The term independent auditors report is described as a formal document prepared by the independent auditor after being cognizant of the company’s financial statement. The report states whether the financial statements present a true and fair view and comply with accounting standards.

Auditors will examine, assess, and analyze the company’s records to form an opinion about the material being put to audit before reporting on it. These findings will then be included in the independent auditor’s report. This report is further utilized to decide upon some prime financial business and hence lends credence to the stated information with a view to overall transparency and accountability.

It offers assurance to the investors, creditors, and the other stakeholders that the company is financially sound. An independent auditor’s report expresses an auditor’s opinion concerning the accuracy and fairness of a company’s financial statements. It is an integral part of the company’s financial reporting.

What is Audit Report?

An audit report is a written document presented by the auditors upon examining the company’s financial statements. The report states the auditor’s opinion of the true and fair view of the financial statements.

The audit report is prepared according to GAAP guidelines and applicable laws. The purpose was to ensure that investors could rely upon the company for information and disclosures about regulatory compliance in their investments. On the contrary, if financial statements carry a historical statement, then legal and financial occur.

Purpose of Audit Report

Every public company must obtain an audit report with external finance. The report is obligatory to furnish useful economic information and aid decision-making. The major purposes of an audit report are:

- To attest to the fair presentation of the financial statements.

- To express an opinion on whether the applicable laws and accounting standards prepared the financial statements.

- To offer assurance to the users of the financial statements.

- To ascertain whether any material misstatement exists.

- To enhance the credibility of the company.

Types of Audit Report

Each type of audit report is the primary basis for any economic decision by the business. Companies should pursue unqualified audit reports to sustain their credibility. Depending on their findings, auditors issue different reports. These reports rely on whether the financial statements are in bona fide health and compliant with laws and regulations.

Unqualified audit report

The unqualified audit report certifies that the financial statements present a true and fair view following accounting standards; it is popularly called a clean audit report. The unqualified audit report says there are no issues with financial reporting.

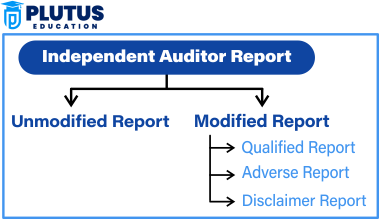

Qualified Audit Report

The qualified audit report is issued for minor issues with the financial statements. While these problems do not affect the overall fair view, they must be corrected. The auditor sets out the reasons for the qualification in the report.

Adverse Audit Report

An adverse audit opinion is issued when the financial statements contain material misstatements and do not present a fair view. This is a distressing opinion and an implication of misrepresentation or fraud. Companies with an adverse report must fix the situation urgently.

Disclaimer of Opinion

The disclaimer of opinion means that the auditor had not been able to obtain sufficient appropriate audit evidence to provide a basis for an audit opinion, such as the inability to verify the information provided or the restriction imposed on the scope of the audit. This report states that financial statements might not be reliable.

Independent Auditors Report Meaning

An Independent auditor report is a report that is issued by an external auditor who does not have any connection with the company. This will ensure that the audit is independent and has no conflicts of interest. The independent auditors report gives an objective opinion as to whether the company’s financial statements are fair in their presentation and comply with rules and regulations. It is critically important for investors, regulators, and other stakeholders.

Importance of an Independent Auditors Report

An independent auditors report is essential for maintaining investors’ confidence and in corporate governance. Companies can ensure accurate financial statements before getting a favourable audit opinion. Depending upon their findings, the auditors provide various forms of audit reports.

- To foster transparency in financial reporting.

- Enables informed decisions by investors.

- Builds trust and credibility in the company.

- Compliance with laws and regulations.

| Importance | Explanation |

| Ensures Financial Accuracy | The report verifies that financial statements are free from material misstatements and present a true and fair view of the company’s financial health. |

| Improves Creditworthiness | Banks and lenders use audited reports to evaluate a company’s financial stability before approving loans or credit lines. |

| Identifies Weaknesses in Internal Controls | Auditors often provide recommendations for improving internal controls, reducing the risk of financial mismanagement. |

Content of Independent Auditors Report

An independent auditors report is in a certain format as it contains sections addressing the audit processes and the auditor’s opinions.

1. Title and Addressee: It will first bear a title, commonly “Independent Auditors Report,” and is directed to the stockholders or the board of directors.

2. Introduction: This introduction declares the reason for writing the report and the financial statements audited. The audited period is also specified in terms of the financial year.

3. Management’s Responsibility: This section shows that management is supposed to create and ensure the accurate preparation of financial statements by the auditor. The auditor does not prepare financial statements but examines them.

5. Auditor’s Opinion: The auditor’s opinion is the most significant part of the independent auditor’s report in which he states whether the financial statements are true and fair.

6. Basis for Opinion: This section provides the grounds underpinning the auditor’s opinion. If there are any limitations, they are mentioned here.

7. Signature and Date: The report is sealed with the auditor’s signature and the date, together with the details of the audit firm, to ensure that the report is authentic.

Opinion in Independence Audit Report

The opinion in the independent audit reports is the conclusion drawn by the auditor, which helps the stakeholders to understand whether the financial statements are reliable.

Types of Opinions in an Independent Auditors Report

- Unqualified Opinion – Financial statements are accurate and comply with regulations.

- Qualified Opinion – There are minor issues, but financial statements are mostly accurate.

- Adverse Opinion – The financial statements are incorrect or misleading.

- Disclaimer of Opinion – The auditor could not complete the audit due to insufficient information.

Importance of Auditor’s Opinion

It affects the reputation and credibility of the company. Most importantly, All companies should strive for an unqualified opinion to maintain trust and avoid financial risks. This is based on the investors’ decision. Used by the regulatory authority for compliance. Considered by the lenders before lending money. It plays an important role in financial reporting and is accurate, transparent, and compliant with regulations. Investors, creditors, and regulators may act on their business-related decisions through this.

It is a well-founded audit report concerning which any company should have unqualified as a sign of credibility and trustworthiness. Besides, preparing a good financial statement helps enterprises grow and avoid legal tangles.

Thus, understanding an independent auditors’ report is essential for financial success. Companies must ensure that their records are accurate and comply with auditing standards to obtain a positive result in the audit opinion.

Independent Auditors Report FAQs

1. What is an independent auditors report format under Companies Act 2013?

The format of an independent auditors’ report under the Companies Act 2013 also contains sections like title, addressee, introduction, management’s responsibility, auditor’s responsibility, opinion, basis for opinion, and signature. Such requirements must be met according to the auditing standards set by law.

2. To whom is the company auditor report given?

The prepared company auditor report will be given to shareholders, the board of directors, or regulatory authorities. Thus ensuring transparency and helping stakeholders make financial decisions.

3. What happens if a company gets an adverse audit report?

If it is an adverse audit report, it can have serious particular financial misstatements. The company must take Corrective measures concerning the accounting policies and regulatory concerns to avert possible legal consequences.

4. Why is it important that an independent auditor report will be valuable to investors?

An independent auditor’s report helps investors conclude the company’s financial health. Therefore, it will assist investors in deciding whether the company is financially stable and relies on the investment itself.

5. Can a company change its audit opinion?

The company cannot directly change its audit opinion. Rather, it can rectify errors and improve financial reporting, and it can also redo an audit to get a better opinion.