An audit committee is an internal governing unit in an organization that monitors financial reporting, internal controls, risk management, and regulatory compliance to ensure financial accountability and transparency. The role of audit committee is to monitor the financial reporting process of a company, risk management, internal controls, and law compliance. An audit committee ensures that an organization remains transparent and accountable in terms of finance, and it protects investors and stakeholders. It is essential in corporate governance as it bridges the board of directors, management, and outside auditors.

What is Audit Committee?

An audit committee is a sub-group of the board of directors responsible for overseeing financial reporting, internal controls, and audit processes. Amenities of internal audit verifies the accuracy of financial statements, monitors regulatory compliance, and assesses the performance of both internal and external auditors.

In India, listed companies have been governed by the provisions of the Companies Act, 2013 and SEBI regulations, which make the formation of an audit committee compulsory. It also serves as a guardian to protect against fraud, mismanagement, and financial misreporting. The committee also helps to improve corporate governance by ensuring transparency and accountabilities.

Role of Audit Committee

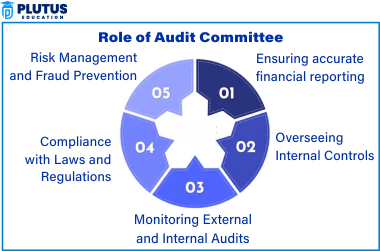

The role of audit committee is diverse, and it includes financial monitoring, risk management, and compliance. Following are the major roles and duties:

Ensuring accurate financial reporting

Audit committees ensure that financial statements provide accurate, complete, and relevant information by accounting standards. It collaborates closely with auditors to ensure the integrity of financial data. This position is vital to building trust with stakeholders and preventing financial fraud. In ensuring transparency, it bolsters investor confidence and promotes long-term financial stability.

Overseeing Internal Controls

The committee monitors the systems of internal control and risk management. It ensures that systems are established to identify and prevent errors, fraud, or other forms of mismanagement. Robust internal controls also promote efficiency while protecting assets. Frequent evaluation assists in spotting vulnerabilities early and taking corrective actions promptly.

Monitoring External and Internal Audits

The audit committee also nominates and assesses the external auditor’s performance. It also oversees the internal audit to ensure the function is independent and effective. This dual oversight helps comprehensively and impartially assess the organization’s financial condition. Frequent meetings with the auditors provide insights into new and emerging risks and help sustain audit quality.

Compliance with Laws and Regulations

It helps ensure the organization obeys the laws, rules, and regulations. It tracks changes in laws and advises the board about what needs to be done. Compliance minimizes the chances of being penalized and increases the organization’s credibility. It encourages ethical corporate governance by proactively taking the lead on regulatory changes.

Risk Management and Fraud Prevention

The audit committee determines and characterizes monetary and property risks. It employs processes to minimize these risks and avoid fraud. This approach ensures that the organization does not lose financially or suffer reputational losses. Risk Monitoring Continuously, the organization can monitor any risks that might arise over time, allowing the organization to adapt and improve with time and closing any gaps as threats evolve.

Audit Committee Regulations

Rules for an audit committee offer a regulated system designed to improve corporate governance, financial soundness, and openness. They help ensure that all companies are operating within sound financial and legal parameters and keep the nest egg from being eaten by fraud. They exist in various forms depending on jurisdictions but are a function of global corporate governance principles.

Composition and Independence

It shall consist of at least three members, the majority of which shall be independent directors, in order to ensure objectivity and the avoidance of conflicts of interest. The independence helps ensure that the financial oversight is done without undue influence from the management. Also, at least one member has to have accounting or finance knowledge so that financial reports, audits, and checks are reviewed with technical competence.

Roles and Responsibilities

Finally, the audit committee shall review for each financial statement the obtained statements for fairness, completeness, and compliance with accounting standards. It also is responsible for ensuring both internal and external auditors operate independently and effectively. Another important responsibility is to monitor internal controls and risk management processes to prevent and detect fraud. Additionally, the committee ensures that legal, regulatory, and ethical standards are met and advises the board on any necessary corrective actions when needed.

