Valuation of equity shares determines the fair market value of a company’s equity shares. It assists investors, companies, and financial analysts make investment, merger, acquisition, and financial reporting decisions. Valuation of equity shares is vital for companies raising funds, issuing shares, or fixing the price of valuation of sweat equity shares for employee remuneration. Knowing various valuation methods enables investors to determine whether a stock is overvalued or undervalued.

Valuation of Equity Shares Meaning

Valuation of equity shares is the process of estimating the value of a company’s equity using several financial parameters like earnings, assets, market movements, and future growth prospects. It assists businesses, investors, and regulatory agencies evaluate a company’s financial position and investment potential.

Who Uses Equity Valuation?

Equity valuation is applied by businesses, fund managers, financial analysts, and investors to determine a firm’s actual worth. Investors estimate stock prices for purchasing or selling shares; businesses apply it in mergers and acquisitions and financial planning, whereas banks and finance institutions use equity valuation to consider loan risks and investing opportunities. Government agencies also apply it to regulatory decisions and taxing assessments. It also assists private companies and startups get investors by highlighting their market worth.

Methods of Valuation of Equity Shares

Various valuation of equity shares methods assist in ascertaining the fair price of shares using various financial models and market situations. The most widely employed methods are:

Net Asset Value (NAV) Method

The net asset value (NAV) approach estimates the value of a firm’s equity by deducting its total liabilities from total assets and dividing the result by the number of outstanding equity shares. This approach is most appropriate for firms with major tangible assets like real estate or manufacturing companies. It might not be appropriate for service-oriented companies dependent on intangible assets like brand value and goodwill. NAV makes investors aware of the book value of shares but not the potential future earnings.

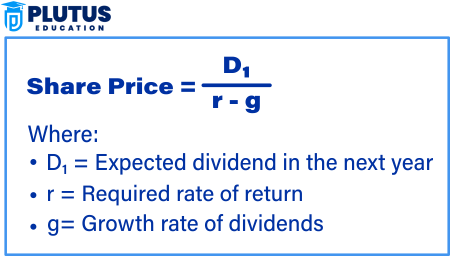

Dividend Discount Model (DDM) Method

The dividend discount model (DDM) prices shares based on anticipated future dividends. It presumes that the present value of a firm is given by its future dividend payments discounted at a rate of return that the investor requires. This model works for firms paying constant and frequent dividends. However, it fails to account for capital appreciation and non-dividend-paying firms. The DDM relies on a steady dividend growth rate, which might not always be true in fluctuating market conditions.

Price-to-Earnings (P/E) Ratio Method

The price-to-earnings (P/E) ratio approach determines the share price by multiplying the market P/E ratio with the company’s earnings per share (EPS). This approach is commonly applied to listed companies because it considers market expectations and sentiment. The P/E ratio differs between industries and depends on market trends, company performance, and economic factors. As this approach relies on market valuations, it might prove unreliable for companies with volatile earnings or those in growth industries.

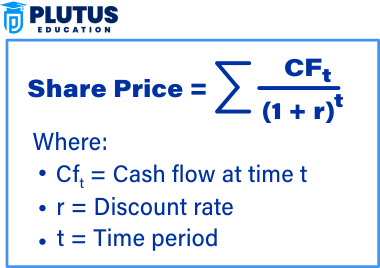

Discounted Cash Flow (DCF) Method

The discounted cash flow (DCF) approach values a company’s shares by computing the present value of its projected future cash inflows. It applies a discount rate factor to consider the time value of money so that future profits are properly valued in the present period. This approach is optimum for firms with solid projected cash flows and high long-term growth prospects. However, precise forecasting is important since varying the discount rate or assumption of revenues can substantially affect the valuation.

Valuation of Sweat Equity Shares

Valuation of sweat equity shares is necessary when firms give shares to employees in return for their skills and services. It is calculated by employing three primary methods. The Market Value Method is based on the prevailing market price of shares. The fair value method employs financial analysis to determine worth, whereas the cost method computes valuation based on the cost of services rendered. These methods ensure that firms compensate employees justly while keeping proper books of accounts.

