The exchange of interest rate payments between two parties over a specified period is an interest rate swap. These instruments are widely utilized by businesses and financial institutions to hedge interest rate risk, lower borrowing costs, or protect against interest rate fluctuations. The most common interest rate swaps involve the fundamental interest rate swaps, where fixed and floating interest rates are exchanged; fixed-for-floating swaps, which involve the payment of a fixed interest rate by one party and the payment of a floating interest rate by the other party; and floating swaps, which involve the exchange of floating rates by both the counterparties based on different benchmarks. Other forms are basis swaps, where two different floating rates are exchanged, and amortizing swaps, where principal amounts reduce in time. They serve as a means to a greater degree of flexibility in reshaping financial operations, allowing companies to level out interest expenses in a distressed market.

What is Interest Rate Swap?

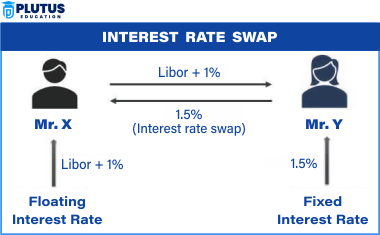

An Interest Rate Swap can be defined as a generally derivative financial contract between the two parties exchanging interest payments related to a specific principal amount. The objective is mostly to hedge some risk or reduce the costs of borrowing.

How Does It Works?

One party agrees to pay a fixed interest rate and then receive floating interest (e.g., market-based LIBOR, SOFR or EURIBOR).

- The other party does the opposite: floating and receiving a fixed rate.

- Again, principal (called notional amount) is never exchanged- meaning interest payments are exchanged.

Types of Interest Rate Swaps

Interest rate swaps are contracts in the financial market that manage interest rate risk. The needs of the parties involved can distinguish them. Some companies would rather pay a fixed interest rate for a floating rate; the reverse holds for firms, and investors using these contracts must understand the workings of an interest rate swap.

Plain Vanilla Interest Rate Swap

The plain vanilla interest rate swap is the most fundamental and popularly used form. In the agreement, one of the counterparties contracts to pay a fixed interest rate, while the other counterparty pays a floating rate based on a market rate such as LIBOR or SOFR. The differential between the two rates determines the cash flow for the interest rate swaps. If the floating rate is above the fixed rate, the party paying the floating rate stands to gain. In contrast, if the floating rate is below the fixed rate, the party paying the fixed rate stands to gain.

For instance, Company A may have a loan with a floating interest rate and think the rates will increase. Thus, Company A enters into an interest rate swap agreement with Company B, which wants a floating rate. Company A pays a fixed rate and receives a floating rate; thus, effectively, it converts its loan into a fixed obligation.

Basis Swap

In a basis swap, one floating interest rate is exchanged for another floating rate, typically linked to different benchmarks. The idea is to remedy mismatches in interest rate benchmarks, thus establishing an essential element in comparing basis swaps vs interest rate swaps. These swaps act as a hedge for financial institutions with inconsistent types of floating rate exposures.

For example, the bank may receive LIBOR but pay SOFR. Using a basis swap, the bank resolves the principal risk associated with those benchmarks.

Cross-Currency Interest Rate Swap

Two or more parties can convert the interest payments and principal amounts from one currency into the cash flows in another with the help of a cross-currency interest swap. These swap benefits incorporate a corporation or institution doing business in one country but have risks owing to currency movement in its multinational locations. They permit such companies to receive financing in a currency while having reduced their currency conversion risk.

For instance, a European company borrows money from the United States. To convert the dollar loan to euro payments, a cross-currency swap is entered into, and this arrangement guarantees a fixed foreign exchange rate between the euro and the dollar on the interest outflows calculated in those currencies towards operational transactions. Principal and interest payments are exchanged on a predetermined schedule.

Forward Rate Agreement vs Interest Rate Swap

The comparison of forward rate agreements to interest rate swaps highlights key differences between the two in terms of even more underlying structures and actual purposes. Forward rate agreements (FRAs) are contracts that lock in an interest rate for a future period. In contrast, interest rate swaps stretch across an uninterrupted series of interest payments for longer. FRAs thus help hedge short-term interest rate risks, while swaps provide long-term interest rate management solutions.

Floating Interest Rate vs Fixed Interest Rate Swap

The floating interest rate versus fixed-rate swap discusses predictable cash flow versus potential savings. When companies expect rising interest rates, a fixed-rate swap is favoured; a floating-rate one is usually preferred if the expectation is lower. Decisions depend on market conditions, appetite, and financial strategy.

