The traditional approach of capital structure relates the financing mix of a company to its value. This theory asserts that an optimal capital structure exists such that the financing mix of debt and equity will minimise the cost of capital facing the firm while maximising firm value. It argues that a modest amount of debt enhances a firm value; however, excessive debt raises financial risk and undermines the advantages. The traditional approach supports the argument that leverage affects a firm’s value, but only to a point.

Capital structure decisions are critical to any firm because they directly impact profit, risk, and the entire corporation. The traditional theory prescribes that companies should combine equity and debt in their capital structure in such a fashion as to reduce their cost of capital and maximise shareholder wealth. The above also acts as a bridge between the Net Income Approach, which states that an increase in debt adds to the firm’s value, and the Net Operating Income Approach, which argues that capital structure is irrelevant in determining firm value.

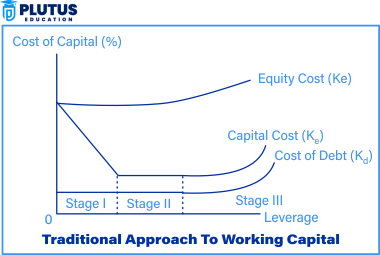

Traditional Approach of Capital Structure in Financial Management Meaning

Traditional capital structure theory maintains that the proportion of debt and equity capital used by the firm is mainly based on minimising the cost of capital. It states that debt proves to be an advantage until a certain level due to the tax benefits and low cost than equity. On the contrary, the moment a company risks too much debt, the higher the financial risks. Costs thus rise, and the value of the firm will go down.

The underlying argument is that capital structure influences the corporation’s market value but not in a straightforward, linear way. The beneficial effect of debt financing on the firm lasts only up to an extent called the optimal capital structure. Beyond that point, the costs associated with financial distress outweigh the benefits of using debt.

Elements of Traditional Approach of Capital Structure in Financial Management

The elements of traditional theory stand between two radical views of capital structure: one that argues for heavy debt in every situation as a blessing and the other that argues for capital structure as an irrelevant issue.

- Optimal Capital Structure: A mix of debt and equity exists that minimises the firm’s capital cost and maximises value.

- Non-Linear Impact: Initially, debt reduces the cost of capital, but excessive debt increases financial risk.

- Trade-Off Between Debt and Equity: Debt provides tax benefits, but too much debt leads to financial distress.

- Market Imperfections: Assumes market imperfections exist, making capital structure relevant.

Traditional Approach of Capital Structure Assumptions

The traditional capital structure approach has also been implemented in real business organisations. Hence, its examples have been given to make reading about the traditional capital structure approach effective.

Access to Capital Markets by Firms

Companies will mobilise their resources and abilities in both debt and equity markets. It assumes that companies now have the freely available market to structure their capital concerning the desired balancing in financing.

Debt Cheaper Than Equity

Interest payments that are tax deductible render debt financing cheaper than equity financing decisions. Debt is thus preferred for the funding through an option of tax loss since the interest pays off the cost.

An Optimal Capital Structure Exists

The traditional approach proposes that some definite debt and equity ratio maintains the minimum possible weighted average cost of capital for the firm. This presumes that the firm’s value is increased by the specific mix of debt and equity, which is more balanced than the others.

Excessive Debt Increases Financial Risk

However, excessive and high debt financing short term results in high-cost capital, credit downgrading and bankruptcy risks. This also implies that debt negatively affects the firm beyond a specific limit.

Market Imperfections Exist

Here, unlike those approaches of capital structure, which posit perfect capital markets, traditional approaches include features such as transaction costs, agency costs, and tax differences, which affect financing decision-making.

Investors React to Capital Structure Decisions

Equity is perceived differently from debt. Investors may regard an increase in borrowing as the corresponding increase in risk, thus possible changes in stock price and cost of capital.

Increase in Cost of Debt Beyond Optimal Point

At this optimum point, WACC decreases with an increase in debt. Still, for a company with very high levels of indebtedness, there is expected to be a higher cost of capital because creditors would need to charge higher interest rates due to their greater risk exposure.

Traditional Approach of Capital Structure in Financial Management Examples

The examples manifest how individual firms create their capital structure profiles, which differ appreciably per the industry structure and risks.