Valuation of Equity Shares Example

XYZ Ltd. wants to calculate the Net Asset Value (NAV) per share to determine its equity share valuation. The company’s total assets and liabilities are given below:

| Particulars | Amount (₹ Crore) |

| Total Assets | ₹500 |

| Total Liabilities | ₹200 |

| Number of Equity Shares | 10 crore |

NAV per Share = (500-200)/10

= 300/10

=₹30

The net asset value (NAV) of each equity share of XYZ Ltd. is ₹30. This implies that if the company is priced based on its assets and liabilities, every share is worth ₹30. This approach does not consider future profits or market expectations and is more appropriate for companies with large tangible assets than high-growth companies.

When is Valuation Required?

Equity share valuation is needed in different financial scenarios to promote fair pricing and sound decision-making. For mergers, investments, financial reporting, or IPOs, precise valuation enables companies, investors, and regulators to determine the real value of a company. Some of the important scenarios where valuation is needed are discussed below.

- Mergers and Acquisitions: Determines a company’s fair value before a merger or acquisition. Assists firms in negotiating more favorable deals. Proper valuation guarantees that both sides receive a reasonable agreement. It also avoids monetary losses as a result of mispricing.

- Investment Choices: Share value is studied by investors before purchasing or selling shares. Helps decide whether a stock is undervalued or overvalued. Accurate valuation assists investors in getting the highest returns and minimizing risks. It also helps them choose the appropriate stocks for long-term growth.

- Financial Reporting and Compliance: Valuation of equity shares is required by companies for tax and accounting. Regulators need valuation reports for auditing. Accurate valuation preserves clear financial records. It confirms that companies abide by tax and legal standards correctly.

- Initial Public Offerings (IPOs): Assist in the appropriate price-setting of public offers. Guarantees just pricing for the investor. An effectively valued IPO induces more investors and more confidence in the market. Prevents the undervaluation or overvaluation of stocks.

- Valuation of Sweat Equity Shares: Sweat equity shares are issued by companies to employees at fair value. Assists in determining compensation based on services rendered. Proper valuation guarantees equitable rewards to employees. It also encourages skilled professionals to contribute towards business growth.

Relevance to ACCA Syllabus

Valuation of equity shares is addressed under Financial Management (FM) and Advanced Financial Management (AFM) under the ACCA syllabus. ACCA exam candidates need to know how to calculate the value of a firm’s shares using tools like the Dividend Discount Model (DDM), Price/Earnings Ratio (P/E), and Net Asset Value (NAV). These theories assist financial practitioners in making investment choices and evaluating business valuations.

Valuation of Equity Shares ACCA Questions

Q1: Which of the following valuation methods is based on the present value of future dividends?

A) Price/Earnings (P/E) Ratio

B) Dividend Discount Model (DDM)

C) Net Asset Value (NAV)

D) Gordon Growth Model

Ans: B) Dividend Discount Model (DDM)

Q2: What does the Price-to-Earnings (P/E) ratio measure?

A) The value of a company’s assets

B) The market price of a share relative to its earnings per share (EPS)

C) The total dividends paid by the company

D) The amount of retained earnings in a firm

Ans: B) The market price of a share relative to its earnings per share (EPS)

Q3: If a company has a high P/E ratio, what does it typically indicate?

A) The stock may be overvalued

B) The company is experiencing financial difficulties

C) Investors expect lower future growth

D) The company is undervalued

Ans: A) The stock may be overvalued

Q4: Which valuation method considers the liquidation value of a company’s assets?

A) Discounted Cash Flow (DCF)

B) Net Asset Value (NAV)

C) Dividend Discount Model (DDM)

D) Price-to-Sales Ratio

Ans: B) Net Asset Value (NAV)

Q5: A company’s stock has an expected dividend of $3 per share and a required return of 10%. Using the Gordon Growth Model with a dividend growth rate of 5%, what is the stock’s estimated value?

A) $30

B) $50

C) $60

D) $80

Ans: B) $50 (Value = 3 / (0.10 – 0.05))

Relevance to US CMA Syllabus

The US CMA syllabus under Corporate Finance and Investment Analysis deals with equity valuation. Candidates are taught to use valuation models to evaluate a company’s financial health and investment worth. Calculating and interpreting the value of stocks is important for financial managers when making capital investment decisions.

Valuation of Equity Shares US CMA Questions

Q1: What is the primary goal of equity valuation?

A) To determine the book value of assets

B) To assess the fair value of a company’s shares

C) To calculate net profit margin

D) To evaluate debt financing options

Ans: B) To assess the fair value of a company’s shares

Q2: Which method of equity valuation discounts future expected cash flows?

