Audit assertions serve as a means for auditors to ensure that financial statements are accurate and complete. The types of audit assertions are designed to provide a specific company’s adherence to accounting principles. Assertion is the representation of management of financial information in reports in words. Auditors employ these assertions to judge whether any errors are present in financial information or whether it is fraud-free.

They would use different types of audit assertions to verify financial data. Such audit assertions would confirm the existence of recorded transactions, the accuracy of assets and liabilities, and the conformity of disclosures on an appropriate accounting basis. The types of audit assertions include assertions related to transactions, account balances, and presentations and disclosures. All these ensure that the truth is reflected in a company’s financial statements.

Auditors check other criteria about financial statements to ascertain their accuracy. These audit assertions help them analyse whether an entity has accurately reported revenues, expenses, assets, and liabilities. This is an essential dimension for protecting investors and other stakeholders against giving out misleading financial reports. Audit assertions provide better knowledge for making compliance and transparency in organizations.

What is Assertion Meaning in Audit?

Auditing assertions are the assertions of management when considering financial statements. These assertions are that the economic data are accurate, complete, and conform to accounting standards. Auditors then tend to inquire into these assertions to ascertain whether the financial statements portray an accurate and fair view of the company’s financial position.

Audit assertions are the ones that let auditors know the chances of fraudulent financials, errors, or misstatements in financial statements. Audit assertions will be the compass in the audit process while assessing the financial statements. Accounting principles concerning transactions and balances have conformed, and compliance requirements have been met.

Audit assertions have a significant basis in financial auditing. They allow auditors to measure the reliability of financial statements by evaluating completeness, existence, rights and obligations, valuation aspects, etc. Without such assertions, auditors cannot say anything about financial data regarding its free material misstatement.

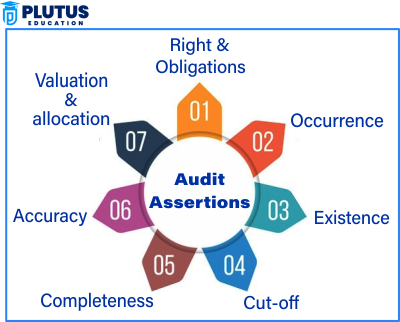

Types of Audit Assertions

Under audit assertions all different types will come into the category of audit assertions, which could be very helpful for auditors in proving the accuracy of the financial records. The principal categories of audit assertions are transaction, account balance, and presentation and disclosure assertions. As the name suggests, each one has a further list of subtypes under it that complete the verification of the financial data.

Transaction Assertions

Whether the financial transactions that are recorded are accurate and complete are verified through these transaction assertions. These assertions deal with the fact that the financial transactions exist and comply with the accounting standards.

Occurrence

This assertion ensures that recorded transactions occurred. Auditors check whether the transactions took place and are not fraudulent.

Example: A company reports revenue from sales. Auditors must confirm that sales occurred by checking invoices and receipts.

Completeness

This assertion states that every financial transaction is recorded; auditors check for missing transactions.

Example: Auditors check that no revenue transaction is left unrecorded when a company earns revenue.

Accuracy

This assertion states that financial transactions must be recorded with correct monetary values. There should be no error in calculation or data entry.

Example: Auditors verify salary payments of all employees against records in the payroll.

Cut-off

This assertion validates that transactions are recorded within the appropriate accounting period.

Example: If a sale happens on December 31, it should be recorded this year and not in the next year.

Classification

This assertion ensures that transactions are recorded under the right financial category.

Example: An expense would not be counted as an asset.

Account Balance Assertions

Account balance assertions relate to asset, liability, and equity balances presented by financial statements. The assertions confirm accurate and representational values of account balances regarding absolute values.

Existence

This assertion ensures that recorded assets, liabilities, and equity balances exist.

Example: When a company states it has $1 million worth of inventory, auditors ask if they could see that inventory.

Completeness

This assertion states that financial balances are recorded in the financial statements.

Example: Auditors make sure there’s no liability unrecorded.

Rights and Obligations

The affirmation states that the assets belong to the company; thus, the company has legal liability for paying the obligations.

Example: Auditors would be checking property ownership documents against buildings reported in the company’s balance sheet.

Valuation and Allocation

This assertion also says that assets and liabilities are valued, estimated, and allocated according to accounting standards.

Example: If the company has machinery, it will check that there is a proper recording of depreciation.

Presentation and Disclosure Assertions

The presentation and disclosure assertions verify both the integrity of the presentation and that all financial data included in the financial statements should be presented and disclosed correctly. Report clarity is given through these assertions, and regulations can be adhered to in generating financial reports.

Occurrence and Rights and Obligations

This assertion requires that all the disclosed information is relevant to the entity and occurred during the reporting period. For example, Auditors check that the lease contracts disclosed pertain to the entity and are valid.

Completeness

This assertion guarantees that financial statements contain all such disclosures which are necessary. For example, Auditors confirm that finical reports contain pending litigations.

