Auditing is being done to ascertain that the transactions find actual reflections within the recorded books of accounts and that all misrepresentation disappears. Auditing itself is one of the significant audit procedures of such a process. There are numerous inquiries from professionals like, what is analytical procedure in audit, as investigations include students interested in acquiring auditing knowledge. Analytical procedures mean evaluating financial information drawn from the relationship of data and identifying unusual trends or inconsistencies. The procedures are directed towards the efficient examination of economic data, hence providing a finger on the pulse so auditors can discover possible errors or fraud. With the skills to focus on high-risk areas, analytical procedures add value to audit information.

What is Analytical Procedures in Audit?

Analytical procedures in auditing refer to methods auditors employ to analyze financial data by finding relationships and patterns and identifying anomalies in the process. This is a procedure that auditors use to analyze financial statements concerning reality and accuracy. The analytical methods are meant to identify misstatements, fraud, or errors in the financial records. It facilitates risk assessment, decision-making, and validation of the financial statements.

Typically, comparative financial data with records, budgets, or even general industry standards represent the building blocks of analytical procedures. Because of the analytical procedures, the unusual fluctuations can easily be spotted, making it easy for auditors to start probing them highly. The auditor uses these at different stages of an audit, including planning, execution, and review.

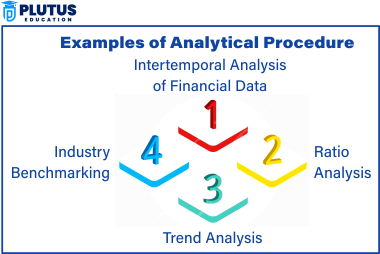

Examples of Analytical Procedure

Analytical procedures are essential in the audit; they enable auditors to analyze financial data while watching divergences. Several examples of analytical auditing procedures illustrate how auditors use these techniques.

Intertemporal Analysis of Financial Data

Auditors look at the last years of financial data compared to those provided in the current year’s financial statements. If they find a significant increase or reduction in revenue, expenses, or profit, they will investigate why that occurred. For example, if sales for that entity increased by 50% and the cost river remained unchanged, auditors would find themselves looking at how the entity recognized that revenue.

Ratio Analysis

Ratio analysis is one more common analytical procedure in audits. Auditors use financial ratios like

- Liquidity ratios (Current Ratio, Quick Ratio)

- Profitability ratios (Gross Profit Margin, Net Profit Margin)

- Efficiency ratios (Inventory Turnover, Accounts Receivable Turnover)

- Leverage ratios (Debt-to-Equity Ratio, Interest Coverage Ratio)

For instance, if a company has a debt-to-equity ratio higher than the industry average, then auditors may question whether the company is experiencing some financial turmoil.

Trend Analysis

Auditors keep an eye on trends in financial statements to spot atypical variances. Whenever expenses remain stable over the years and suddenly go through a very high leap, the auditors will look into what caused such an increase. Trend analysis is also helpful in identifying the effects of seasonality, market conditions, and operational changes.

Industry Benchmarking

Auditors compare a company’s financial performance with industry benchmarks. Auditors will investigate what happens if a company’s profit margin is significantly lower than competitor companies. Industry benchmarking assists in knowing if a company’s performance aligns with industry standards.

Types of Analytical Procedures in Auditing

There are different types of analytical procedures that auditors use in auditing to analyze a financial statement effectively. These will determine if an auditor will perform a risk investigation, detect fraud, or determine the correctness of financial statements.

Trend Analysis

Trend analysis involves comparing financials at different points in time to discover patterns or aberrations in a firm. The auditees would establish trends regarding the revenue, expenses, and profits maintained or maintained for the duration. Any significant aberration would be traced further.

Ratio Analysis

Ratio analysis enables the auditors to examine the segment’s financial viability. The auditors work out liquidity and solvency ratio, profitability, and efficiency ratios, which are three kinds of financial ratios that help spot financial and business risk and operational efficiency.

Reasonableness Testing

Reasonableness testing relates financial data with the expected outcome. The auditors will then check for consistency with the firm’s operational expenses versus the performance. For example, if there are increased sales figures and constant operating expenses, the auditors will investigate the reasonableness of that sales amount.

Interrelationships of Data

Auditors investigate the relationships for discrepancies. Costs usually incurred for production will increase in the value of inventories.

The Analytical Procedures Process in an Audit

Various steps in analytical auditing help auditors to evaluate financial statements. It finds misstatements and risks and assures the auditor that the financial statements are prepared on a reliable basis.

Step 1: Planning Analytical Procedures

The analytical procedure used to the nature of the audit to be conducted by the auditors will constitute the planning of any audit work to reduce audit risk. Auditors identify, among others, financial information to be analyzed and how these analyses will be performed. The planning will focus on high-risk areas, efficiently using the audit resources.

Step 2: Collection of Financial Data

The auditors gather financial data from all sources, such as balance sheets, income statements, and cash flow statements. Besides these financial statements, they also procure industry benchmarks, historical data, and data based on budgets to compare with the monetary items.

Step 3: Application of Analytical Procedures

In an analytical review, the auditors may perform trend analysis, ratio analysis, and/or reasonableness testing in evaluating financial data. The auditors compare historical records of financial statements against industry benchmarks to pinpoint divergence.

Step 4: Investigating Unusual Variations

If the auditors suspect the financial data of any unusual swing, they will go ahead and find out the reasons that may cause such variations. Investigations can either include looking for errors or fraud or determining if material misstatements undermine the integrity of the financial statement.

Step 5: Findings and Conclusions

The results obtained by the auditors are presented in an audit report, along with recommendations to rectify such errors or misstatements. In addition, they shall record their findings and suggest corrective measures intending to enhance the reliability of financial information.

What is Analytical Procedure in Audit FAQs

1. What is meant by analytical procedures in planning an audit?

Analytical procedures in audit planning should indicate risk areas and misstatement detection and assess financial performance. These procedures include trend analysis, ratio analysis, and industry benchmarking, which help auditors’ audit planning approach.

2. Why are analytical procedures useful in auditing?

Analytical procedures help auditors sniff out errors, fraud, and financial misstatements. They also highlight the high-risk areas and allow auditors to see the efficiencies in their audit work.

3. Differentiate analytical procedure from substantive testing.

Analytical procedures pertain to evaluating financial data for trends and anomalies, while substantive testing requires in-depth inspection of records and transactions for disciplining them.

4. How do auditors use analytical procedures?

Auditors compare financial data with past data, industry benchmarks, and expected results when using analytical procedures. They use trend analysis, ratio analysis, and reasonableness testing to locate inconsistencies.

5. Are analytical procedures useful in detecting fraud?

Yes, analytical procedures aid auditors in identifying fraud by throwing up red flags for aberrant trends and discrepancies in the financial statements; if they find unusual fluctuations, an investigation ensues to establish whether fraud is involved.