A) Net Asset Value (NAV)

B) Price-to-Earnings (P/E) Ratio

C) Discounted Cash Flow (DCF) Model

D) Dividend Yield

Ans: C) Discounted Cash Flow (DCF) Model

Q3: The dividend yield of a stock is calculated as:

A) Dividend per share / Earnings per share

B) Dividend per share / Market price per share

C) Market price per share / Book value per share

D) Earnings per share / Dividend per share

Ans: B) Dividend per share / Market price per share

Q4: A company has a market capitalization of $100 million and annual earnings of $10 million. What is its P/E ratio?

A) 5

B) 10

C) 15

D) 20

Ans: B) 10 (P/E = Market Capitalization / Earnings = 100M / 10M)

Q5: If a company consistently increases its dividends, what impact does it have on its share valuation?

A) Share price may increase

B) P/E ratio will decrease

C) Net asset value will be negative

D) Discounted Cash Flow value will decrease

Ans: A) Share price may increase

Relevance to US CPA Syllabus

The US CPA exam syllabus covers equity valuation in financial accounting and reporting (FAR) and business environment and concepts (BEC). CPA aspirants are examined over valuation techniques, financial statement analysis, and the influence of market trends on the share price. Understanding equity valuation is pivotal for auditing, taxation, and advisory purposes.

Valuation of Equity Shares US CPA Questions

Q1: What does the Discounted Cash Flow (DCF) model primarily rely on?

A) Book value of assets

B) Present value of future free cash flows

C) Current liabilities of the company

D) Past earnings reports

Ans: B) Present value of future free cash flows

Q2: If a stock has a high dividend yield, what does it suggest?

A) The company has a low dividend payout ratio

B) The company’s stock price is relatively low compared to its dividends

C) Investors expect rapid growth

D) The stock is always a good investment

Ans: B) The company’s stock price is relatively low compared to its dividends

Q3: What is a limitation of the Net Asset Value (NAV) method in equity valuation?

A) It ignores intangible assets and future earnings potential

B) It includes all future expected cash flows

C) It considers only dividend-paying companies

D) It does not account for market conditions

Ans: A) It ignores intangible assets and future earnings potential

Q4: Which financial ratio is commonly used to determine if a stock is overvalued or undervalued?

A) Current Ratio

B) Price/Earnings (P/E) Ratio

C) Debt-to-Equity Ratio

D) Return on Assets (ROA)

Ans: B) Price/Earnings (P/E) Ratio

Q5: What does a high P/E ratio typically indicate about investor expectations?

A) Investors expect high future growth

B) The company is experiencing a financial decline

C) The stock price is falling

D) Investors expect lower future dividends

Ans: A) Investors expect high future growth

Relevance to CFA Syllabus

The CFA syllabus provides detailed coverage of the valuation of equity shares in Financial Analysis and Equity Investments. The CFA candidates must comprehend diverse valuation methods, including Discounted Cash Flow (DCF), Price Multiples, and Market-based Valuation Techniques. Investment analysis, portfolio management, and equity research all rely heavily on these valuation methods.

Valuation of Equity Shares CFA Questions

Q1: What is the primary assumption behind the Gordon Growth Model (GGM)?

A) Dividends grow at a constant rate

B) Interest rates remain constant

C) Stock prices are always efficient

D) Earnings per share remain unchanged

Ans: A) Dividends grow at a constant rate

Q2: The Enterprise Value (EV) of a company is calculated as:

A) Market Cap + Total Debt – Cash

B) Net Income – Depreciation

C) Total Assets – Total Liabilities

D) Price-to-Book Ratio × Earnings per Share

Ans: A) Market Cap + Total Debt – Cash

Q3: What does the PEG ratio measure?

A) Price-to-Earnings (P/E) ratio adjusted for growth

B) Debt-to-Equity ratio

C) Dividend per share divided by market price

D) Return on total assets

Ans: A) Price-to-Earnings (P/E) ratio adjusted for growth

Q4: If a company’s stock is undervalued according to fundamental analysis, what should an investor do?

A) Short-sell the stock

B) Buy the stock

C) Ignore the stock

D) Wait for a stock split

Ans: B) Buy the stock

Q5: What is the intrinsic value of a stock?

A) The stock’s actual fair value based on fundamental analysis

B) The price set by market demand

C) The total dividends paid over time

D) The face value of the stock

Ans: A) The stock’s actual fair value based on fundamental analysis