Every occupation has ethics that form the very basis of trust. The basic principle of professional ethics states that people are responsible for acting in a manner. That is honest, decent, and accountable regarding their workplaces and professions. These applied principles give professionals the capability. If not, the right to exercise discretion in judgment. Justly treating one another or any other party that may be adversely affected by their actions. Ethics create a stronghold in finance, law, healthcare, and education. Professional ethics always account for fair treatment and accountability. However, one must also show respect to others involved. To build faith and transparency, professionals must operate under ethical business principles. Each field has a set of professional ethics, which lay down moral guidelines in the workplace. Understanding the pillars of professional ethics assists individuals in fulfilling their responsibilities and making the right ethical choices in times of trouble.

Nature of Professional Ethics

Professional ethical principles ensure that their application is considered in his trade. These essential principles are oriented around conduct and choice, which guide a professional to uphold the highest moral and ethical standards. Ethics determine how professionals interact with each other at work and serve clients. The absence of professional ethics leads to a malfunctioning system for businesses. Also,o for the institutions.

Importance of Professional Ethics

The foundation of professional ethics guides those who enter the profession to act. To act responsibly and ethically. These principles govern human behavior and decision-making by high moral and ethical standards. In other words, ethics determine how people work, interact with their peers, and perform client services. Shorn of a guiding ethical foundation, businesses and institutions cease functioning normally. Ethical action inspires trust, transparency, and accountability. These are vital in all fields to preserve professionalism. Medicine, law, finance, and engineering are some fields within which the profession must follow ethical guidelines. To ensure fairness and credibility in its conduct.

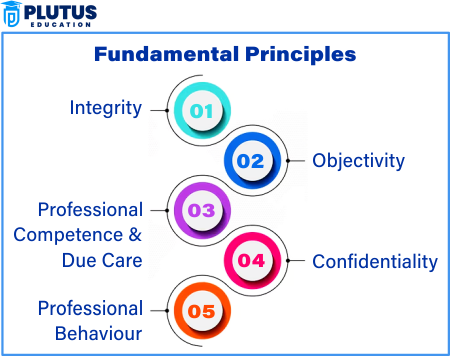

Fundamental Principle of Professional Ethics

A profession entails a unique set of ethical responsibilities to retain the credibility provided to it by society. Ethics are fundamental to honesty and fairness when carrying out a duty. The code of ethics varies among occupations but generally shares the same core values. These core values foster an environment. It discourages professional misconduct, conflict of interest, or other unethical conduct. It safeguards the interests of the concerned professionals’ clients, patients, and stakeholders.

Integrity in Professional Ethics

Integrity is considered the core or one of the significant values in the framework of professional ethics. It requires professionals to be completely honest and transparent in their dealings. Physicians must render honest diagnoses and refrain from imposing unnecessary therapies. Accountants must relay information on an organization’s financial integrity without manipulation. Lawyers must present a fair picture of the situation and let the court decide.

Decisions of Ethics in Business

In business ethics, professionals must explore the situation thoroughly before taking equitable and responsible actions. Corporate professionals find themselves in questions demanding ethical decisions. For instance, a financial analyst might have insider information but cannot use it for his consumer interest. For example, managers can cut costs or care for their subordinates. Ethical decision-making entails weighing decisions’ effects on stakeholders. In compliance with the law and integrity of the organization as a whole. Prevents unethical practices such as fraud, bribery, and corruption.

Workplace Ethical Guidelines

From the organizational perspective, these ethical principles and guidelines have also been designed for the workplace. It will help inform employees about professional, dignified, and civil behavior. In contrast, guidelines also express behavior expectations to effect favorable discipline. It enables a positive work environment. Enterprises established their ethical policies covering harassment, discrimination, and conflicts of interest, among many other specific areas, which would be referred to as they ought to be within the rules and report the violation. These include the guidelines for interpersonal relationships among employees in the workplace, thus ensuring the employees can socialize respectfully and professionally. Strong ethical guidelines encourage teaming between strong work partnerships and enhance the illusion of improved productivity and, eventually, employee satisfaction. They would promote a culture of fair respect towards one’s self and the other people as a whole within the organisation.

Code of Professional Ethics

A code of professional ethics is a procedural list of rules and principles that an individual must follow. They help continue professional conduct maintenance by making employees and employers accountable. Each industry’s ethics code lays down its professionals’ expected behaviors and ethical responsibilities. From here, ethical codes play the role of reducing unethical practices while building trust within a profession.

Professional ethics are defined to allow the smooth functioning of an organization or business operation. Employees generally have the tools for ethical decision-making and good integrity during working hours. Accountants follow the moral guidelines that ensure accurate financial reporting against fraud and misrepresentation. The confidentiality and fairness standards that tort lawyers follow are to ensure that justice prevails. Doctors operate within medical ethics, prioritizing patients’ rights and access to equal healthcare. Engineers have ethical codes to ensure public safety and sustainable development in all their projects.

