Preference share valuation should interest both investors and the companies involved. The shares have a fixed return on dividends, unlike equity shares. The values give investors an overview of the worth of the investment before a decision is made, such that preference share valuations might include dividends, redemption rights, and market conditions.

Therefore, different methods are being applied to assess the value of preference shares by investors; these involve the dividend discount model for preference shares, the book value approach for preference shares, and market-based approaches. Still, variables like interest rates, profitability, and company policies could affect any methodologies involved in preference share valuation.

Valuation of Preference Share

Different financial approaches are used to rate preference shares. These shares, unlike equity shares, promise a fixed income. Thus, the valuation of these shares will depend on dividends, redemption, and market conditions. Although theoretically similar, investors’ and companies‘ techniques to evaluate preference shares always yield different results.

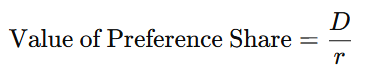

1. The Dividend Discount Model

It values future estimated dividends based on their present value. It is the most widely used valuation. Technique Since it applies to preference shares because of the fixed dividends it pays, preference share value would, therefore, be established through this model as:

Where:

- D = Fixed Dividend

- r = Required Rate of Return

For example, if a preference share offers a dividend of ₹10 and the required rate of return is 5%, the value is:

10 /0.05 =200

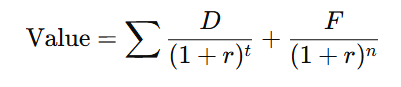

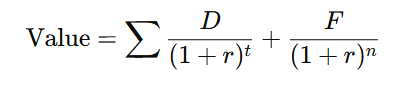

2. Redeemable Preference Shares Valuation

Redeemable preference shares have a fixed maturity date. The valuation considers both the periodic dividend and the redemption price. The formula is:

Where:

- D = Annual Dividend

- r = Discount Rate

- F = Face Value

- n = Number of Years

For example, suppose a preference share offers ₹10 annual dividend, a face value of ₹100, a discount rate of 6%, and a maturity of 5 years. In that case, the valuation will consider discounted cash flows over five years.

3. Perpetual Preference Shares Valuation

Perpetual preference shares do not have a maturity date. These methods allow insights regarding distinguishing references to the standard pricing for preference shares. They provide dividends forever. The formula is:

For instance, if a perpetual preference share pays ₹ eight annually and the required return is 4%, its valuation is:

8/0.04=200

Factors Influencing Valuation of Preference Shares

Various factors influence preference share prices in the market. These factors help investors to realise a fair valuation for preference shares concerning the investee.

1. Rates of Interest

Interest rates have turned out to be one of the chief determinants in determining the value of preference shares. Hence, with regard to their falling through sky-high doors, preference shares could be included in that number of all fixed dividend instruments where the current going away falls as interest rates go up. In fact, preference shares would become very attractive when interest rates are at a low level.

2. Issuer Profitability

Another factor that affects the price or value of timeshare shares is the financial condition of the company. If the companies suffer short-term low-profit generation, high yield will be demanded, and hence the price of the preference shares would fall.

3. Dividend Declaration Policy

The market generally expects the payment of dividends for preference shares, even if deferred. Regular dividend payment on preference shares boosts the calculations of yields and thus increases such shares’ value.

4. Economic Climate

The investor’s risk appetite may vary with changes in economic conditions. Generally, preference shares will preserve their value under normal market conditions. Uncertainty creeps in only during disruptions, and their value starts to plummet.

5. Terms of Redemption and Liquidity

The critical aspect influencing the valuation of redeemable preference shares is the redemption period and the value. Shares with fixed and clear redemption terms will be regarded as best. Liquidity would seriously impact the intrinsic value: should a redeemable preference share be considered non-liquid, its price will crash.

Interest should also focus on the above points, showing the causes for treating preference shares differently than equity shares in market valuations.

Formula for Preference Share Valuation

Investors must correlate their calculations with important formulae to find the book value of preference shares.

