Goodwill is the most widely used term in commercial and accounting vocabulary, yet it baffles most students. It is anything greater than a basic asset or money in tangible form owned by a target company. Goodwill is the reputation, loyalty of customers, and brand value that the business has developed over time. In accounting terms, goodwill becomes extremely significant when one firm buys out another. For commerce students, knowledge about goodwill is crucial since it is profoundly used in business valuation, mergers, and acquisitions.

Goodwill Definition

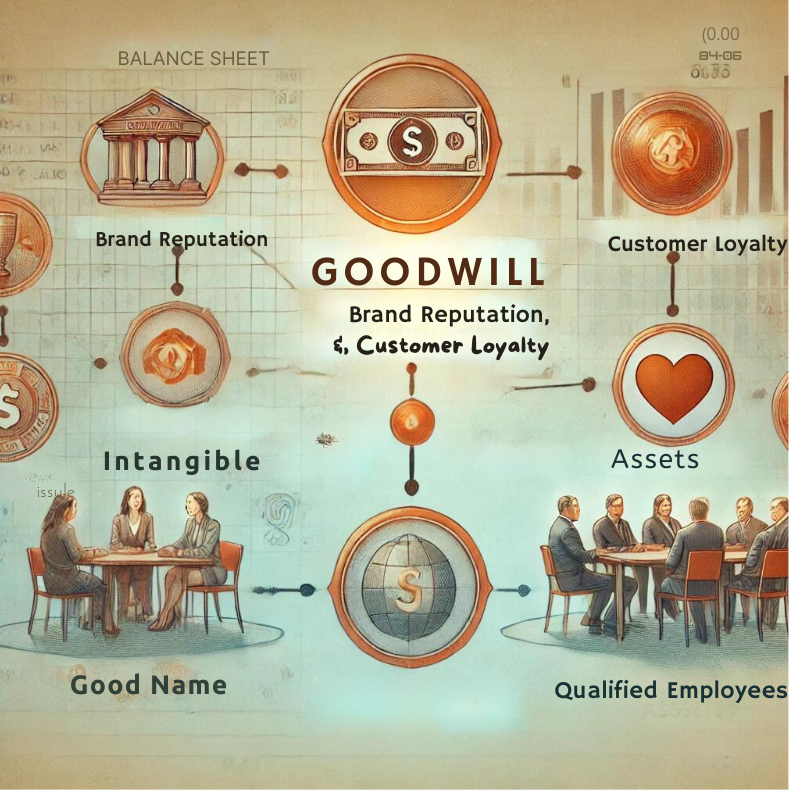

Goodwill is an intangible asset that arises when a company buys another business entity at a price greater than its book value. It can be said to be the premium a buyer is willing to pay for non-physical assets like a company’s reputation, good customer relationships, or brand value.

Goodwill is considered to be an intangible asset. It is a sum of everything that carries additional value to a business beyond just the mere aggregation of tangible or identifiable assets. Examples include brand reputation, customer loyalty, qualified employees, and good supplier relationships.

What is Goodwill Meaning in Accounting?

Goodwill meaning in accounts is an intangible asset that accounts for the excess purchase price of another company. Goodwill accounting includes proprietary or intellectual property, brand recognition, and other aspects of a company that are valuable but not easily quantifiable.

Goodwill does not happen overnight. Goodwill is acquired by a business when it produces adequate operating results, which are achieved by the merits of an entity, its assets, or by simply existing reputation and customer satisfaction over time. It happens without any effort on the part of the entire business when they expand and strengthen their relationships with customers, suppliers, and personnel.

Goodwill is shown in the firm’s financial statements only when the firm is buying another firm. This means that when the firm is thriving on its own, its value in terms of goodwill is not shown. Only when some other firm buys it does goodwill appear in the journal entry.

Methods of Valuation of Goodwill

Goodwill is the value of a firm’s brand name, customer relationships, employee relations, and any patents or proprietary technology. The calculation of goodwill is one of the most important calculations performed during mergers, and acquisitions, and to determine the fair value of a firm. There are numerous techniques to calculate goodwill:

1. Average Profits Method: In this method, the goodwill is calculated by averaging the profits from previous years and multiplying this by a predetermined number of years.

2. Super Profits Method: Super profits are calculated by subtracting normal profits from actual profits. The result is then multiplied by a certain number of years or a capitalization rate.

3. Capitalization Method: This method capitalizes the average or super profits using a normal rate of return on capital employed in a similar business.

4. Annuity Method: Future super profits are discounted to their present value considering that they will reduce with time.

How is goodwill calculated?

There is a very simple formula widely applied in the goodwill calculation. It says:

Goodwill = P – (A + L) or

Goodwill = Purchase Price− Net Fair Value of Identifiable Assets

Here,

P is the price paid to buy the company,

A is the fair price of the assets of the company, and

L is the fair value of the company’s liabilities.