Ethical Behavior at the WorkPlace

Ethical behavior at the workplace includes employees’ actions in a very professional environment. This includes treating colleagues and clients respectfully, having honest communication with people in the workplace, and being by workplace policies, among other things. Companies that thrive on ethical behaviors encourage their staff to create an environment where trust and fairness become the basic foundation of justice. Ethically behaving employees contribute significantly to bringing about a positive working environment.

Respecting Colleagues and Clients

Employees must respect their colleagues and clients alike, with gentility and professionalism being the hallmarks of a healthy work environment. Exclusion, harassment, or unfair treatment lowers morale and distorts workplace culture. Companies imbued toward diversity and inclusion gain returns in team dynamics and employee engagement. Respect also equates to those traits that foster colleagues communicating, communicating actively, listening, communicating, and giving credit.

Honesty and Transparency

Honesty is a critical consideration in workplace ethics. Employees must give meaningful and truthful information and avoid misleading behavior toward colleagues or clients. Transparency builds trust within the organization when there is decision-making and communication. Instead, a company might be upfront about financial difficulties instead of glossing over the issue. Honesty matters concerning financial reports, customer relations, and project administration. A company that adheres to honesty builds long-standing credibility and loyalty from customers.

Accountability and Taking Responsibility

Employees are to be held accountable for what they do and what they decide to do. This implies that when employee is held responsible for something they have done, they must own up to their mistakes, learn from them, and not pass off the blame on someone else. Where accountability exists, it draws more towards creating a working environment where people want to work. Employers have a role in creating accountability, highlighting clear expectations, and providing constructive feedback. Accountability catalyzes efficiency and inspires employees to become responsible in discharging their duties to deliver results.

Adherence to Workplace Policies

Workplace policies exist to maintain order and professionalism. Employees are supposed to comply with the company rules on confidentiality, conflict of interest, and conduct in the workplace. For instance, an employee with customer data must respect privacy and not disclose sensitive data. Those companies that uphold ethical policies prevent unethical activities such as fraud, bribery, and favoritism. The adherence to company policies gives credence to a structured and just working environment.

Encouragement of Ethical Leadership

Leaders have a big responsibility concerning the promotion of ethical behavior. Ethical leadership sets the tone for the whole corporation. If managers operate with integrity, employees follow suit. Ethical leaders promote teamwork, fair decision-making, and good communication. Ethical leadership also recognizes and rewards employees for ethical conduct. Ethical leadership translates into fewer conflicts, higher employee retention, and a better culture in the workplace for the businesses that foster it.

Relevance to ACCA Syllabus

Ethics and professional behavior are core components of the ACCA syllabus. These ethics and professional behavior are loosely focussed in isolation, as seen in the Strategic Business Leader (SBL) and Corporate and Business Law (LW). ACCA expects candidates to apply the integrity of objectivity, professional competence, confidentiality, and professional behavior in executing their duties.

Fundamental Principle of Professional Ethics ACCA Questions

- Which of the following is NOT one of the fundamental principles of professional ethics under ACCA’s Code of Ethics and Conduct?

A) Integrity

B) Objectivity

C) Advocacy

D) Professional Competence and Due Care

Ans: C) Advocacy - What does the principle of Objectivity in ACCA’s Code of Ethics require from a professional accountant?

A) To prioritize employee yer’s interest above everything

B) To remain free from bias, conflicts of interest, or undue influence

C) To maintain absolute confidentiality under all circumstances

D) To always disclose personal financial interests to clients

Ans: B) To remain free from bias, conflicts of interest, or undue influence - Which ethical principle ensures that an accountant keeps client information confidential unless required by law?

A) Integrity

B) Objectivity

C) Confidentiality

D) Professional Competence

Ans: C) Confidentiality - Under ACCA’s ethical framework, what should an accountant do if they identify a conflict of interest in their work?

A) Ignore it unless a client complains

B) Disclose the conflict and take steps to mitigate it

C) Withdraw from the engagement immediately

D) Inform their employer but not the client

Ans: B) Disclose the conflict and take steps to mitigate it - Why is “Professional Behavior” a core principle in ACCA’s Code of Ethics?

A) It ensures accountants avoid any action that discredits the profession

B) It requires accountants to always agree with clients

C) It focuses on promoting self-interest above public interest

D) It allows accountants to prioritize employer benefits over regulations

Ans: A) It ensures accountants avoid any action that discredits the profession

Relevance to US CMA Syllabus

The Certified Management Accountant CMA syllabus emphasizes ethical behavior in financial decision-making and internal control frameworks. The IMA Statement of Ethical Professional Practice includes principles such as honesty, fairness, objectivity, and responsibility. Ethical compliance is tested in corporate governance, risk management, and financial statement analysis.

