The limitations of internal rate of return play a vital role in the decisions about investment and project assessment. Investments depend on IRR to deliver assessment results on the reliability and accuracy of projects for investors. Contrary to its favoured term in capital budgeting, IRR has many faults that may mislead investors. The method of IRR requires multiple responses, unrealistic reinvestment rates, and perfect treatment of unconventional cash flows. Each of these situations may lead to inconveniences when comparing different investment projects.

The internal rate of return denotes internal investment profitability and is the only discount rate that sets NPV equal to null regarding cash flow. The IRR method can also be referred to as a criterion to justify whether a particular investment project should be accepted or rejected. Despite its merits, IRR has a lot of shortcomings, which, if considered, could lead to erroneous investment decisions.

Firms use the IRR to compare investment projects with varying cash flow structures. In this regard, it is relevant in capital budgeting decisions but does not factor in any external influences, such as market conditions and cost of finance. The IRR model also presupposes cash flows to be reinvested at IRR, which is hardly realistic. These are some of the impediments that limit the methods; thus, they become unreliable in many situations.

What is Internal Rate of Return?

The IRR refers to the discount amount that makes a project’s net present value equal to zero. The IRR expresses the expected annual return for an investment. This is a significant measure in capital budgeting, often used for comparing the profitability of alternative projects.

The IRR helps firms evaluate whether an investment would result in positive returns. The higher the IRR, the more valuable the project; the lower the IRR, the less attractive the investment. IRR is then determined against a required return to decide whether to accept or reject a project. The project may be accepted if the IRR exceeds the capital costs.

However, IRR has some disadvantages that make it inadequate. It does not factor in size, length of execution, or susceptibility to external danger. It also assumes that reinvestment occurs at IRR, which is often unacceptable. All these factors continue to create problems for investment analysis with IRR.

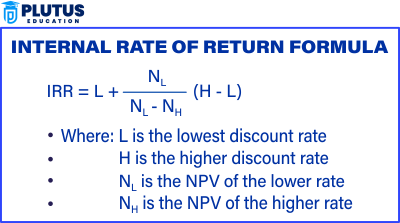

Internal Rate of Return Formula

The internal rate of return formula defines the discount rate that sets cash flows’ net present value (NPV) to zero. The IRR formula is:

With the above formula, cash flow from an investment is thus internally compared. Since analytically solving for IRR is impossible, solving the IRR equation requires either trial and error or a software tool.

Assumptions of Internal Rate of Return Formula

The IRR formula has several assumptions underlying it. These assumptions can generate this metric into an untrustworthy investment analysis standard. These assumptions further reveal the inadequacies of IRR and show why businesses should look at other evaluative measures, such as net present value (NPV), in evaluating their future investments.

- Reinvestment at IRR: The IRR method assumes that future cash flows are reinvested at the calculated IRR. This assumption is often unrealistic since businesses reinvest at the cost of capital.

- Stable Discount Rate: While it is true that IRR assumes the discount rate remains stable over the entire lifetime of a project, in reality, interest rates fluctuate and significantly affect investment returns.

- Positive Cash Flows: The formula assumes that cash flows will always be positive after the initial investment; however, many projects experience negative cash flows in some years.

- Singularity of IRR Value: The method assumes only one IRR value exists. Nonetheless, projects experiencing unconventional cash flows may possess more than one IRR, rendering such projects very hard to evaluate.

- Equal Time Frame of Comparison for Projects: IRR does not recognize the time difference when assessing two real or hypothetical projects. As a result, the comparison appears to be misleading.

Limitations of Internal Rate of Return

The IRR can be accepted as the basis for one more investment decision; nevertheless, it has certain limitations that reduce its reliability. Out of the eight limitations listed below, those are the most notable.

Multiple IRRs

A project with unconventional cash flows may have several IRRs, thus creating difficulties in understanding and selecting the effective rate of return, further confusing the investment decision. A project with alternating cash inflows and outflows has other corresponding discount rates that will satisfy the equation, i.e., NPV = 0, thus creating ambiguities.

Assumes Reinvestment at IRR

The IRR method assumes all future cash flows are reinvested at the IRR. In practice, firms reinvest at their cost of capital, which is invariably less than the IRR. Such false assumptions inflate the estimated returns for decision-making purposes.

Ignores Project Size

Internal Rate of Return does not consider the absolute project size. A smaller investment with a higher IRR may not generate as much profit as a bigger one with a lower IRR. Hence, some other kind of project evaluation parameter/financial metrics must be used to compare among projects effectively.

