A cash flow statement is a financial statement giving a breakdown of all cash inflows and outflows a company or business has encountered within any given period, mainly over one fiscal quarter or year. It keeps businesses and investors abreast of a company’s cash generation and use, vital information for estimating its liquid position and actual financial performance. This document is important to check whether a company has sufficient cash to meet its obligations, fund its operations, or invest in future growth.

What Is Cash Flow Statement?

A cash flow statement is one of the three key financial statements that businesses use to track and analyze cash transactions. It shows how cash moves in and out of a business, broken down into three main categories: operating activities, investing activities, and financing activities.

Essentially, the statement gives a company’s cash generation and usage overview, thus it makes it easier for the stakeholders to determine whether the company is likely to generate future cash flows and pay dividends. Unlike the income statement which uses an accrual basis for reporting revenues and expenses, the cash flow statement uses only cash transactions, hence making it the most essential document in decision-making processes by creditors, investors, and management.

The statement typically includes:

- Operating Activities: Cash flows generated or spent on core business operations.

- Investing Activities: Cash flows from the purchase and sale of long-term assets such as property, equipment, and investments.

- Financing Activities: Cash flows associated with borrowing, repaying debt, and equity transactions such as issuing or buying back shares.

How to Create a Cash Flow Statement?

Preparing a cash flow statement is not as difficult as it seems because, in reality, it is divided into several steps, a careful analysis of records needs to be done with systematization, dividing items under the correct heading for segregation.

Step 1: Determine the Starting Balance

Preparing the cash flow statement begins with the determination of the cash on hand at the opening balance of the period. This is usually the closing balance of the last period’s cash flow statement or the cash year-end balance as indicated on the balance sheet.

For example, if the opening balance of your company is $50,000 at the beginning of the period, then cash at the beginning of the period is $50,000.

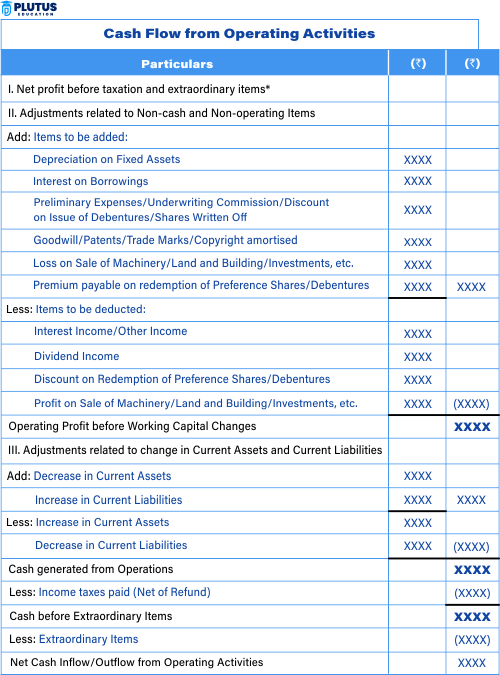

Step 2: Calculate Cash Flow from Operating Activities

Calculate the cash flow from operations. This step determines net cash inflow or outflow produced from a company’s normal business activities, such as selling products or services, paying employees, or acquiring materials.

There are two methods to calculate cash flow from operating activities: the direct method and the indirect method.

Direct Method

This method calculates cash flows directly by adjusting for actual cash receipts and cash payments. The steps include:

- Add cash received from customers.

- Subtract cash paid to suppliers and employees.

- Adjust for other operating receipts and payments. This method provides a more accurate reflection of cash inflows and outflows, but it requires detailed transaction data.

Indirect Method

The indirect method begins with net income and adjusts for non-cash items such as depreciation and changes in working capital. It is widely used because of its simplicity:

- Begin with net income (from the income statement).

- Adjust for non-cash items like depreciation.

- Adjust for changes in working capital (e.g., increase in receivables or payables). The indirect method offers a high-level view of cash flow but may not capture all specific transactions in detail.

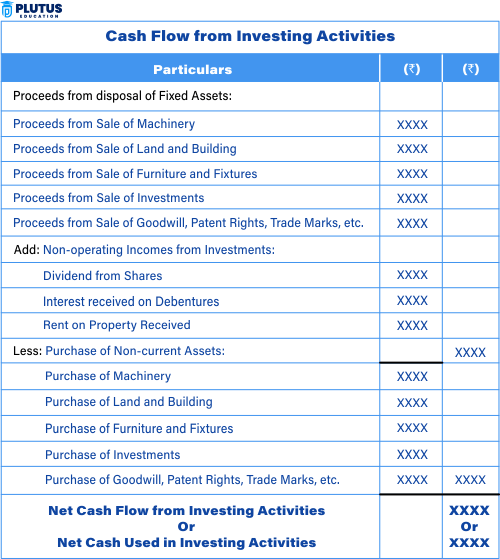

Step 3: Calculate Cash Flow from Investing Activities

The next section of the cash flow statement deals with cash inflows and outflows from investing activities. It includes cash transactions associated with the acquisition or disposal of physical and financial assets. They include but are not limited to:

- Purchases of property, plant, and equipment (capital expenditures).

- Proceeds from the sale of investments or assets.

- Purchases or sales of securities (stocks, bonds, etc.).

For example, if a company buys a new machine for $10,000, that’s a cash outflow under investing activities. If the company sells an old building for $50,000, it’s a cash inflow.