Classification and Understandability

This assertion adjoins itself to establishedness that financial inferences are duly classified and easily comprehensible. Example: Auditors look into whether made provision for contingent liabilities in adequate terms that can be understood by stakeholders.

Importance of Assertions in Auditing

Auditing assertions helps verify the company’s financial aspects. The financial statements will be an accurate and fair representation of the company’s worth without these assertions. Reliability in the economic data would never be possible with the absence of these assertions.

- Fraud Detection: Help auditors specific allegations regarding fraudulent transactions and misstatements in their financial statements.

- Ensuring Compliance: Assertions are useful in ensuring the financial reports comply with the applicable accounting standards and regulations.

- Protection of Stakeholders: Financial statements can be instruments that—besides defining the general situation of a company—also determine when it is necessary for an investor, creditor, or regulator to make a decision.

- Financial Transparency Improvement: Assertions contribute to making financial reporting transparent and trustworthy.

- Reducing Errors: Assertions minimise errors in financial statements and ensure accurate reporting.

Audit Assertions ASB Standards

The Accounting Standards Board (ASB) standard assertions tell auditors about the examination of financial statements for public and private entities. The assertions guide auditors in ascertaining transactions, account balances, and disclosures.

The ASB has put forth the following three main categories of assertions:

- Assertions concerning classes of transactions and events

- Assertions concerning account balances

- Assertions concerning presentation and disclosures

Each assertion helps ascertain financial statements’ accuracy, completeness, and presentation.

Assertions About Classes of Transactions and Events

These assertions concern revenue, expenses, and other transactions. They ensure that the proper recording and classification of transactions have been done.

- Occurrence Assertion: This assertion ensures that all recorded transactions happen. Auditors look out for fake sales as well as fraudulent purchases.

- Completeness Assertion: The completeness assertion in an audit ensures that all the transactions are recorded. Auditors verify the financial records for missing transactions.

- Accuracy Assertion: Under the accuracy assertion in an audit, the transactions have been appropriately recorded. The auditors examine invoices, receipts, and financial documentation.

- Cutoff Assertion: This confirms that transactions have been recorded in the proper period. The auditors check year-end transactions.

- Confirmation of Classification: Assertions ensure that the transactions are correctly classified or presented in financial statements. The misclassification might confuse the stakeholders.

Transaction assertions help an auditor detect errors and fraud in the accuracy of financial statement reporting. Auditors will check whether transactions relate to:

- Complete and Proper Classification

- Accurate Recording

- Validity and Authorization

- Presentation in compliance with Accounting Principles

- Key Assertions Regarding Transactions

Assertions About Account Balances

The existence assertion in the audit, completeness, valuation, and rights/obligations assertions are subsumed in this. Auditors apply the verification of the accuracy of balance sheet items to them. Assertions about account balances facilitate the auditors in verifying the accuracy as far as balances of assets, liabilities, and equity; such assertions enable the financial statements to reflect the actual position of a company. Such assessments are as follows:

- Existence Assertion: The existence assertion in the audit affirms that reported assets and liabilities exist. Corporal audit verification will use auditors’ evidence to establish possible assets and liabilities through bank(s) balance verification.

- Completeness Assertion: This assertion ensures that all assets and liabilities are recorded. All missing liabilities can mislead the investors.

- The valuation assertion states that assets and liabilities should be recorded at actual values. Auditors consider examining depreciation, inventory valuation, and impairment losses during the audit.

- Rights and Obligations Assertion: These assertions ensure the company’s legal title to its assets. The auditors examine documentation and agreements.

Claims referring to account balances are valuable in identifying financial misstatements and, more importantly, in the prevention of such misstatements.

Assertion on Presentation and Disclosure

These assertions relate to whether information about presentation and disclosure standards is complete and presentable. Auditors assess the adequacy of the notes and supplementary disclosures. With that, ASB standard assertions are being applied by auditors in structured audits to uphold the credibility of financial reporting.

Types of Audit Assertion FAQs

1. Why are audit assertions important?

Audit assertions verify how factual or erroneous financial statements are. They give auditors the confidence to assert that all transactions, balances, and disclosures comply with accounting standards in form and percentage and are free from errors and fraud.

2. What are the main types of audit assertions?

Transaction assertions, account balance assertions, and presentation and disclosure assertions are three main types. The auditors can use them to verify various aspects of financial data.

3. What is completeness assertion in an audit?

The completeness assertion in an audit ensures that all transactions, balances, and disclosures are comprehensive. Auditors check if liabilities, revenue, or expenses are missing.

4. What does accuracy assertion mean in an audit?

The accuracy assertion makes it possible for auditors to put checks on invoices, financial reports, and calculations that record information in the financial statements.

5. Why are management assertions essential?

Management assertions in the audit are essential because they provide the basis upon which an auditor assesses the financial statements. These assertions help detect fraud and misstatement and help in transparency in financial reports.