An interim audit involves preliminary audit work conducted before the financial year-end of a client, usually covering six or nine months. Generally, interim audit work involves tests of controls and specific substantive procedures.

Every business requires keeping accurate financial records for smooth operations within the organization. Auditing proves to be vital in examining and verifying those financial records. There is one such type of important audit, which is called interim audit. Then, it is given to the company’s management for immediate corrections, if needed, based on timely indicators of financial health.

Interim Audit Meaning

Interim audit allows businesses to track their financial health to make sure all transactions are correctly recorded. Unlike the final audit, which is conducted at the end of the financial year, an interim audit is generally performed after the house periods, such as quarterly or semi-annually.

An interim audit aims to detect early errors, fraud, and misstatements, improve internal controls, and ensure regulation compliance. With increasing demands for transparency in financial markets, many companies conduct interim audits to build their credibility.

Advantages and Disadvantages of Interim Audit

A business must scale the merits of undertaking an interim audit, with some demerits being adverse to this exercise. While it does aid in efficiently managing financial records, some challenges are associated with it.

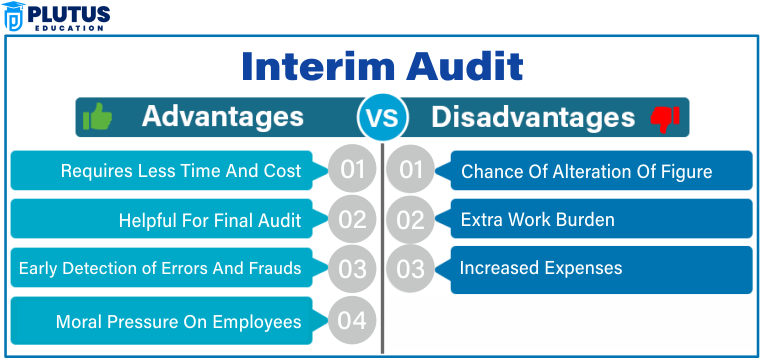

Advantages of Interim Audit

To achieve all this and more, interim audits benefit businesses by creating a more effective financial discipline. Interim audits help companies to minimize their financial discrepancies and ensure the precision of financial statements. These have become a part of the very important expectations from a company aspiring to have a transparent record and develop stakeholder trust.

Early Detection of Errors and Frauds

Interim audits assist firms in discovering and remedying mistakes quickly. If there are misstatements, fraud, or discrepancies in finances, they will find them before final auditing. In this way, money mismanagement does not happen.

Better Financial Control

Business running interim audits can also refine their internal control systems. Auditors investigate the accounting records, making identifying loopholes or weak financial practices easy. Strong controls reduce business risk and enhance transparency.

Reduced Year-End Collections

Interim audits assess the business’s financial records over intervals so that at the final audit, one does not face much ado about end-year collections. It saves time while ensuring a smooth auditing process.

Improve Stakeholder Confidence

Regular audits engender trust among stakeholders like investors, creditors, and regulatory bodies. Companies are then perceived as fiscally more responsible and reliable for conducting interim audits.

Disadvantages of Interim Audit

An interim audit does not warrant increased efficiency at times and further added workload. This process needs additional financial resources and risks repeating checks if not coordinated with the final audit.

Additional Costs

Managing several audits during the year takes in an extra financial planning cost. Even hiring auditors and maintaining audit procedures incur additional fees for the businesses. Lastly, the audit process has to be carefully managed to avoid disruptions to routine activities.

Risk of Duplicative Work

The transaction will likely undergo another set of examinations by an auditor in an interim audit since it will be before the last audit. Hence, audit processing will be inefficient, and the costs incurred during the audit will rise.

Interruptions of Business Operations

An interim audit would need the presence of financial staff, but this might disrupt daily business operations. Employees can schedule time for auditors but not their routine responsibilities. These balances of advantages and disadvantages highlight why businesses must carefully implement interim audits to maximize benefits while minimizing drawbacks. Good planning and sound structuring of auditing execution improve the efficiency and benefit of the companies.

Possible Manipulation of Accounts

Some firms are likely to manipulate their account books after interim audits since final audits are carried out long after the interim audits. Companies will use the time-lapse to change their transactions and misinform auditors.

Objectives of Interim Audits

Interim audits vary and serve many purposes in effective financial management. Businesses carry it out for many reasons, all for the same purpose- ensuring financial correctness and openness.

- Check Financial Records for Accuracy: The primary purpose of the interim audit is to ensure all financial transactions are recorded appropriately. The audit examination finds inconsistencies and errors in maintaining exact accounting records.

- Identification of Fraud and Errors: Fraud detection is an essential objective of the interim audit. The auditor can pick up unreasonable transactions and fraud cases that can save companies from fraudulent financial loss.

- Assessment of Internal Controls: An interim audit also assesses a company’s internal controls. Poor controls create risk; auditors typically advise on any improvement needed.

- Ease the Final Audit Process: An interim audit reduces the work for the final audit process. The financial statements then are up-to-date and facilitate the final audit process.

Purpose of conduct of Interim Audits.

There are various reasons why companies conduct interim audits, including financial accuracy, compliance, legal legality, and operational efficiency.

- Regulatory Compliance: Many industries must conduct periodic audits to be legal and financially compliant in these areas.

- Investor Confidence: Interim audits bring to the business the scope of transparency and, hence, more trust from the investors.

- Operational Efficiency: It avoids constant review of the business finances being conducted.

How Are Interim Audits Conducted?

Auditors will decide which financial areas to focus on. Auditors review accounting records and financial statements. The effectiveness of controls is assessed. The audit findings are presented to management for measures to take.

Difference Between Continuous Audit and Interim Audit

These audits allow companies to assess their financial state before the final audit and simplify matters during the year-end. Through interim audits, organizations can increase the correctness to their financial statements and better internal control systems. Continuous audit vs final audit are as follows.

| Aspect | Continuous Audit | Interim Audit |

| Frequency | Conducted regularly throughout the year | Conducted at specific intervals |

| Objective | Ensures real-time financial accuracy | Check financial status before the final audit |

| Scope | Extensive, covering daily transactions | Limited to periodic reviews |

| Timeframe | Continuous process | Fixed intervals |

Difference Between Interim Audit and Final Audit

Interim audits are largely beneficial to businesses for having their financial records well-kept all year. It reduces the financial burden accrued at the end of the financial year and assists in ensuring financial correctness.

| Aspect | Interim Audit | Final Audit |

| Timing | Conducted before the financial year ends | Conducted at the financial year’s end |

| Objective | Identifies financial errors early | Provides final verification of financial statements |

| Scope | Limited to specific areas | Covers all financial transactions |

| Legal Requirement | Not mandatory | Mandatory for most businesses |

Interim Audit FAQs

What is interim audit?

A financial review done in intervals before the final audit is called as an interim audit. It detects errors early, ensures compliance with laws, and improves internal controls.

What is the distinction between interim audit and final audit?

An interim audit would be done from time to time. However, the final audit will be conducted at the end of the year for financial purposes. In the last audit, all financial transactions are legally obligatory.

What are interim audits benefits and cons?

The pros are distinct early detection of errors, good control, and a less burdensome final audit. The cons could include greater than average costs, duplication of effort, and disturbances to business.

What is the difference between an interim audit and continuous audit?

A continuous audit is held regularly, which involves daily transactions, while an interim audit evaluates the financials at several intervals.

Why Companies would do Interim Audits?

Companies undertake this type of audit to ensure financial accuracy, fraud detection, compliance, and improved operational efficiency.