A thorough external audit is an outside examination of a company’s financial records and workings. It handles the correctness of the financial statements and their lawful and regulatory correspondence. External auditors stand for audit results and reconciliations fulfillment based on determinate standards and deliver an external audit report.

The external audit processes are jurisdiction-driven and include various external audit procedures like risk assessment, collection of evidence, and reporting. Audits must take place to ensure the accountability and transparency of the company. Audit firms, in turn, are often appointed to provide the audit is done professionally. Internal audits, on the other hand, are not independent of the company. External audits consist of an independent assessment of the company’s financial books.

What is External Audit?

External audits denote independent assessments of the financial statements, internal controls, and compliance with laws concerning the external auditor without personal involvement with the company. This audit aims to present an impartial viewpoint on whether the company’s financial reports present a true and fair view of its financial position.

The external audit follows universally accepted external auditing standards such as ISA and GAAS. These standards promote uniformity and reliability in the audit process. External auditors trace financial transactions and accounting records and processes for conformity with the expected standard.

External auditing augments the trust of outside stakeholders such as investors, creditors, or regulators. This will include a report from an outside auditor’s review that he would include in formulating opinions on the company’s financial health.

Objectives of External Audit

The external audit objectives mainly require accuracy, transparency, and legal compliance. The auditors inspect the financial statements to ensure they follow accounting principles.

Financial Accuracy

An external audit that aims to judge financial statements‘ accuracy and locate material misstatements should any be found. Financial recording will then be in the form of all these procedures related to accounting standards and principles.

Detecting Fraud and Errors

External auditors usually diagnose and assess financial transactions for misstatements, fraud, and accounting errors. They have their suspicious patterns looked into, internal control systems assessed, and corrective actions recommended.

Strengthening Corporate Governance

By securing management’s ethical business practice in external auditing, the functions of the Auditors would check compliance with the corporate governance policies to ensure the organization’s transparency and accountability.

Diagnose Financial Transactions

When you conduct an entire investigation concerning fraudulent misrepresentation, the errors or the very smallest mistakes in accounting can easily be detected, where the external auditors catch any misstatement, fraud, or accounting errors. They try to analyse suspicious patterns, assess the internal control system, and make corrective recommendations.

Ensure Regulatory Compliance

Companies must comply with financial regulations, tax laws, and industry standards. The auditors variedly verify whether the organisation follows legal requirements.

Provide Credibility to Stakeholders

Audited statistics present the viable decisions of the investors, creditors, and shareholders. A clear external audit report raises the confidence of the stakeholders in the company’s financial stability.

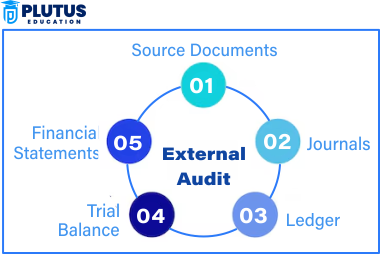

External Audit Process

The external audit process includes several steps, from planning to report finalization; among these, any one step must be followed with a definite system that allows the auditors to review the company’s financial information with reasonable assurance.

1. Audit Engagement Plans

Every Single External Auditor gets to understand the entity, its operations, financial reports, and risk items at the beginning of the audit. Auditors collect preliminary information about the company’s business model and accounting policies. An external audit checklist may be prepared in this phase regarding the major subjects being subjected for consideration.

2. Risk Assessment

The account work in these key risk factors would interfere with a true and fair view. They pinpoint areas for potential fraud, error, or misrepresentation. Thus, this is working to emphasize high-risk transactions and accounts more.

3. Evidence Gathering

External auditors collect their evidence through various external audit procedures, such as verifying documents, interviewing people, testing transactions, etc. They check invoices, contracts, bank statements, etc., on a selecterecognised basis to ensure that all financial activities are currently recognized.

4. Internal Control Testing

Auditors test the internal controls to control fraud and error. They verify whether the company performs approval procedures and segregation of duties. Weakened internal controls enhance the chances of financial misstatement.

5. Issuance of the Audit Report

External auditors finalise their work by preparing a report on an external audit. The report states their findings and the opinion of the external audit. Their opinion is on the credibility of the presentation and reliability of the statements. The company submits its report to interested parties and regulatory bodies.

Independence of External Auditors

The independence of external auditors is essential for informed audits to be conducted. The auditors should, however, not have any financial or personal relationships with the company under audit. A conflict of interest can impair the credibility of an audit.

Independence of the External Auditors

Elimination of Conflicts of Interest

To be independent of any financial or personal relationships with the business, external auditors should not be related to any of these factors. Any conflict of interest will then affect the objectivity and credibility of the audit conducted.

Follow Ethical Standards

Auditors must follow the professional codes of conduct set forth by the regulatory bodies. The ethical guidelines help to ensure that he performs an unbiased assessment and that he will adhere to integrity throughout the auditing.

Resist External Influence

Companies are not involved in interfering with external audit processes or manipulating audit findings. Auditors would receive no incentives or gifts nor be offered jobs from the company to maintain an independent status.

Enhance Trust in Financial Reporting

Independent auditors give credibility to the investors’ and regulatory bodies’ fair financial reporting. Auditor independence makes it possible for the financial statements to be true and fair.

Legal and Professional Compliance Guidelines

External auditors have stringent independence requirements as required by the regulatory authorities. This kind of regulation or obligation for the company and auditor will open the process while ensuring users’ credibility of financial audits.

Importance of External Audits

External audits are important for more than just verifying financial value. Independent audits assert benefits in a multiplicity to the companies.

- Builds Trust in Investors: An external audit helps build trust between investors and stakeholders. Public observation of the current financial review helps assure them that the financial statements would convey accurate reports.

- Law mandates: Most jurisdictions would impose the need for an external audit in a business to see compliance with the tax rules, financial regulations, and corporate governance policies up to non-compliance.

- Identify Weaknesses in Internal Control: An external audit will highlight gaps in managing these internal finances. Include all recommendations for improvement in risk management, fraud detection, and operational efficiencies.

- Business Growth: A clean external audit report is usually a requirement that sets aside businesses demanding loans from investors or trying to expand operations. Lenders and financial institutions prefer to work with transparent companies financially.

- Financial Risks Reduced: External audits assess a company’s financial health and spot potential risks. Thus, by resolving the risks early, businesses can avoid financial mismanagement, fraud, and operational inefficiencies.

External Audit FAQs

1. What is an external audit?

An Independent examination of the company’s financial record is called an external audit. It ensures that financial statements are true and accurate in analysis and comply with the regulations. The external auditors analyze transactions, accounting policies, and internal controls before Forming an opinion in the audit report.

2. What distinguishes external audit from internal audit?

An outside audit certifies that financial accuracy is independent reports by other firms. On the other hand, an internal audit is a risk and efficiency assessment by the in-house team. Organisations give an unbiased evaluation of funds. Organisations help refine the operations of the organization.

3. What is the organisation of the external audit?

Auditors outside will audit an organization alone, planning, assessing risk, recruiting evidence, testing internal control, and report issuing. They would check the financial statements and transactions according to the laws to get their opinion before doing so.

4. State the Importance of External Audit for Business.

Credibility, legal compliance, fraud detection, and management of damage to businesses are ofexternall audit importance. Usually, such companies attract foreign investment and even approve government institutions having a good external audit report.

5. State the External Audit Limitations.

The probable biases of auditors and the sampling procedures also mark some limitations of this study in the detection of management fraud. Nevertheless, external audits become crucial in the integrity of financial reporting.