When you buy life insurance, you’re making a deal with an insurance company. You agree to pay them regularly, and they promise to give your family a chunk of money if you pass away. This way, your loved ones won’t have to worry about things like the mortgage, school fees, or everyday expenses without you around. It’s all about making sure your family is financially set, giving you peace of mind knowing they’ll be okay.

What Is Life Insurance?

Life insurance acts as a crucial financial tool, giving financial security and stability to an individual’s dependents if they pass away unexpectedly. Essentially, it serves as a way to manage risk by shifting the financial burden from the person holding the policy to the insurance company.

- Death Benefit:

- A predetermined amount paid to the beneficiaries upon the policyholder’s death.

- Premium Payment:

- Regular payments made by the policyholder to keep the policy active.

- Policy Term:

- The duration for which the life insurance coverage is active.

- Maturity Benefit (for certain policies):

- A lump sum paid to the policyholder if they outlive the policy term.

Why Life Insurance Matters?

- Provides financial security to dependents.

- Covers debts, loans, and other financial obligations.

- Ensures peace of mind, knowing that loved ones are protected.

Understanding what is life insurance is the first step toward making informed decisions about securing your family’s future.

Types of Life Insurance

Various life insurance policies cater to different financial needs, like securing your family, building wealth, and hitting long-term goals. You’ve got term insurance if you’re looking for low-cost coverage, whole life insurance when you want protection for your entire life, endowment plans to save up some money, and ULIPs if you’re aiming for growth linked to investments. This way, there’s a tailored solution for every life stage.

Term Life Insurance

- Offers coverage for a specific term, such as 10, 20, or 30 years.

- Provides a death benefit but no maturity benefit.

- Example: A 20-year term policy with a $500,000 death benefit.

Whole Life Insurance

- Provides lifetime coverage with a death benefit and cash value component.

- Premiums are higher than term insurance but remain constant throughout the policy.

Endowment Plans

- Combines life coverage with savings.

- Pays a lump sum at the end of the policy term or upon the policyholder’s death.

Unit Linked Insurance Plans (ULIPs)

- Combines life insurance with investment.

- Premiums are invested in equity or debt funds, offering returns along with life coverage.

Child Plans

- Secures the financial future of children by covering education and other expenses.

- Provides payouts at significant milestones in the child’s life.

Pension Plans

- Provides a regular income post-retirement while offering life coverage.

- Example: Annuity plans ensuring income after retirement.

These types of life insurance policies cater to different financial goals, making it essential to choose one that aligns with individual needs.