Example 1: Automobile Industry – Tata Motors

Tata Motors uses a capital structure, which an automobile financing company follows because it is optimal for neither too much nor more balanced cap models. Tata Motors borrows for expansion but refrains from exceeding optimal debt levels, which benefits them in tax savings due to interest charges without increasing the financial risk. In the downturns, the risk profile would quickly increase due to high debt and limited borrowing.

Technology Sector – Infosys

Infosys has an equity capital model that is different from debt capital. It minimises the financial risks that the high dependency on debt can cause. The traditional theory is accepted to discuss the shape of debt that should be used by companies such as Infosys. In contrast, it advises using debt for cash-conservative companies, while revenue-volatile firms may restrict the use of debt.

Retail Sector- Reliance Retail

Reliance Retail combines debt with equity financing, whereby it borrows money for specific projects and expansions while adhering to its required level of debt to avoid financial distress. The above strategy is similar to that of the traditional approach, which states that some debt is good for the company, but borrowing too high may bring financial instability.

Relevance to ACCA Syllabus

The ACCA syllabus covers capital structure decisions under Financial Management (FM) and Advanced Financial Management (AFM). Understanding the traditional approach helps evaluate capital costs, risk assessment, and business financing choices. Candidates of ACCA must analyse financial statements, cost of debt/equity, and weighted average cost of capital (WACC) calculations.

Traditional Approach of Capital Structure ACCA Questions

Q1. According to the Traditional Approach of Capital Structure, what happens when a company initially increases debt financing?

A) The cost of equity falls, and overall cost of capital increases

B) The cost of capital remains constant

C) The overall cost of capital decreases due to tax benefits of debt

D) The company’s risk remains unchanged

Ans: C) The overall cost of capital decreases due to tax benefits of debt

Q2. Which factors influence a firm’s capital structure under the Traditional Approach?

A) Tax benefits of debt

B) Cost of financial distress

C) Agency costs

D) All of the above

Ans: D) All of the above

Q3. In the Traditional Approach, why does excessive use of debt increase a firm’s cost of capital?

A) Debt financing always has a higher cost than equity

B) Excessive debt increases the risk of financial distress, raising the cost of equity

C) Investors prefer firms with no debt

D) Interest expenses decrease, leading to higher costs

Ans: B) Excessive debt increases the risk of financial distress, raising the cost of equity

Q4. What happens to Weighted Average Cost of Capital (WACC) when a firm takes on moderate debt, according to the Traditional Approach?

A) WACC decreases due to cheaper debt financing

B) WACC increases due to higher risk

C) WACC remains constant

D) WACC is not affected by debt levels

Ans: A) WACC decreases due to cheaper debt financing

Q5. At what point does the cost of capital increase under the Traditional Approach?

A) When a firm reaches the optimal capital structure

B) When financial risk starts affecting the cost of equity

C) When the proportion of debt remains constant

D) When a firm has no debt in its capital structure

Ans: B) When financial risk starts affecting the cost of equity

Relevance to US CMA Syllabus

The Certified Management Accountant (US CMA) syllabus covers capital structure in Part 2: Financial Decision Making. Candidates of CMA must understand how financing decisions affect a firm’s risk, value, and cost of capital. The Traditional Approach is tested in questions related to WACC, leverage analysis, and risk-return trade-offs.

Traditional Approach of Capital Structure US CMA Questions

Q6. According to the Traditional Approach, what is the key benefit of using a moderate level of debt?

A) Higher interest payments

B) Lower tax benefits

C) Reduction in the overall cost of capital

D) Increased default risk

Ans: C) Reduction in the overall cost of capita

Q7. Why does excessive debt lead to an increase in WACC under the Traditional Approach?

A) Higher interest costs reduce net income

B) Increased financial distress raises the cost of equity

C) Debt financing eliminates the tax benefit

D) The firm avoids risk exposure

Ans: B) Increased financial distress raises the cost of equity

Q8. Which component is NOT directly considered in the Traditional Approach to capital structure?

A) Debt financing

B) Cost of bankruptcy

C) Market value of the firm

D) Net working capital

Ans: D) Net working capital

Q9. At the optimal capital structure in the Traditional Approach, which of the following is minimized?