Appointment and Removal of Auditors

The audit committee has one of the most important responsibilities, which is to appoint, oversee, and discuss the external auditors. This helps to ensure that auditors remain independent and do not act in a biased manner. This prevents long-term dependence and possible conflict of interest, which is why regulations often mandate a rotation of auditors after a certain period.

Meetings and Reporting Requirements

Audit committees should meet at least four times yearly, with more frequent meetings as appropriate given the company’s financial reporting cycle and emerging risks. All the above key information gets reviewed by the committee in such meetings, including financials, auditing reports, compliance, and potential risks. Thus, each meeting needs to be carefully minuted for records, transparency, and accountability.

Compliance with Laws and Standards

Audit committees must guarantee strict compliance with them, as any violation on a local or international level could lead to risks and legal penalties. Here, regulatory frameworks, including the Sarbanes-Oxley Act (SOX) in the U.S., the Companies Act in India, Corporate Governance Code in UK and Europe, explain where the responsibility in audit oversight lies. Securities regulations also require companies to follow transparent and fair practices when reporting financial results to help protect investors.

Whistleblower Protection and Ethical Oversight

An important role of the audit committee is to create whistleblower systems through which employees and others can confidentially report fraud, financial misconduct, or unethical behavior. These mechanisms provide transparency and a systematic approach to investigating and rectifying any issues that have been reported. First off, each member of the committee is required to take corrective action to ensure that future fraud or wrongdoing does not occur.

Risk Management and Financial Oversight

The audit committee will now assist in detecting and mitigating financial, operational, and compliance-related risks. The committee routinely evaluates the threats, thus assisting organizations in avoiding financial uncertainties and fraud. It works with management to help ensure that effective risk controls are in place to protect the company’s assets and long-term financial health.

How to Form an Audit Committee?

Establishing an audit committee is not as simple as just picking two employees, it’s a complex process to form a proper audit committee. Here’s a step-by-step guide:

- Determine the Size and Composition: The audit committee should consist of three members, all of whom must be independent. At least one member must have relevant experience in accounting or finance. Having members with a diversity of skills and perspectives improves decision-making and oversight. This enhances the governance and accountability of financial management.

- Define Roles and Responsibilities: Define the committee’s missions and scope. Compliance with legal aspects and requirements of corporate governance. Update responsibilities periodically, including those for newly emerging risks and business sectors. Clear role definitions enhance accountability and operational effectiveness.

- Appoint Qualified Members: Share the responsibility with well-qualified members. Avoid conflict of interest by ensuring independence. Different backgrounds help build a more complete risk picture. Continuing education keeps members up to date on financial and regulatory developments.

- Establish a Charter: Formulate a charter to define the committee’s purpose, authority, and procedures. (regularly discuss and revise the charter to adapt to shifting needs.) An organised charter increases clarity and makes sure of consistent operations. Through periodic reevaluations, processes may be refined for increased efficiency.

- Conduct Regular Meetings: Hold regular meetings to discuss financial reports, audit findings, and compliance matters. Keep detailed minutes of what takes place and what is decided. Frequent engagements help manage and monitor issues before escalation and mitigate risk. Regular documentation provides transparency and aids in regulatory compliance.

Role of Audit Committee FAQs

What is the role of audit committee in corporate governance?

The audit committee promotes transparency, accountability, and compliance with legislation, enhancing corporate governance.

Who can be a member of an audit committee?

Members are usually independent directors with a financial background to provide unbiased supervision.

What are the role of audit committee?

The role involves monitoring financial reporting, internal controls, audits, compliance, and risk management.

Is an audit committee compulsory for all companies?

It is compulsory for listed companies and some other categories of companies under the Companies Act, 2013.

How Often Should an Audit Committee Meet?

The committee must meet at least four times annually, with extra meetings as and when required to discuss pressing matters.