Payable management systematically manages a firm’s short-term obligations to vendors and suppliers. It ensures prompt payments, maximises cash flow, and fosters strong vendor relationships. Companies employ payable management techniques to manage cash outflows and prevent liquidity problems. Proper payables management lowers costs, improves financial well-being, and optimises operational performance. Effective payable management also enables companies to negotiate favourable credit terms and benefit from early payment discounts.

What is Payable Management?

Payable management is the management of a firm’s outstanding payments to vendors, suppliers, and creditors. It includes monitoring invoices, making timely payments, and maximising payment terms to enhance cash flow and business relationships.

Invoice tracking is beneficial for businesses as it allows them to record all outstanding payments for accuracy. A deposit scheduling system ensures payments are timely and avoids late fees. Companies can negotiate favourable terms and discounts with strong supplier relationships. Cost optimisation minimises costs by utilising early payment discounts. Proper cash flow management ensures enough inflows to meet outflows and maintains liquidity and financial stability.

Payable Management Objectives

The payable management objectives focus on optimising cash flow, maintaining supplier trust, and improving financial stability.

- Optimizes Cash Flow: Provides enough liquidity for day-to-day operations. Divides inflows and outflows to prevent cash shortages. It allows businesses to project future outcomes accurately. Avoid cash flow interruptions that could affect business operations It has long-term financial stability and growth.

- Avoid Late Payment Penalties: It saves interest and penalty charges and improves financial discipline and compliance. Minimises the risk of hurting supplier relationships. Enhances creditworthiness and business image/ goodwill. Maintains organised, complete, and accurate financial records.

- Enhance Supplier Relationships: Instills a sense of trust in the vendors by making timely payments. It aids in negotiating better credit terms and discounts. Asks suppliers to provide flexible payment terms. Mitigates risk of supply chain interruptions. Advocates long-term partnerships targetting your business.

- Cost Efficiency: Saves costs by avoiding early payment discounts. Enhances financial performance by optimising working capital. Removes needless late fees and penalties. It also allows businesses to allocate money to priority areas. Makes wise financial decisions while increasing revenues.

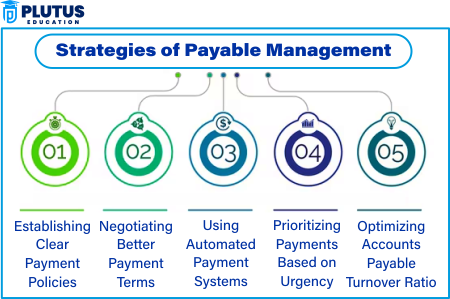

Strategies of Payable Management

Payable management is an integral part of any business that ensures the smooth flow of capital in and out of an organisation. Companies benefit from timely payments, cost reduction, and improved supplier relationships by adopting the right strategies. The following summarises important techniques businesses use to manage payables efficiently.

Establishing Clear Payment Policies

By establishing punctual payment schedules, vendor payments can correlate with the business’s cash influx. Companies must establish a structured payment process to ensure uniformity and avoid delays. Having straightforward policies omits deadline lapses, lowers penalties, and improves financial planning. Standardising payment terms establishes trust with suppliers and enhances relationships.

Negotiating Better Payment Terms

Negotiating to extend your payment deadlines prevents businesses from being over-stressed in their cash flow and still meeting their obligations. Suppliers can provide bulk buying discounts or payment options to a long-term business partner. This will enable businesses to strike better terms, minimise excessive financial burden, and manage working capital more effectively in the long run to ensure healthy operations.

Using Automated Payment Systems

Automating the payment processes minimises human errors in invoice processing and guarantees precise transactions. Businesses can automate in advance payments and avoid missed deadlines and penalties. Digital payment solutions also enable real-time tracking, improving financial control. Automation increases efficiency, lowers administrative costs, and handles seamless cash flow.