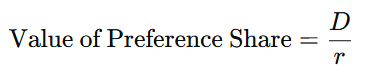

1. Fixed-Dividend Preference Shares Formula

In the case of fixed-dividend preference shares, the intrinsic value of preference shares formula is:

For example, if a company issues preference shares with a ₹15 dividend and the market expects a 7% return, the value is:

15/0.07=214.286

2. Formula for Redeemable Preference Shares

For redeemable preference shares, the valuation formula is:

For instance, if the company redeems the shares in 5 years at ₹100 with a 6% discount rate and pays ₹10 annually, the valuation follows discounted cash flow calculations.

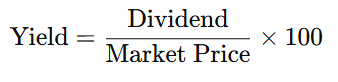

3. Preference Share Yield Calculation

Investors use yield calculations to measure returns. The formula is:

If a preference share pays a ₹12 dividend and trades at ₹240, the yield is:

( 12/240) X 100 = 5

These formulas help determine the fair value of preference shares.

Preference Shares vs Equity Shares

Preference shares differ from equity shares in terms of returns, risk, and valuation.

| Aspect | Preference Shares | Equity Shares |

| Dividends | Fixed dividend | Variable dividend |

| Voting Rights | No voting rights | Voting rights |

| Risk | Lower risk | Higher risk |

| Valuation Method | Based on fixed dividends | Market-driven valuation |

Equity shares have market-driven prices, whereas preference shares depend on dividend payments and risk.

Investment in Preference Shares

Investing in preference shares can be beneficial. It provides fixed income and is less risky than equity. However, investors must assess:

- Fixed Returns: Preference shares offer stable income.

- Risk: Lower than equity but still subject to company performance.

- Liquidity: Some preference shares may be less liquid.

Perpetual preference shares valuation suggests that these shares are suitable for long-term stable returns. Investors should analyse the preference share cost of capital before making decisions.

Relevance to ACCA Syllabus

Valuation of preference shares is essential in ACCA, especially in financial management (FM) and advanced financial management (AFM). This area deals with investment appraisal, capital structure, and cost of capital; understanding preference share valuation thus helps ACCA students distinguish between different financing sources, analyse their respective impacts on company valuation, and ultimately make some huge strategic financial decisions by IFRS.

Valuation of Preference Shares ACCA Questions

Q1: Which formula calculates the value of irredeemable preference shares?

A) Dividend / Market Price per Share

B) Dividend / Required Rate of Return

C) Dividend / (Market Price per Share – Growth Rate)

D) Dividend / Net Income

Ans: B) Dividend / Required Rate of Return

Q2: Preference shares are classified as what under IFRS when they have a mandatory redemption date.

A) Equity

B) Non-current Asset

C) Liability

D) Contingent Liability

Ans: C) Liability

Q3: What is a key disadvantage of issuing preference shares for a company?

A) They dilute the voting rights of ordinary shareholders

B) They increase financial leverage

C) They result in higher taxes

D) They cannot be repurchased

Ans: B) They increase financial leverage

Q4: How does an increase in the required rate of return impact the valuation of preference shares?

A) The value remains constant

B) The value decreases

C) The value increases

D) The value is unaffected if dividends remain the same

Ans: B) The value decreases

Q5: Which discounting technique is commonly used when valuing redeemable preference shares?

A) Net Present Value (NPV)

B) Payback Period

C) Future Value Formula

D) Accounting Rate of Return

Ans: A) Net Present Value (NPV)

Relevance to CMA Syllabus

The valuation of preference shares is a key topic in the US CMA syllabus under Part 2: Financial Decision Making. The CMA curriculum focuses on cost of capital, investment valuation, and financial statement analysis. A deep understanding of preference share valuation helps CMAs assess financing alternatives and determine their impact on the firm’s economic performance.

Valuation of Preference Shares CMA Questions

Q1: How do preference dividends affect common shareholders’ earnings per share (EPS) calculation?

A) They are deducted from net income

B) They are added to net income

C) They do not affect EPS calculation

D) They are reported as an expense

Ans: A) They are deducted from net income

Q2: Which of the following is a characteristic of cumulative preference shares?

