Financial statement assertions refer to specific claims made by management. It’s regarding a firm’s financial statements. These assertions are put to validate that the financial statements give an accurate and fair image of the company’s financial position. It affords a precise representation of its affairs. They include occurrence, completeness, accuracy, cut-off, classification, presentation, rights and obligations, and valuation. The auditors then use these assertions to determine whether or not there exists any material misstatement in the financial statement. If the statement conforms to the accounting principles laid down.

Financial statement assertions are, therefore, of great importance to all auditors, investors, and regulators. They guide the working of auditors. They guide the disclosure of errors or frauds potentially found in financial statements. Every firm must observe such assertions to be transparent and reliable.

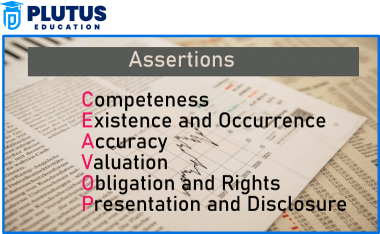

Financial Statement Assertions

Financial statement assertions are statements that management makes. It is about recognizing, measuring, presenting, and disclosing financial information. This information is present in the financial statements. These assertions create a base for the auditors to assess the reliability of financial reports.

When preparing financial statements, companies must ensure their financial information is accurate. The financial statements are also evenly present. Auditors determine audit assertions of financial statements. It is to qualify the info presented as precise. It must fall under the ambit of the applicable financial reporting framework. Assertions are some benchmarks to which auditors apply their audit. It is the procedure to seek out errors, frauds, or misrepresentations.

It is a generalized description of some types of assertions. The properties of the financial statements may differ. Some of them would be concerned about ascertaining whether or not an actual transaction happened at all. Others look at the boundary to determine whether or not an event or transaction qualifies for the statements. These assertions help provide a checks-and-balances-like system for financial reporting.

Types of the Financial Statement Assertions

- Complete Assertion- Ensures that all the financial transactions associated with that time are considered.

- Accurate Assertion- Ensures that all financial transactions during that period are recorded with the correct figures.

- Cut-off Assertion– Ensure transactions are related to the correct period.

- Classification Assertion– Ensure that the transactions are allocated to the right accounts.

- Presentation Assertion- Assurance of how financial information on relevant rules is represented.

- Rights and Obligations Assertion- Assurance that the company’s assets and liabilities are possessed.

- Valuation Assertion- Ensure that assets and liabilities are recorded with appropriate values.

Occurrence Assertion

The occurence assertion states that the events that have taken place have occurred. This assertion acts as a safeguard as well. It is to make sure that management has not overstated revenue. Or not overstated assets by manipulating transactions. The auditors validate the occurrence of an event. It checks supporting documents such as invoices, receipts, and contracts. Mainly to confirm that transactions recorded in accounts did come to be.

A company manipulates its financial statement by recording sales before goods are delivered to the customer. The occurrence assertion in auditing may detect the blatantly wrong occurrence made by the company. It may be to mislead the investor and authority.

Specific audit procedures are followed for financial assertion testing. I will review contracts, scrutinize invoices, and verify the transactions with third parties. They are performed to test for occurrence. However, where differences are detected, the auditors may conclude that the financial statements are misstated.

All organizations should have established and maintain an internal control system within their frameworks. It does not allow and permit transactions in the financial statements without appropriate verification. Primarily, it aims at determining whether it happened or not.

Completeness Assertion

The completeness assertion ensures that all transactions and other events that should be included in the accounting records have been included. This assertion protects against management understating liabilities. It protects from understating expenses in financial statements to make them look better than they are. A company may decide not to record certain expenses, artificially inflating profits. If a business doesn’t include all liabilities, the investor may think the company is in a much stronger financial position than it is. Auditors turn to completeness assertion in auditing to catch such misstatements.

In straightforward terms, Auditors substantiate completeness through substantive procedures for financial assertions. They trace transactions from source documents. To financial statements, corroborating records against external confirmations from suppliers, lenders, customers, etc.

Internal control systems provide defense against such assertions not being met. Companies should reconcile accounts periodically. It must perform internal audit procedures to ensure that records are being checked against one another. It will help ensure completeness and reduce the likelihood of record error or fraud.

Accuracy Assertion

The accuracy assertion ensures all recorded transactions and events are practical and appropriate. It ensures they are presented that way in the financial statements. Because errors in the economic data could lead users astray in their business decision-making, Accuracy is key, as tiny errors could lead to material misstatements. For instance, missing the details on a sales discount or a tax on a particular transaction could affect its financial reporting. The accuracy assertion requires that any financial transaction reflects appropriately its values.

