The payback period formula is applied to calculate the period in which an investment will cover its initial cost through generated cash flow. It is an easy and effective method for assessing investment choices. Companies apply the payback period method formula to check the risk and viability of projects. The less the payback period, the quicker the recovery of the investment. Yet this approach does not consider the time value of money, which is why the formula for discounted payback period is also employed to be more precise.

What is Payback Period?

The payback period is when it takes to pay back the money invested in an investment. It indicates how long an asset, such as a machine or plant, will take to make enough profit to repay the original cost. Companies use this to know when they will break even on their investment.

Divide the initial investment by the yearly cash inflow to get the yearly payback period. If you want to know the monthly payback period, divide the initial investment by the monthly cash inflow. The shorter payback period indicates a quicker return on investment, which assists firms in making good financial decisions.

How to Calculate Payback Period?

The payback period tells how long it takes for an investment to recover its cost. It is calculated by dividing the total investment by the money earned each year.

Step 1: Find the Initial Investment

This is the total money spent on the project. Example: A company invests ₹6,00,000 in a new machine.

Step 2: Find the Annual Cash Inflows

This is the amount of money the project earns every year. Example: The machine generates ₹1,50,000 per year in savings.

Step 3: Apply the Payback Period Formula

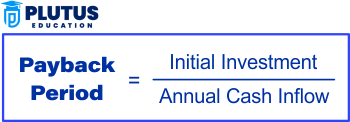

Payback Period=Initial Investment/Annual Cash Inflows

Using the example:

6,00,000/1,50,000=4 years

This means the company will recover its ₹6,00,000 investment in 4 years.

Payback Period with Unequal Cash Flows

Sometimes, a project does not earn the same amount every year. In such cases, we add the yearly earnings until the total investment is recovered.

A company invests ₹8,00,000 in a project with the following cash inflows:

| Year | Cash Earned (₹) | Total Earned So Far (₹) |

| 1 | 2,00,000 | 2,00,000 |

| 2 | 2,50,000 | 4,50,000 |

| 3 | 3,00,000 | 7,50,000 |

| 4 | 2,00,000 | 9,50,000 |

After 3 years, the company has earned ₹7,50,000.

The remaining amount to recover is 8,00,000−7,50,000=50,000. In Year 4th, the company earned ₹2,00,000, more than needed.

To find the fractional year, we divide the remaining amount by Year 4 earnings: 50,0002,00,000=0.25

Now, we add this to 3 years:

3+0.25=3.25 years

So, the investment will be recovered in 3.25 years.

Payback Period Formula

The basic payback period method formula is: Payback Period=Initial Investment/Annual Cash Inflows.

But when cash flows are not regular, we utilize a cumulative cash flow method:

- Cumulative Cash Flow Calculation: Sum annual cash flows until the sum reaches or surpasses the initial outlay.

- Fractional Year Adjustment: If the investment is returned between years, use:

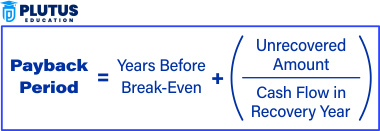

Payback Period=Previous Year Of Recovery+Unrecouped Investment/Net Cash Flow in coming Year.

What is Good Payback Period?

A good payback period is when an investment will yield sufficient cash flows to recover the initial investment cost. In most instances, companies want a 3 to 5 years payback period. This enables them to quantify how fast they can recover their funds and minimize financial risk.

A lower payback period is preferable as it reduces risk and enhances investment effectiveness. It indicates that companies can realize profits sooner. A reasonable payback period also generates a faster return on investment; thus, it is an essential determinant of financial decisions.

What is Bad Payback Period?

A bad payback period means an investment doesn’t recover its cost quickly enough, usually anything around 7 to 10 years, and so on. This renders the investment quite risky and unappealing. Two out of every 3 firms can suffice for a payback duration of under 3 years because shorter payback periods lower the uncertainty of finances and can improve cash flows.

A long payback period can indicate poor capital allocation and high risk when investing. It may be a bad investment if it takes hours to break even. This also shows regressive returns and resource misuse, leading to lower profitability over a prolonged period.

Payback Period Example

A retail company seeks to expand by opening new store locations to broaden its market presence and drive revenue growth. The initial investment is only part of the equation; it is crucial to ascertain the payback period for these new stores.

Assuming that we are required to organize new shops by covering ground of ₹40,00,000 and that the stores will generate called for cash inflow of ₹20,00,000 per annum, the payback period is:

Payback period = initial investment/ Annual cash inflow

= ₹40,00,000/₹20,00,000

= 2 years

Years to Break-Even Formula

The years-to-break-even formula helps determine when an investment will generate profits beyond its initial cost.

- Years To Break-Even: The full years before the break-even point is met. In other words, it is the number of years the project remains unprofitable.

- Unrecovered Amount: The unrecovered amount is the negative balance for the year before the company has a positive cumulative net cash flow.

- Recovery Year Cash Flow: The company produced cash flow once the initial investment cost was recovered and profits were generated.

This formula is applied when enterprises have to consider overhead costs.

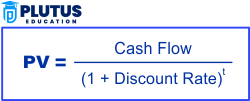

Discounted Payback Period Calculation Analysis

The discounted payback period formula adjusts future cash flows to reflect their present value.

This example uses the discounted payback period, which considers the time value of money, meaning that money received today is more valuable than the same amount received in the future.

- Initial Investment: ₹200 crore

- Annual Cash Flow: ₹60 crore

- Discount Rate: 10%

The cash flows are adjusted using the formula:

Compared to the basic payback period, this technique discounts each year’s cash flow before summing to determine when the total investment is broken even.

After using the formula, the break-even point comes between Year 4 and Year 5. As the balance amount to be recovered in Year 5 is ₹10 crore and the discounted cash inflow for the year is ₹37 crore, the additional fraction of the year required is:

₹10 crore/₹37 crore = 0.26 years

This translates to approximately 3 months or one-quarter of a year.

The firm breaks even in approximately 4 years and 3 months, including the time value of money. This method gives a better estimate of time to break even and is applicable for assessing long-term investments.

Payback Period Formula FAQs

What is the payback period formula?

Payback Period=Initial Investment/Annual Cash Inflows

What is the difference between discounted payback period and payback period?

The discounted payback period considers the time value of money, whereas the conventional payback period does not.

How is payback period calculated for uneven cash flows?

By accumulating cumulative cash flows annually and interpolating between years when the initial investment is being recovered.

What is the formula for payback period method?

It is applied in capital budgeting to analyze investment risk and recovery duration.

Why is discounted payback period more precise?

It considers inflation, interest rates, and money’s decreasing value over time.