Fundamental Principle of Professional Ethics US CMA Questions

- Which ethical standard in the IMA’s Statement of Ethical Professional Practice focuses on maintaining professional expertise and continuous learning?

A) Integrity

B) Competence

C) Objectivity

D) Confidentiality

Ans: B) Competence - What should a CMA do if they discover a serious financial misstatement their manager refuses to correct?

A) Ignore it to maintain good workplace relationships

B) Report the issue to external auditors or regulators

C) Resign without disclosing the reason

D) Discuss it informally with colleagues

Ans: B) Report the issue to external auditors or regulators - Which of the following is a core ethical concern for management accountants under the IMA guidelines?

A) Maximizing revenue at any cost

B) Providing misleading financial reports to meet targets

C) Maintaining integrity and avoiding conflicts of interest

D) Supporting aggressive tax avoidance strategies

Ans: C) Maintaining integrity and avoiding conflicts of interest - If a management accountant is pressured to manipulate cost data for financial reporting, which ethical principle is being violated?

A) Fairness

B) Objectivity

C) Professionalism

D) Independence

Ans: B) Objectivity - Under the IMA’s Code of Ethics, what must a management accountant do when faced with an ethical dilemma?

A) Immediately report it to the media

B) Seek guidance from relevant authorities

C) Ignore it if it benefits the company

D) Accept the decision made by senior management

Ans: B) Seek guidance from relevant authorities

Relevance to US CPA Syllabus

The CPA (Certified Public Accountant) exam covers professional ethics under the AICPA Code of Professional Conduct. US CPAs must uphold integrity, maintain objectivity, and ensure compliance with GAAP, SEC, and PCAOB regulations. Ethics-related topics are tested in the Regulation (REG) and Auditing (AUD) sections.

Fundamental Principle of Professional Ethics US CPA Questions

- Which AICPA Code of Professional Conduct principle emphasises acting in the public interest?

A) Confidentiality

B) Integrity

C) Professional Skepticism

D) Self-Interest

Ans: B) Integrity - A CPA is auditing a company where they hold financial investments. Which ethical principle is at risk?

A) Integrity

B) Confidentiality

C) Independence

D) Objectivity

Ans: C) Independence - What must a CPA do if they uncover fraudulent activities during an audit?

A) Ignore it unless specifically asked about it

B) Immediately report it to law enforcement

C) Discuss with the company’s management and escalate if unresolved

D) Adjust financial statements without disclosure

Ans: C) Discuss with the company’s management and escalate if unresolved - Under the AICPA ethical code, which scenario is considered a breach of professional conduct?

A) A CPA accepting a reasonable audit fee

B) A CPA promoting financial transparency

C) A CPA accepting gifts that impair objectivity

D) A CPA complying with auditing standards

Ans: C) A CPA accepting gifts that impair objectivity - Which fundamental principle requires CPAs to comply with relevant laws and avoid discrediting the profession?

A) Due Care

B) Professional Behavior

C) Advocacy

D) Public Interest

Ans: B) Professional Behavior

Relevance to CFA Syllabus

The CFA (Chartered Financial Analyst) program emphasises ethics in investment management and financial analysis. The CFA Institute Code of Ethics and Standards of Professional Conduct includes principles such as loyalty, prudence, diligence, and fair dealing to protect investors and market integrity.

Fundamental Principle of Professional Ethics CFA Questions

- Which ethical principle is a core focus of the CFA Code of Ethics?

A) Prioritizing client interests over personal gains

B) Following employer instructions without question

C) Manipulating market information for profit

D) Encouraging insider trading

Ans: A) Prioritizing client interests over personal gains - A CFA professional must disclose conflicts of interest to clients. This falls under which standard?

A) Fair Dealing

B) Loyalty and Prudence

C) Independence

D) Confidentiality

Ans: B) Loyalty and Prudence - What action violates the CFA ethical standard of Market Manipulation?

A) Trading based on publicly available information

B) Engaging in fraudulent activities to influence stock prices

C) Conducting due diligence on investments

D) Providing unbiased research reports

Ans: B) Engaging in fraudulent activities to influence stock prices - Which is NOT a CFA Code of Ethics principle?

A) Integrity

B) Loyalty

C) Self-Promotion

D) Fairness

Ans: C) Self-Promotion - Under CFA’s Code, misrepresenting investment performance results violates which standard?

A) Fair Dealing

B) Professionalism

C) Misrepresentation

D) Duty to Clients

Ans: C) Misrepresentation