Interest Rate Swap Risks and Benefits

Interest rate swaps bring with them several benefits; however, there are associated risks that the parties must consider. Some risks related to interest rate swaps are market, counterparty and valuation risks. The benefits of rate swaps include the cheaper cost of debt, risk management, and improved financial dynamics.

Risks of Interest Rate Swaps

- Market Risk – Fluctuations in interest rates change the value of the swap contracts: a corporation incurs higher costs if the rates shift against its interests.

- Counterparty Risk – The risk of incurring losses if the counterparty to the swap defaults; this is more critical in long-term contracts.

- Liquidity Risk – Unwinding some swaps before maturity can be very difficult, thus placing some participants in a difficult position to extricate themselves from unfavourable contracts.

- Regulatory Risk – Changes in regulations, such as hedge accounting rules for interest rate swaps, impact how companies treat swaps in their financial statements.

- Valuation Complexity – The interest rate swap valuation process demands knowledge of complex models and market data, creating difficulty in some companies accurately evaluating their positions.

Benefits of Interest Rate Swaps

- Hedging Interest Rate Risk – Companies hedge interest rate risk in a forward sense by using swaps to secure stable financing costs regardless of rising or falling interest rates.

- Lower Borrowing Costs– Swaps offer an alternative means by which a corporation obtains a cheaper interest cost by taking advantage of the prevailing market conditions.

- Flexibility in Financial Management with the Use of Swaps- Firms could adjust their interest rate exposure without editing or altering their existing loans and bonds.

- Improved Management of Cash Flows – Corporates can manage their cash flow more efficiently through increased stability of interest payments.

- Access to International Markets – Products like the cross-currency interest rate swap make it easier for companies to manage adequate international funding and currency exposure.

Interest Rate Swap Example and Valuation

An example of an interest rate swap is crucial to understand better how these contracts operate. For example, a company has a loan of $10 million with a floating interest rate equal to LIBOR + 2%. The company expects interest rates to increase, so it produces a swap that pays a fixed 5% and receives LIBOR. In other words, if LIBOR goes up to 4%, the company will pay only 5% instead of 6%(LIBOR + 2%).

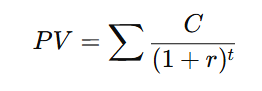

The interest rate swap formula for valuation considers the present value of future cash flows. To arrive at this, one uses basic discounted expected payment at appropriate discount rates.

C represents cash flows, r is the discount rate, and t is the period.

Relevance to ACCA Syllabus

Interest rate swaps are a crucial topic in the ACCA syllabus, particularly under Financial Management (FM) and Advanced Financial Management (AFM) papers. Understanding different types of interest rate swaps helps ACCA candidates analyse financial risk management techniques, hedge interest rate fluctuations, and advise businesses on financial instruments. This topic’s mastery is vital for corporate finance, treasury, and investment banking roles.

Types of Interest Rate Swaps ACCA Questions

Q1: Which type of interest rate swap involves one party paying a fixed interest rate and receiving a floating rate?

A) Basis Swap

B) Fixed-for-Floating Swap

C) Zero-Coupon Swap

D) Callable Swap

Ans: B) Fixed-for-Floating Swap

Q2: A company enters into an interest rate swap agreement to exchange a floating rate based on LIBOR for another floating rate based on SOFR. What type of swap is this?

A) Basis Swap

B) Fixed-for-Fixed Swap

C) Inflation Swap

D) Amortizing Swap

Ans: A) Basis Swap

Q3: In a zero-coupon swap, how is the interest paid?

A) Interest is paid periodically throughout the swap term

B) No interest payments are made until the maturity date

C) Interest is paid only in the first year

D) Interest payments are made at a variable frequency

Ans: B) No interest payments are made until the maturity date

Q4: A callable interest rate swap allows which party the right to terminate the swap early?

A) The floating rate payer

B) The fixed-rate payer

C) Either party, based on mutual agreement

D) The party that initially received the swap premium

Ans: B) The fixed rate payer

Q5: What is the primary purpose of an amortising interest rate swap?

A) To adjust for currency fluctuations

B) To hedge exposure to changing interest rates on a decreasing loan balance

C) To extend the maturity of a swap contract

D) To increase leverage in a portfolio

Ans: B) To hedge exposure to changing interest rates on a decreasing loan balance

Relevance to US CMA Syllabus

The US (Certified Management Accountant) CMA syllabus covers financial risk management, including derivatives and hedging strategies. Interest rate swaps are critical for treasury and risk management professionals who need to manage cash flow risks in corporate finance. This knowledge is applied in financial strategy and performance management modules.

Types of Interest Rate Swaps US CMA Questions

Q1: Which type of interest rate swap best suits a company wanting to hedge against rising interest rates?

