Non-Independent

Internal auditors are internal employees; therefore, it is difficult for them to remain unbiased, as adverse reporting may come under pressure from the senior management. This, however, tends to have adverse implications for the credibility of audit results.

High Operational Costs

Internal audits generally require the appointment of skilled professionals and audit tools. These costs can become unbearable in a small-scale business, making internal audits costly. Employees typically see the internal audit as an effort to catch faults and not improve processes. It leads to incomplete information sharing in the audit, thus reducing audit effectiveness.

Limited Scope

Internal audits pertain only to some prioritized regions as per management. Because of this selective approach, the implications of other significant risks and inefficiencies in the organization may be ignored.

Possibility of Human Bias

Since internal auditors report to top management, they would not want to raise questions that may damage the leadership. Thus, it results in the credibility loss of audit reports.

Over-reliance on Internal Auditors

Companies in this category will not seek external expertise when required because they are too reliant on internal auditors. Such a case resulted in a manifested opportunity for improvement being missed.

Lack of Fresh Perspectives

Internal auditors may become too accustomed and familiar with the process and fail to spot improvement areas. External auditors provide a fresh and objective viewpoint, which internal audits tend to lack.

Scope of Internal Audit

The scope of an internal audit is defined as the areas and activities within an organization that internal auditors examine and evaluate. It includes all processes, including risk management, financials, compliance, and enterprise performance. Its extent(broad) depends on the organization’s needs and the industry.

Financial Audit

Financial audits examine an organization’s financial statements and verify that all records and transactions are accurate, complete, and conform to the relevant accounting standards and regulations. “It’s a process that essentially ensures that the financial reporting system is functioning and not subject to material errors or fraud. By detecting any differences or vulnerabilities, auditors make sure that the assumptions and accounts that the company provides to the public and investors are accurate, transparent, and in observance of legal standards.

Operational Audit

An operational audit assesses organizational processes for inefficiencies and improvement opportunities. They drive productivity and utilize resources efficiently. They suggest modifications to processes, mechanisms, and controls that can result in greater efficiency and fewer costs.

Compliance Audit

A compliance audit assesses the extent to which an organization has followed laws, regulations, industry standards, and internal policies. Auditors can evaluate processes and practices for violations or compliance issues and recommend correcting these problems. Compliance audits help them prevent legal punishment, ensure minimal organizational risk, promote ethical practices, and work within limits while maintaining dignity and market.

Information Technology (IT) Audit

An IT audit evaluates how well an organisation’s IT systems covering data protection, software, and cybersecurity perform as planned. The audit procedure also ensures that the technology infrastructure collaborates with the organization’s needs and runs securely. Auditors determine potential threats and provide suggestions for improvement to increase security, safeguard sensitive data, and ensure the technology systems are effective, dependable, and consistent with business goals.

Difference Between Internal Audit and External Audit

To cater to different purposes, internal and external audits have to differ in scope, objectives, and methods of execution. Internal audits are conducted within the organization to enhance processes, while external audits are independent assessments conducted by third-party professionals.

| Aspect | Internal Audit | External Audit |

| Purpose | Improve internal processes and controls | Provide an independent audit opinion on financial statements |

| Conducted By | Employees or outsourced professionals | Independent auditors |

| Frequency | Regularly throughout the year | Annually or as required |

| Scope | Based on management priorities | Covers entire financial statements |

| Compliance Focus | Internal policies and procedures | Legal and regulatory compliance |

| Reporting | Reports to management | Reports to shareholders and regulators |

| Independence | Less independent | Completely independent |

| Cost | High for small businesses | Usually fixed fees for external auditors |

| Objectivity | Can be biased | Completely objective |

| Legal Requirement | Not mandatory | Required by law for many companies |

Disadvantages of Internal Audit FAQs

What is internal audit?

Internal audit is the review through which a company inspects its financial and operational processes to assure compliance with policies, regulations, and best practices. It is through the use of internal audits that businesses will detect fraud, ascertain risks, and improve their efficiencies.

What are the disadvantages of internal audit?

The disadvantages of internal audit include lack of independence, high costs, employee resistance, and the possibility of bias. Most likely, the scope of internal audit is limited, and the audit consumes a considerable amount of time, all of which decreases productivity.

What are the advantages and disadvantages of internal audit?

The advantages and disadvantages of internal audit affect its effectiveness. The advantages could include fraud prevention, regulatory compliance, and greater efficiency.

What is the difference between internal audit and external audit?

The reasons for the difference between internal and external audits are the differences in purpose, execution, and independence. One internal audit would be an effort to improve internal control, whereas an external audit would give an independent opinion on financial statements.

Why do companies do internal audits?

The simple answer is that it would help the firms identify incidences of fraud, make processes efficient, and ensure compliance with regulatory practices, among other benefits of internal auditing. Regular audits serve as investigative tools to point out all possible risks of committing financial mismanagement.