Accuracy is key, as tiny errors could lead to material misstatements. For example, missing details about a sales discount or a tax on the specific transaction may take its financial reporting into new realms. Therefore, the accuracy assertion is that all financial transactions must properly reflect the amounts.

For accuracy is key, since even to the smallest extent, errors may lead to material misstatements. Accounting departments operate regularly and do reconciliations to achieve more accuracy along with reviewing and approval processes.

Accuracy is key since usually even the smallest errors may lead to material misstatements. Regularly running an accounting organization, performing reconciliations, and maintaining review and approval procedures are also helpful in guaranteeing greater accuracy.

Cut-Off Assertion

The cut-off assertion asserts that transactions have been captured in the proper accounting period. Misstatement of the financial results due to manipulation by the delayed recognition of revenue or expenses is countered by this assertion.

For instance, the company may postpone recognizing an expense to bolster income in the current period instead of an expense. On another account, the company recognizes revenue without affecting sales. All of those procedures are distorting the financial statements and deceiving stakeholders. The cutoff assertion helps prevent these misstatements.

The cut-off will be partially verified by comparing the transactions’ initiation with their dates in the financial statements. These dates included all relevant invoices, receipts, and shipping documents, ensuring that transactions were recorded in the correct period. Strong closing processes will also augment the cut-off procedures at month-end and year-end. Specifically, periodically reviewing ell-defined accounting policies ensures compliance with this cut-off assertion.

Classification Assertion

This assertion indicates the proper classification of all records relating to transactions in appropriate accounts. Any misrepresentation of transactions could result in distorted financial statements for the company and could, in turn, affect the ratios derived from the accounting figures. For example, capital expenditure classified as an operating expense would misstate profits. It refers to that notion inscribed in audit works, eradicating from the auditor’s mind that every transaction recorded should belong to the correct category according to its nature.

Auditors thus confirm classification by examining the general ledger accounts and financial statements, assessing account structure journal entries, and comparing accounting policies. Auditors also rectify misclassifications through the adjustments that take place during auditing. Therefore, the company must comply with its accounting policies, train its employees, and conduct internal audits to keep all transactions classified appropriately.

Presentation Assertion

The presentation assertion ensures that the financial statements clearly and duly present the relevant accounting standards. This assertion takes on disclosures, classifications, or explanatory notes.

Financial statements should provide complete information in a form consumable by users. The presentation and disclosure assertion ensures transparency by requiring the company to disclose significant accounting policies, contingencies, and risks.

Auditors assess presentation by examining financial statement layouts, disclosures, and underlying documents. They then check the requirements set by the relevant reporting standards, either GAAP or IFRS.

The presentation requirements will be satisfied by companies through consistent financial reporting and adherence to its disclosure guidelines.

Rights and Obligations Assertion

The rights and obligations assertion also assures that a firm’s recorded assets and liabilities belong to such an entity. It prevents misrepresentation regarding the ownership of assets or liabilities.

For instance, if the company chooses not to record an asset that is not owned or fails to exclude a liability against which it has a claim, it has violated the rights and obligations assertion. Auditors thus validate these rights and obligations by reviewing legal dossiers, contracts, and loan agreements.

Companies must maintain proper documentation and periodically review ownership records to implement this assertion fully.

Valuation Assertion

The valuation assertion ensures that an asset or liability has been recorded appropriately. A false valuation may mislead an investor and adversely affect financial decision-making.

For example, an inflated asset value tends to exaggerate measures of financial strength, while giving low values to liabilities results in overstating profit. Valuation assertions ensure that the financials are accurate.

Auditors challenged valuation by assessing their financial model, market data, and supporting documents. They ask themselves whether the assumptions applied in their valuations were reasonable.

Companies must maintain consistency in the valuation methodology and the implementation of accepted standards while also engaging in periodic asset revaluations.

Financial Statement Assertions FAQs

1. What are financial statement assertions?

Management makes claims about the financial statements and uses these assertions to assist auditors in verifying the financial reports’ correctness, completeness, and fairness.

2. Why are they important?

They ensure the accuracy accuracy ability of financial statements for investors, regulators, and auditors to detect errors, fraud, and misstatements.

3. What is accuracy assertion vs. valuation assertion?

The accuracy assertion ensures that all transactions are accurately recorded, while the valuation assertions state that all assets and liabilities are valued correctly.

4. On what basis do auditors verify financial statement assertions?

Auditors substantiate these assertions through substantive procedures, including documentation review, transaction testing, and confirmation with a third party for the balance.

5. What is the role of financial statement assertions in auditing?

They provide a conceptual framework against which auditors can determine whether the financial statements are free from material misstatement.