A) Cost of equity

B) Cost of debt

C) Weighted Average Cost of Capital (WACC)

D) Leverage ratio

Ans: C) Weighted Average Cost of Capital (WACC)

Q10. Under the Traditional Approach, a firm should increase leverage until which point?

A) When debt is cheaper than equity

B) When the firm’s tax rate is maximized

C) When the cost of capital starts increasing due to risk

D) When investors demand higher dividends

Ans: C) When the cost of capital starts increasing due to risk

Relevance to US CPA Syllabus

The Certified Public Accountant (US CPA) syllabus covers capital structure decisions in the Financial Accounting and Reporting (FAR) and Business Environment & Concepts (BEC) sections. Candidates of CPA must analyse financial leverage, cost of capital, and capital structure impact on financial performance.

Traditional Approach of Capital Structure US CPA Questions

Q11. Which of the following best describes the Traditional Approach to capital structure?

A) Capital structure does not affect firm value

B) There is an optimal capital structure that minimizes WACC

C) Equity financing is always cheaper than debt financing

D) Debt financing should always be avoided

Ans: B) There is an optimal capital structure that minimizes WACC

Q12. Which of the following is an assumption of the Traditional Approach?

A) Capital markets are always efficient

B) Firms have no bankruptcy costs

C) Debt is cheaper than equity up to a certain level

D) The cost of capital is independent of financing decisions

Ans: C) Debt is cheaper than equity up to a certain level

Q13. What is the primary goal of capital structure management under the Traditional Approach?

A) Maximizing leverage

B) Minimizing the tax rate

C) Minimizing WACC and maximizing firm value

D) Maintaining a 50:50 debt-equity ratio

Ans: C) Minimizing WACC and maximizing firm value

Q14. Why do firms avoid excessive leverage under the Traditional Approach?

A) Because debt does not provide any benefit

B) Because the cost of equity rises due to financial distress risk

C) Because equity holders always prefer zero debt

D) Because interest on debt is not tax deductible

Ans: B) Because the cost of equity rises due to financial distress risk

Q15. According to the Traditional Approach, how does debt financing initially affect a firm’s value?

A) It increases firm value due to tax shields

B) It has no effect on firm value

C) It decreases firm value immediately

D) It leads to higher equity issuance

Ans: A) It increases firm value due to tax shields

Relevance to CFA Syllabus

The CFA (Chartered Financial Analyst) syllabus covers capital structure theories in Corporate Finance under Level 1 & 2. CFA candidates must analyse how financing decisions impact the cost of capital, risk, and shareholder value.

Traditional Approach of Capital Structure CFA Questions

Q16. What is the key premise of the Traditional Approach in capital structure?

A) Capital structure is irrelevant

B) An optimal mix of debt and equity minimizes WACC

C) Equity financing is always better than debt financing

D) Debt financing does not impact firm value

Ans: B) An optimal mix of debt and equity minimizes WACC

Q17. How does the Traditional Approach differ from Modigliani-Miller (M&M) Proposition I without taxes?

A) M&M assumes capital structure is irrelevant, while Traditional Approach suggests an optimal structure exists

B) M&M favors debt financing, while Traditional Approach favors equity financing

C) The Traditional Approach assumes no bankruptcy costs

D) M&M considers cost of equity as fixed

Ans: A) M&M assumes capital structure is irrelevant, while Traditional Approach suggests an optimal structure exists

Q18. Which factor increases the cost of equity in a highly leveraged firm under the Traditional Approach?

A) Reduced operating income

B) Increased financial distress risk

C) Lower tax rates

D) Increased retained earnings

Ans: B) Increased financial distress risk

Q19. What is the relationship between leverage and cost of capital under the Traditional Approach?

A) WACC initially decreases with leverage, but then rises after an optimal point

B) WACC remains constant regardless of leverage

C) WACC only increases with leverage

D) Leverage does not impact cost of capital

Ans: A) WACC initially decreases with leverage, but then rises after an optimal point

Q20. Which element is crucial in determining the optimal capital structure?

A) Dividend payout ratio

B) Market efficiency

C) Financial distress costs

D) Earnings per share

Ans: C) Financial distress costs