A) Floating-for-Floating Swap

B) Fixed-for-Floating Swap

C) Zero-Coupon Swap

D) Inflation Swap

Ans: B) Fixed-for-Floating Swap

Q2: If a company has a variable rate debt and wants to stabilise its interest payments, which type of swap would it use?

A) Basis Swap

B) Fixed-for-Fixed Swap

C) Fixed-for-Floating Swap

D) Commodity Swap

Ans: C) Fixed-for-Floating Swap

Q3: In an inflation swap, what do the parties exchange?

A) A fixed rate for a floating rate

B) A nominal cash flow for an inflation-adjusted cash flow

C) A variable rate for a fixed rate

D) A fixed interest rate for a zero-coupon bond

Ans: B) A nominal cash flow for an inflation-adjusted cash flow

Q4: Why might a firm use a callable interest rate swap?

A) To hedge against exchange rate fluctuations

B) To terminate the swap early if interest rates move favourably

C) To extend the maturity of a fixed-rate loan

D) To increase its credit rating

Ans: B) To terminate the swap early if interest rates move fav move, which type is commonly used when companies want to convert debt from fixed to floating while reducing overall interest costs?

A) Zero-Coupon Swap

B) Amortizing Swap

C) Basis Swap

D) Fixed-for-Floating Swap

Ans: D) Fixed-for-Floating Swap

Relevance to US CPA Syllabus

The US (Certified Public Accountant) CPA syllabus includes interest rate swaps under Financial Accounting & Reporting (FAR) and Business Environment & Concepts (BEC). CPAs must understand how swaps impact financial statements, hedge accounting, and regulatory compliance under US GAAP and IFRS.

Types of Interest Rate Swaps US CPA Questions

Q1: Under US GAAP, how should a fair-value hedge involving an interest rate swap be reported?

A) Recognized at fair value with gains/losses in OCI

B) Recognized at cost with no impact on financial statements

C) Recognized at fair value with gains/losses in the income statement

D) Not recognised unless exercised

Ans: C) Recognized at fair value with gains/losses in the income statement

Q2: A company with a floating-rate loan wants to swap it for a fixed rate to reduce interest expense volatility. What type of swap should it use?

A) Fixed-for-Floating Swap

B) Basis Swap

C) Amortizing Swap

D) Zero-Coupon Swap

Ans: A) Fixed-for-Floating Swap

Q3: What does the notional principal represent in an interest rate swap?

A) The amount exchanged between parties

B) The amount on which interest payments are calculated

C) The amount paid at the end of the swap

D) The fixed rate agreed in the swap

Ans: B) The amount on which interest payments are calculated

Q4: Which type of swap is best for a company managing a loan with decreasing principal over time?

A) Basis Swap

B) Amortizing Swap

C) Zero-Coupon Swap

D) Callable Swap

Ans: B) Amortizing Swap

Q5: How are unrealised gains or losses on interest rate swaps typically reported under IFRS?

A) Directly in the statement of cash flows

B) As part of OCI (Other Comprehensive Income)

C) As part of operating income

D) They are not recognised until settlement

Ans: B) As part of OCI (Other Comprehensive Income)

Relevance to CFA Syllabus

Interest rate swaps are a core part of the CFA curriculum, particularly under the Fixed Income and Derivatives sections. CFA candidates must understand swap pricing, valuation, risk management, and applications in investment strategies.

Types of Interest Rate Swaps CFA Questions

Q1: What is the primary risk involved in interest rate swaps?

A) Inflation Risk

B) Credit Risk

C) Interest Rate Risk

D) Sovereign Risk

Ans: C) Interest Rate Risk

Q2: Which financial institution typically arranges and facilitates interest rate swaps?

A) Hedge Funds

B) Investment Banks

C) Government Agencies

D) Retail Banks

Ans: B) Investment Banks

Q3: In a basis swap, what is exchanged?

A) A fixed rate for a floating rate

B) A floating rate based on one index for a floating rate based on another index

C) A nominal rate for an inflation-adjusted rate

D) A short-term rate for a long-term rate

Ans: B) A floating rate based on one index for a floating rate based on another index

Q4: Why do financial institutions engage in interest rate swaps?

A) To speculate on exchange rates

B) To hedge against interest rate fluctuations

C) To reduce transaction costs in bond trading

D) To increase loan demand

Ans: B) To hedge against interest rate fluctuations

Q5: What is the main component to discount future cash flows in swap valuation?

A) LIBOR or SOFR curves

B) Stock Market Returns

C) Federal Reserve Interest Rate

D) Dividend Yield

Ans: A) LIBOR or SOFR curves