Difficult for Mutually Exclusive Projects

IRR can produce misleading results when compared to mutually exclusive projects. Thus, it would favour quick returns on a brief duration over long-term sustainable cash flow investments. External risks such as market conditions, inflation, and changes in interest rates have no bearing on the IRR, which tends to be an unreliable indicator on its own.

Fails in Unconventional Cash Flow Scenarios

IRR works poorly in hazardous cash flow variations; where gains are realised in one period followed by losses in another, the IRR calculations would yield multiple or nil values, thus placing an obstacle in assessing the project.

Does Not Consider Project Duration

IRR does not discern between a short-term project and one of long duration. A project with a high IRR but a short duration may not be preferred over a long-term project with stable returns; hence, the misuse of this method may lead to incorrect investment decisions.

Requires Complex Calculations

The computation of IRR utilises iterative techniques and is unruly for algebraic reckoning. Firms usually require supportive software or financial tools for accurate IRR computation, making it less useful in rapid decision-making.

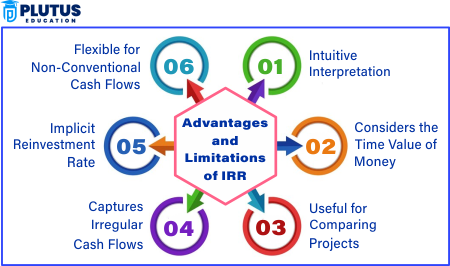

Advantages of Internal Rate of Return

Despite the disadvantages, there are several advantages to IRR. It is most commonly used in capital budgeting because it is a relatively easy way to evaluate the return on investment. The five main advantages are as follows:

- Easy to interpret: IRR expresses profitability in percentage terms, an easily understood scale for investors to make relative comparisons across projects.

- Time value of Money: IRR accounts for the time value of money and applies proper discounting for future cash flows.

- Useful for Capital Budgeting: IRR aids capital budgeting decisions by contemplating a project’s immediate future viability.

- Independent of Project Size: Other measures require project size information, while IRR can compare projects of any size without such knowledge.

- Considers the cash flow timing: The IRR considers timing regarding cash flows, which is the basis of project evaluation.

Net Present Value vs Internal Rate of Return: Key Differences

Both net present value (NPV) and internal rate of return (IRR) are among the most popular capital budgeting methods. Although these methods evaluate possibilities in project profitability, their surrounding techniques and interpretations differ. NPV measures value in absolute dollars added by investment instead of an IRR, which expresses return as a percentage. Therefore, the choice between NPV and IRR depends on the project size, cash flow patterns, and the cost of capital.

| Feature | Net Present Value (NPV) | Internal Rate of Return (IRR) |

| Definition | Calculates the difference between the present value of cash inflows and outflows | Determines the discount rate where NPV equals zero |

| Measurement | Expressed in absolute monetary terms | Expressed as a percentage |

| Decision Rule | Accept if NPV > 0 | Accept if IRR > required rate of return |

| Consideration of Cost of Capital | Explicitly considers the cost of capital | Assumes reinvestment at IRR |

| Handling of Multiple Projects | Works well for mutually exclusive projects | It may give misleading results for mutually exclusive projects |

| Complexity | Requires setting an appropriate discount rate | May have multiple IRRs in complex cash flows |

| Suitability | Better for large-scale investments with varying cash flows | Helpful in comparing projects of similar size and risk. |

Limitations of Internal Rate of Return FAQs

What is the internal rate of return in capital budgeting?

Internal rates are helpful in capital budgeting for determining the profitability of an investment. It gives the discounted rate at which future cash flows equals zero because the present value of cost equals revenue.

How is the internal rate of return formula used in method?

The internal rate of return formula is applied to determine a suitable discount rate for which the project’s net present value will be equivalent to zero. Trial-and-error calculations or software implementation would be required as they are not directly computable.

What are the main limitations of internal rates of return?

It has several inherent limitations, including multiple IRRs generated due to an assumption of reinvestment at the IRR, ignoring project size, and failing in some unique cash flow situations.

Why does IRR assume it should reinvest at its IRR?

Calculating IRR is made so easy, but it never turns true since institutions would reinvest at their respective cost of capital instead of at the IRR.

What method is superior NPV vs IRR for evaluating investments?

NPV has proven to be a better method than IRR for overall investments, as it gives all investments an accurate evaluation and does not go through multiple IRR problems.