A) Dividends accumulate if not paid

B) Shareholders have voting rights

C) They have a fixed maturity date

D) They are always convertible into common shares

Ans: A) Dividends accumulate if not paid

Q3: What happens to the valuation of preference shares if market interest rates increase?

A) The value of preference shares increases

B) The value of preference shares decreases

C) The value remains unchanged

D) The dividend yield decreases

Ans: B) The value of preference shares decreases

Q4: A company issues preference shares with a 6% annual dividend. If the required rate of return is 8%, what is the valuation of a single share with a $100 par value?

A) $75

B) $80

C) $100

D) $120

Ans: B) $80 (Calculated as $6 / 0.08)

Q5: Which type of preference share allows holders to participate in additional earnings after common shareholders receive a specified dividend?

A) Convertible preference shares

B) Participating preference shares

C) Redeemable preference shares

D) Cumulative preference shares

Ans: B) Participating preference shares

Relevance to the CPA Syllabus

The valuation of preference shares is crucial in the US CPA exam, particularly under the Financial Accounting and Reporting (FAR) section. By GAAP standards, CPAs must understand how preference shares impact financial statements, including balance sheets and earnings calculations.

Valuation of Preference Shares CPA Questions

Q1: How are preference dividends reported in financial statements under US GAAP?

A) As a liability until paid

B) As an operating expense

C) As a deduction from retained earnings

D) As part of net income

Ans: C) As a deduction from retained earnings

Q2: How is the cost of preference shares included when calculating the weighted average cost of capital (WACC)?

A) Market price of preference shares

B) Dividend yield of preference shares

C) After-tax cost of preference shares

D) Pre-tax cost of preference shares

Ans: C) After-tax cost of preference shares

Q3: Which characteristic of redeemable preference shares makes them similar to debt?

A) They pay variable dividends

B) They must be repaid at a future date

C) They offer voting rights

D) They can be converted into common stock

Ans: B) They must be repaid at a future date

Q4: Which of the following factors affects the valuation of preference shares?

A) The company’s net income

B) The dividend payout ratio of common shares

C) The required rate of return

D) The company’s capital expenditure

Ans: C) The required rate of return

Q5: A company issues 10% preference shares at $50 each. If the required rate of return is 12%, what is the fair valuation per share?

A) $40

B) $41.67

C) $50

D) $60

Ans: B) $41.67 (Calculated as $5 / 0.12)

Relevance to CFA Syllabus

The CFA curriculum in Corporate Finance and Equity Investments covers preference shares’ valuation. CFA candidates must analyse preference shares as part of a company’s capital structure, determine their impact on investment risk, and use valuation models to assess their fair value in market conditions.

Valuation of Preference Shares CFA Questions

Q1: How do preference shares impact a firm’s capital structure?

A) They are considered short-term liabilities

B) They reduce overall financial risk

C) They provide fixed-income financing without increasing debt

D) They are always classified as equity

Ans: C) They provide fixed-income financing without increasing debt

Q2: If a company issues preference shares with a fixed dividend, which valuation approach is most appropriate?

A) Dividend Discount Model (DDM)

B) Free Cash Flow Model

C) Market Capitalization Model

D) Capital Asset Pricing Model (CAPM)

Ans: A) Dividend Discount Model (DDM)

Q3: What effect does a decrease in the required rate of return have on the value of preference shares?

A) Increases the value

B) Decreases the value

C) Has no effect

D) Reduces dividend payments

Ans: A) Increases the value

Q4: Which factor is least relevant when valuing preference shares?

A) Dividend rate

B) Market interest rates

C) Common stock volatility

D) Required rate of return

Ans: C) Common stock volatility

Q5: What type of preference shares can be exchanged for common shares at a predetermined ratio?

A) Callable preference shares

B) Participating preference shares

C) Convertible preference shares

D) Redeemable preference shares

Ans: C) Convertible preference shares