Prioritising Payments Based on Urgency

Payments must go to high-interest obligations first instead of free play. Liabilities are not only short-term but also long-term. Paying off the most pressing debts first helps to avoid extra costs to the debt, like penalties or late fees. A practical payment strategy allows the business to maintain a good credit score and improve financial flexibility.

Optimising Accounts Payable Turnover Ratio

To optimise their status in the turnover ratio accounts, businesses should analyse their payables in correlation with their total purchases. Aligning payments with financial goals avoids liquidity problems. A higher turnover ratio shows that a company pays off its debts quickly, leading to better financial credibility. Through effective payables management, we can sustain long-term economic development and stability.

Importance of Payable Management

Payable management is an integral part of a company’s financial health. Improper payables management could lead to liquidity crises, poor supplier relationships, and higher operational costs.

- Maintains Liquidity: Helps give businesses cash to cover expenses. Lowers reliance on outside funding. Includes better cash flow planning and forecasting. Avoiding cash deficiencies that might impede day-to-day activities. Instead focuses upon ensuring financial sustainability and long-term business viability.

- Prevents Financial Risks: No more late fees and interest due to overdue payments. Monitors supplier compliance with agreements. Keeps businesses financially disciplined and organised. Minimise supply chain disruptions that delayed payments can cause.

- Improves Supplier Trust and Collaboration: Initiates long-term business partnerships. Gives enhanced bargaining power for subsequent dealings. Guarantees timely payments that generate credibility amongst suppliers. Which could lead to bulk discounts and favourable payment terms. Consolidates the supply chain for easy business operation.

- Boosts Business Credibility: A positive payment history can raise credit scores and ratings. It helps businesses to obtain better financing options. It is more easily accessible through bank loans and credit facilities. Make it cheaper with lower interest rates because of strong financial credibility.

- Optimizes Business Operations: Lowers administrative burden with professional payable tracking. Enables seamless production and inventory management. Actions make it easier to plan finances and allocate resources. Reducing payment delays helps enhance overall business efficiency. It improves internal controls and financial transparency.

Relevance to ACCA Syllabus

Payable management forms a significant component of Financial Management (FM) and Advanced Financial Management (AFM) in the ACCA curriculum. Schools for Finance reflect an understanding of what funds enterprises use to manage short-term liabilities, optimise cash flow and find suppliers.

Payable Management ACCA Questions

Q1: What is the primary objective of payable management in financial management?

A) To delay payments as long as possible

B) To ensure timely payments while optimising cash flow

C) To increase short-term liabilities for better financial leverage

D) To reduce accounts payable to zero

Ans: B) To ensure timely payments while optimising cash flow

Q2: Which of the following is an advantage of an optimised payable management strategy?

A) Increased interest expenses due to delayed payments

B) Poor supplier relationships and reduced credit terms

C) Improved working capital efficiency and cost savings

D) Higher risk of stock shortages due to late payments

Ans: C) Improved working capital efficiency and cost savings

Q3: In financial management, what is the impact of an increase in accounts payable on cash flow?

A) Cash flow increases because payments are deferred

B) Cash flow decreases because more cash is used for payments

C) No impact as payables do not affect cash flow

D) Cash flow remains constant as payables and receivables balance out

Ans: A) Cash flow increases because payments are deferred

Q4: Which financial ratio is most commonly used to assess a company’s ability to pay its short-term obligations?

A) Return on Assets (ROA)

B) Current Ratio

C) Price-to-Earnings Ratio

D) Debt-to-Equity Ratio

Ans: B) Current Ratio

Relevance to US CMA Syllabus

In the CMA syllabus, payable management is dealt with under working capital management and financial decision-making, including cost control, liquidity management, and ensuring that cash flows to avoid financial distress. Accounts payable knowledge helps CMA candidates add value to an organisation by improving business efficiency and reducing costs.

Payable Management US CMA Questions

Q1: Which of the following best describes the relationship between accounts payable and working capital?