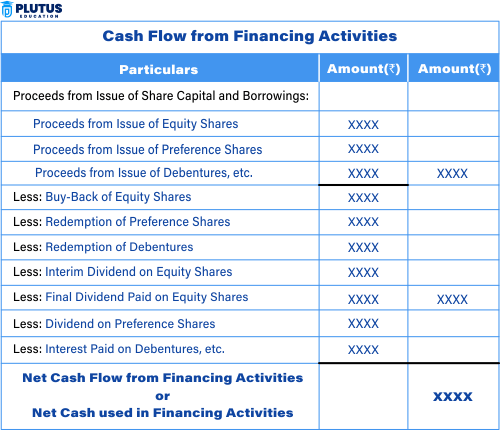

Step 4: Calculate Cash Flow from Financing Activities

The financing activities section of the cash flow statement captures cash flows related to borrowing, repaying debts, or changes in equity. This section includes:

- Proceeds from issuing stocks or bonds.

- Repayments of loans or debts.

- Dividend payments to shareholders.

For instance, if the company raises $100,000 by issuing new equity or borrows $200,000, those transactions would be cash inflows under financing activities. On the other hand, repaying $50,000 in loans would be a cash outflow.

Step 5: Determine the Ending Balance

After getting the cash flow of operating, investing, and financing activities, the following process for the cash flow statement would determine how the balance of cash is present at the end of a given period.

This is calculated by adding the net cash from all activities (operating, investing, and financing) to the starting balance of cash. The formula is:

Ending Cash Balance = Starting Cash Balance + Net Cash Flow from Operating Activities + Net Cash Flow from Investing Activities + Net Cash Flow from Financing Activities

This ending balance will reflect the total cash available at the close of the period and should match the cash balance reported in the balance sheet for that period.

How to Prepare Cash Flow Statement from Balance Sheet?

If you would like to prepare a cash flow statement from the balance sheet, then you would need to adjust changes in the cash and non-cash accounts from one period to the next. You are going to extract specific data from the balance sheet such as:

- Changes in current liabilities and assets: Changes in accounts such as accounts receivable, accounts payable, and inventory.

- Depreciation and amortization: The non-cash charges of these must be added back into net income because they are reductions to profit but not to cash.

- Capital expenditures: These must be recognized as these represent cash outflow for long-term assets.

Once you obtain such data from the balance sheet, follow the same procedures for operating, investing, and financing activities described above. This approach requires you to understand changes in the accounts of the balance sheet and how they affect cash flows.

What to Include in a Statement of Cash Flows?

When preparing a statement of cash flows, some essential components must be included in the document to make it as accurate and complete as possible. The components provide an overall picture of a company’s cash position, and they are:

- Net Income: The statement of cash flows shows net income before preferred dividends. Net income from the income statement can be positive or negative, depending on how much money the business makes and its expenditure. Taxes and interest on debts are examples of costs subtracted from gross income to get the net income.

- Cash Flow from Financing Activities: This section includes cash flows from borrowing and repaying loans, issuing shares, and paying dividends.

- Working Capital: Working capital affects cash flow operating activities, representing the difference between current assets and liabilities other than cash. There’s no change in working capital if a transaction increases current assets and liabilities by the same amount.

- Cash Flow from Investing Activities: This section tracks cash inflows and outflows related to investments in assets, including capital expenditures and sales of long-term investments.

- Cash Flow from Operating Activities: This section reports all cash generated or used in the company’s core business activities, including sales revenue, expenses, and changes in working capital.

- Dividends: Dividends involve owners and affect cash flow, making them part of financing activities. You subtract them from cash when issued. It’s important to record dividend issuance on the statement for accurate results.

How to Enhance Decision-Making with Financial Statements?

A cash flow statement, among other financial statements, such as the balance sheet and income statement, plays a crucial role in business decision-making. It helps stakeholders assess the financial stability and liquidity of a company. Thus making it easier for them to make decisions about investments, financing, and daily operations.

For instance, investors can use the cash flow statement to determine whether the company is generating enough cash to pay its financial obligations, including dividend payments or servicing debt. On the other hand, business owners can use it to understand how efficiently they are managing working capital and whether they need to seek additional financing to fund growth.

The integration of cash flow analysis in decision-making can also enable companies to identify potential financial distress early, allowing for corrective action before the problems worsen.

How to Prepare Cash Flow Statement FAQs

What is the main purpose of a cash flow statement?

The main purpose of a cash flow statement is to provide a detailed analysis of a company’s cash inflows and outflows. It helps investors, creditors, and management assess the company’s liquidity, solvency, and financial health.

What is the direct method of calculating cash flow from operating activities?

The direct method calculates cash flow from operating activities by directly tracking actual cash receipts from customers and payments to suppliers and employees. This method offers more detailed insights into cash operations but is more data-intensive.

How does a company calculate cash flow from investing activities?

Cash flow from investing activities is calculated by adding the cash received from the sale of assets and subtracting cash spent on purchasing new assets, such as property, plant, or equipment. It reflects how the company invests in long-term assets.

Can I prepare a cash flow statement without an income statement?

Yes, you can prepare a cash flow statement without an income statement, but it will be more difficult. The income statement provides essential details on net income, which is used in the indirect method of calculating cash flow from operating activities.

What are the main sections of a statement of cash flows?

The three main sections of a statement of cash flows are cash flows from operating activities, investing activities, and financing activities. Each section details the respective inflows and outflows of cash during the reporting period.