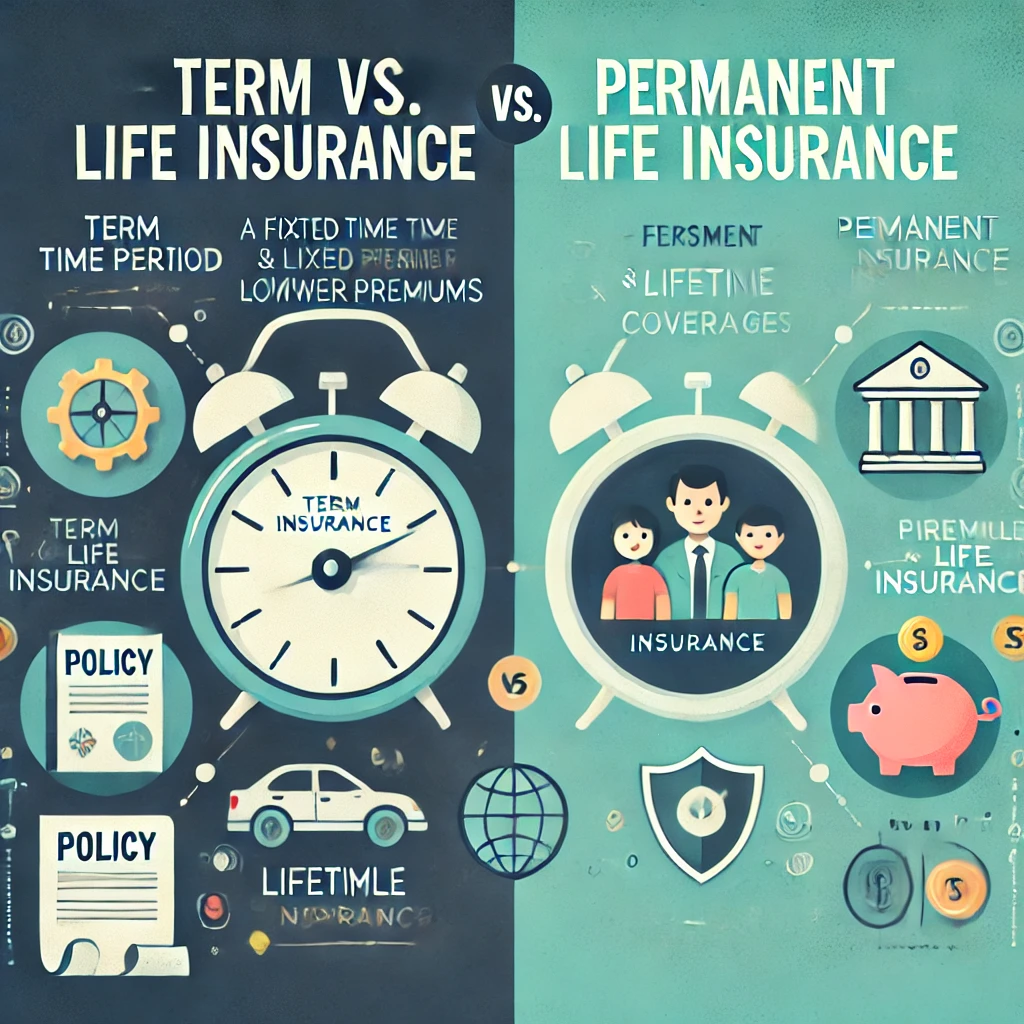

Term vs. Permanent Life Insurance

You need to get the hang of what makes term life insurance different from permanent life insurance. With term insurance, you’re looking at coverage for a set period at super affordable rates, but it doesn’t build cash value. It’s perfect if you’re covering short-term needs. On the other hand, permanent insurance sticks with you for life, comes with savings and growth potential, and is a solid choice for long-term financial goals and wealth accumulation.

Term Life Insurance

- Coverage for a specific term.

- No cash value component; pays only the death benefit.

- Lower premiums compared to permanent policies.

- Ideal for temporary needs, such as covering a mortgage or education expenses.

Permanent Life Insurance

- Provides lifetime coverage.

- Includes a cash value component that grows over time.

- Higher premiums due to added benefits.

- Suitable for long-term needs, such as estate planning or wealth transfer.

| Feature | Term Life Insurance | Permanent Life Insurance |

| Coverage Duration | Specific term (10, 20 years) | Lifetime |

| Cash Value | None | Builds over time |

| Premium Cost | Lower | Higher |

| Ideal For | Short-term financial needs | Long-term financial security |

Understanding the differences between term vs. permanent life insurance helps in choosing the right policy for your needs.

What Affects Your Life Insurance Premiums and Costs?

Your age, health, and lifestyle habits, along with your financial goals and the amount you want covered, play a big role in setting your life insurance premiums. The kind of plan you pick, how long it covers you, and any extra features like riders also affect the price. So, it’s really important to make smart choices based on what you need.

Age

- Younger applicants pay lower premiums as the risk of death is lower.

- Example: A 25-year-old may pay $20/month, while a 50-year-old pays $100/month for the same coverage.

Health

- Pre-existing conditions and lifestyle habits, such as smoking, increase premiums.

- Example: Smokers often pay 20-30% higher premiums.

Policy Type

- Term insurance has lower premiums, while permanent policies cost more due to cash value benefits.

Coverage Amount

- Higher death benefits result in higher premiums.

- Example: A $1 million policy costs more than a $500,000 policy.

Occupation and Hobbies

- Risky jobs or hobbies, like aviation or scuba diving, increase premiums.

Gender

- Women typically pay lower premiums as they have longer life expectancies.

Understanding these factors lets you better estimate and manage life insurance premiums and costs. It’s a crucial financial tool that secures your loved ones’ stability and security if something happens to you. Getting the hang of the different types of life insurance, comparing term versus permanent policies, and digging into what affects your premiums can guide you in making a smart choice to protect your family’s future. Whether you’re looking to pay off debts, fund education, or set up for retirement, life insurance offers unbeatable peace of mind and financial security.

What do you mean by Life Insurance? FAQs

What is life insurance?

Life insurance is a contract where the insurer pays a lump sum to beneficiaries upon the policyholder’s death, in exchange for premiums.

What are the types of life insurance?

Types include term insurance, whole life insurance, endowment plans, ULIPs, child plans, and pension plans.

How does age affect life insurance premiums?

Younger individuals pay lower premiums as the risk of death is minimal compared to older applicants.

What is the difference between term and permanent life insurance?

Term insurance provides temporary coverage with no cash value, while permanent insurance offers lifetime coverage with a cash value component.

Can life insurance be used as an investment?

Yes, policies like ULIPs and endowment plans combine life coverage with investment options, offering returns along with protection.