As per Accounting Rules, partners need to figure out their firm’s goodwill for these reasons:

- Time of admission of a new partner.

- A present partner dies or withdraws.

- The partners wish to dissolve the firm.

- The partners agree to share profits differently.

In all these cases, the partners must first compute and share the existing goodwill before doing anything else.

Example:

If Company ABC buys Company EFG for $500,000 and the total value of Company EFG’s assets is $400,000, then the amount of goodwill would be $100,000.

Types of Goodwill

In accounting, goodwill refers to the value intangible that a business possesses due to its reputation, customer loyalty, brand, or other factors that result in higher profits compared to competitors. The kinds of goodwill mainly vary based on the circumstances under which it arises. In the business world, there are usually two kinds of goodwill.

Purchased Goodwill

Purchased goodwill results when a new business buys into another and pays more than the fair value of its net identifiable assets. Such excess is represented as goodwill in the acquirer’s balance sheet. It is the premium paid over the net value of the identifiable assets and liabilities of the company.

Try to think of this analogy: You buy more than the physical assets and debts. You pay for the reputation of the business, customer relationships, brand recognition, and other intangible assets that have contributed to the value of the target company.

Inherent Goodwill

The goodwill created by a business over the years. However, this form is not accounted for in the books of account unless there is an acquisition. Although inherent goodwill is somewhat distinct from the rest, it is the value that a business possesses besides the fair value of its identifiable assets. Different from purchased goodwill, which has emanated through a transaction, inherent goodwill is generated internally over a period of time.

Characteristics of Goodwill

Goodwill has some special characteristics that differentiate it from other assets. In fact, there are some of the important features, as stated below:

Intangible Asset

Goodwill is not a tangible asset since it cannot be seen or even touched. It is an intangible asset since it does not have a physical form but still provides value to the company.

Difficult to Measure

The value of goodwill is highly subjective. It depends on factors like the market position and brand strength of a business, and customer loyalty also plays an important role. Two companies might value the same company’s goodwill differently.

Not Sold Separately

Goodwill is not sold separately. It is always accompanied by the business. If a business is sold, then goodwill is sold along with it.

Long-Term Asset

Goodwill does not have a stipulated life since other assets lose value gradually over time. However, it can be impaired when the business fails to outperform its market or becomes incapacitated in terms of loss of reputation.

Arises only When Acquired

Goodwill can only arise in accounting records when there is an acquisition of a business. Internal goodwill cannot arise in financial statements.

Significance of Goodwill

Goodwill also represents an important dimension of business and accounting, especially in the process of mergers and acquisitions. Why is goodwill important anyway?

Increases the Purchase Price

When a company is sold, the person buying it may be willing to pay more than the net worth of its physical and financial assets. This premium is goodwill. It shows the value of a purchasing company’s intangible assets, such as customer loyalty and brand reputation.

Reflects Business Reputation

Goodwill pertains to the trust and respect that an enterprise has gained in the market. A company that has strong goodwill is termed reliable as well as trustworthy, which will attract and retain new as well as old customers.

Competitive Advantage

The reason why goodwill gives a company a competitive edge is that any business that has a high goodwill is normally easy to expand because it already has an established reputation and loyal customers ready to give it patronage as it gets new products or enters new markets.

Effects on Financial Statements

Goodwill is an asset on the company’s balance sheet of the firm. However, if the value of goodwill decreases, say, a customer base or reputation is lost, the amount can be written off in the books of accounts, which would affect the net profit of the business.

Consolidates Synergies in Acquisitions

Goodwill is that value created due to synergy as a result of the acquisition by two companies combining and creating better operational efficiency, increased market share, and strong brand positioning.

Conclusion

Goodwill is one of the business world’s intangible values that a company has established over time. It indicates the level of reputation of a firm, customer loyalty, and brand power. It will help in forming a clear understanding of the concept of goodwill in accounting. For commerce students, goodwill is important in efforts to get a sense of the value of businesses, especially during mergers and acquisitions. While it is an intangible asset, it weighs much in determining the value of a company.

Goodwill FAQs

Can goodwill be negative?

No, goodwill can never be negative. However, in case the purchase price is lower than the value of net assets, it is called a “bargain purchase.”

Why is goodwill different from other intangible assets?

Goodwill is not identifiable or separable like patents or trademarks. Goodwill arises only in the context of an acquisition and encompasses various factors, including brand name and customer loyalty.

What is the accounting for amortization of goodwill?

Under most accounting standards, goodwill is not amortized but instead undergoes an annual impairment test.

What occurs when goodwill is impaired?

Accounting goodwill involves the impairment of assets that occurs when the market value of an asset drops below historical cost. This causes a decline in cash flows and economic depression.

What is impairment test?

In the impairment test, it is decided whether the carrying value of goodwill exists in the current scenario or if that value exceeds its recoverable amount. Therefore, its value is reduced.