A) Increasing payables decreases working capital

B) Decreasing payables improves working capital

C) Increasing payables improves cash flow and working capital efficiency

D) Working capital does not include accounts payable

Ans: C) Increasing payables improves cash flow and working capital efficiency

Q2: A company negotiates longer payment terms with its suppliers. What is the most likely impact on cash flow?

A) No impact on cash flow

B) Improved cash flow due to delayed payments

C) Reduced cash flow due to higher interest expenses

D) Increased cash flow volatility

Ans: B) Improved cash flow due to delayed payments

Q3: Which formula is used to calculate the payable turnover ratio?

A) Total Payables / Total Purchases

B) Total Purchases / Average Accounts Payable

C) Cash Flow from Operations / Accounts Payable

D) Average Inventory / Accounts Payable

Ans: B) Total Purchases / Average Accounts Payable

Q4: Which financial metric will likely improve if a company takes full advantage of early payment discounts?

A) Profit Margin

B) Earnings Per Share (EPS)

C) Operating Cash Flow

D) Fixed Asset Turnover

Ans: C) Operating Cash Flow

Relevance to US CPA Syllabus

Payable management is covered as part of accounts payable under the Certified Public Accountant (CPA) syllabus under Financial Accounting and Reporting (FAR) and Business Environment and Concepts (BEC). It is the responsibility of accounts payable to classify liabilities appropriately, manage cash flows effectively, and ensure compliance with accounting standards to accounts payable and working capital optimisation.

Payable Management US CPA Questions

Q1: Under US GAAP, accounts payable should be classified as what type of liability?

A) Long-term liability

B) Current liability

C) Contingent liability

D) Deferred liability

Ans: B) Current liability

Q2: A company has a payable turnover ratio of 5. What does this indicate?

A) The company pays its suppliers on average 5 times a year

B) The company delays its payments for 5 years

C) The company has poor credit terms with suppliers

D) The company is inefficient in managing its payables

Ans: A) The company pays its suppliers on average 5 times a year

Q3: In accrual accounting, when should accounts payable be recognized?

A) When the supplier is paid

B) When the expense is incurred

C) When cash is received from customers

D) When the company has excess cash available

Ans: B) When the expense is incurred

Q4: Which of the following best represents an example of an accrued expense in payable management?

A) A loan payment made to a bank

B) Unpaid supplier invoices for goods received

C) Early payment discounts received from suppliers

D) A customer refund due to product returns

Ans: B) Unpaid supplier invoices for goods received

Relevance to CFA Syllabus

In the CFA (Chartered Financial Analyst) curriculum, payable management forms part of Corporate Finance and Financial Statement Analysis. CFA students learn the impact of payables on liquidity ratios, cash flow management and financial risk. Such a ratio is pivotal in assessing the short-term financial strength of an organisation and making decisions around suppliers’ financing.

Payable Management CFA Questions

Q1: How does an increase in accounts payable affect the operating cash flow in the indirect method of cash flow statement?

A) Operating cash flow increases

B) Operating cash flow decreases

C) No impact on cash flow

D) Cash flow from financing increases

Ans: A) Operating cash flow increases

Q2: What is the effect of an increase in the payable turnover ratio?

A) The company is paying suppliers faster

B) The company is delaying payments to suppliers

C) The company is not managing working capital efficiently

D) The company has too much cash tied up in inventory

Ans: A) The company is paying suppliers faster

Q3: Which financial metric is most impacted by changes in accounts payable?

A) Return on Equity (ROE)

B) Net Profit Margin

C) Free Cash Flow

D) Asset Turnover Ratio

Ans: C) Free Cash Flow

Q4: Which of the following characteristics is a company with a payable turnover ratio of 12 likely to have?

A) Pays suppliers every 30 days

B) Pays suppliers every 60 days

C) Pays suppliers every month

D) Pays suppliers once a year

Ans: C) Pays suppliers every month