Reasonable assurance is one of the most important concepts in auditing, and it describes the extent of confidence auditors provide regarding the accuracy and reliability of financial statements. It implies that auditors collect enough evidence to ascertain that the financial statements are free from material misstatements. It does not, however, ensure absolute accuracy because of limitations inherent in auditing. In this article, we’ll explore reasonable assurance, its examples, how to use it, and how it differs from limited assurance.

Reasonable Assurance Meaning

Reasonable assurance is the strong level of confidence auditors seek to attain when reviewing financial statements. It signifies that auditors obtain sufficient evidence to conclude that the financial statements are not material misstated, either by error or fraud. It does not imply absolute assurance, though, because audits are plagued by inherent limitations such as sampling risks and the risk of human error.

Auditors achieve a reasonable assurance level by applying standardized auditing practices and collecting sufficient and appropriate evidence. Statutory audits, for example, require this level of assurance, since stakeholders, such as investors or creditors, need to rely on the auditor’s opinion to make informed decisions. Not too burdensome or costly yet still enough to bring about some confidence in the reliability of financial statements.

Example of Reasonable Assurance

Reasonable assurance in auditing refers to the acquisition of adequate evidence that will ensure the authenticity and verifiability of financial statements. Auditors obtain this by sampling transactions, evaluating internal controls, and corroborating account balances through third parties.

- Testing a Sample of Transactions to Verify Their Accuracy: The auditors pick a few transactions to audit. They determine whether transactions comply with the rules and agree with the accounts. This allows them to detect errors or fraud quickly. The financial statements are considered to be audited, and they are reliable and trustworthy. It saves a lot of time from reviewing every single transaction.

- Assessing Internal Controls: One of the reasons why auditors review internal controls is to ensure they are effective. They investigate whether the controls protect against error, fraud or mismanagement. This step helps find holes in the system. Effective internal controls increase the efficiency and reliability of the organization. Auditors suggest ways to strengthen the controls further.

- Confirming Account Balances With Third Parties: Auditors confirm account balances with third parties such as banks or customers. They crosscheck the organization’s records against external sources for accuracy. This part helps to detect discrepancies or errors in the accounts. Balance confirmation gives the financial statements a higher level of credibility. It also helps to build trust with stakeholders and regulators.

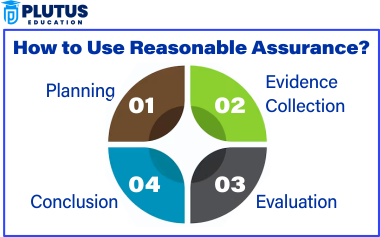

How to Use Reasonable Assurance?

Reasonable assurance involves a systematic approach to audit. Here’s how auditors apply it:

Planning

Auditors begin by carefully planning the audit. They learn about the client’s business, flag potential risks, and develop procedures to mitigate them. This gives a very big picture context so the audit not only looks at the right areas but it also knows what to expect within those areas. Proper planning saves time and enables auditors to do their job efficiently. It also offers that the audit effectively meets its objectives.

Evidence Collection

Gathered strong relevant evidence based on Business needs and strategy. They do so using tests of controls, substantive procedures and analytical review. This step allows them to validate the accuracy of financial records. Evidence collection, auditors must collect a cover weight to make credible conclusions about the financial statements.

Evaluation

The evidence auditors collect is closely scrutinized. They care if the evidence aligns with the truthfulness of the financial statements. This process enables them to discover errors, fraud or mismanagement; Evaluation makes sure that all audit results are just and supportable by valid evidence. It also prepares auditors for the final stage.

Conclusion

They use the evidence so collected to form opinions on the financial statements. They state whether the statements present a true and fair view of the client’s financial position. This statement is very important because for stakeholders this gives a strong trust and confidence in the economic health of the organization.

Importance of Reasonable Assurance

Reasonable assurance is vital in establishing confidence and dependability in financial reporting. Reasonable assurance guarantees that financial statements are reliable and free from material errors. Below are five reasons why reasonable assurance matters:

- Builds Stakeholder Confidence: Reasonable assurance provides strong assurance to stakeholders that financial statements are accurately presented. It can be trusted that the information is accurate and reliable for decision-making.

- Detects Errors and Fraud: Reasonable assurance requires completing comprehensive testing and gathering necessary evidence. By doing this, you can spot material misstatements in the financial books, errors, or even potential fraud.

- Improves Financial Transparency: Reasonable assurance improves the transparency of the financial statements by providing a high level of confidence. This level of transparency is vital to sustaining a company’s reputation and credibility.

- Ensures Compliance with Laws: It assists organizations in complying with laws and regulations. Statutory audits, which demand reasonable assurance, guarantee corporate compliance with financial reporting guidelines.

- Facilitates Better Decision Making: Accurate financial statements help management and stakeholders make the right decisions. Reasonable assurance ensures that the data they rely on is dependable and lacks material errors.

Reasonable Assurance vs Limited Assurance

Auditors give varying levels of assurance on their work based on the engagement type. Reasonable assurance provides a high level of trust, whereas limited assurance gives a moderate level. This helps stakeholders understand how much trust they can have in the findings of the audit. The following is a comparative analysis of their main features.

Reasonable Assurance

A reasonable assurance is a high level of assurance on your audit findings. The auditors have designed extensive procedures and obtained substantial evidence supporting their conclusions. This level of comfort for statutory audits of financial statements. The ultimate opinion is that the financial statements are free from material misstatement, which provides external parties with considerable confidence in the reported information.

Limited Assurance

Limited assurance has a middle level of assurance. Auditors rely on limited procedures like inquiries and analytical reviews rather than detailed testing. This method is typically used for review engagements, not full audits. Therefore, nothing has come to our attention that causes us to believe that, based on the limited work we have performed, there are material misstatements. It gives some level of assurance but not as extensive as reasonable assurance.

| Aspect | Reasonable Assurance | Limited Assurance |

| Level of Confidence | High | Moderate |

| Procedures | Extensive | Limited |

| Purpose | Statutory audits | Review engagements |

| Conclusion | Free from material misstatements | No material misstatements found |

Reasonable Assurance FAQs

What is reasonable assurance?

Reasonable assurance is the high confidence that auditors provide that financial statements are free from material misstatements.

What is assurance in auditing?

Assurance in auditing is the confidence auditors provide about the accuracy and reliability of financial information.

What is the difference between reasonable assurance and absolute assurance?

Reasonable assurance provides a high but not absolute level of confidence, while absolute assurance provides 100% accuracy, which is impossible in auditing.

What is a reasonable level of assurance?

A reasonable level of assurance means auditors have collected sufficient evidence to determine that financial statements contain no material misstatements.

How does reasonable assurance differ from limited assurance?

Reasonable assurance is a full process and provides great confidence, while limited assurance is a less complete process and provides moderate confidence.