A well-organized inventory is essential for any business’s operations. The ABC analysis of inventory management is one of the best tools for stock classification and control based on value. Businesses categorise their inventory items into three groups according to importance: A, B, and C. This way, high-value items get more attention than low-value items, which deserve much less attention.

Such a method aids businesses in optimising resources, saving on inventory costs, and enhancing inventory control. A thorough guide such as this will look into ABC classification in inventory management, how it works, the steps involved in implementation, practical examples, advantages, and best practices.

ABC Classification in Inventory Management

ABC classification in inventory management is established on the scientific principle of the 80-20 rule weighing, that 80% of the results come through 20% of the causes. In simple language, a small part contributes to a bulk in inventory, generating revenue and vice-versa.

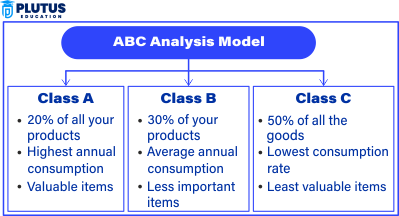

Three categories fall under the division of inventory for any business:

Category A

High-value items that have low sales volume. These require stringent monitoring, with forecasting being of high accuracy. Since they contribute most to the revenue, firms must ensure their availability, taking care not to be overstocked simultaneously. Frequent stock checks and demand forecasting help businesses maintain the right balance.

Category B

Moderate-value items that have medium sales volume. These require moderate control and tracking. These items are essential but need not be monitored as closely as Category A. Thus, businesses need to optimise stock levels to ensure availability while at the same time preventing unnecessary storage costs.

Category C

Low-value items that generate high sales. They are always given less oversight and stocked in bulk. These items have a much lower profit margin. Hence, companies must minimise the costs of ordering and holding the items. These items can be efficiently managed by bulk purchasing and automatic replenishment.

This classification helps businesses to utilise resources optimally. High-value items are to be checked frequently, while low-value items require less effort regarding management. Therefore, with the ABC classification, companies can focus more on these two categories to manage inventory effectively.

Why Is ABC Classification Important?

Without such classification, a business may waste front-end resources on low-value items while ignoring crucial ones substantially high in value. This creates situations where cash is blocked, storage becomes unqualified, and essential products are left to stay out of storage. In the proper classification procedures, the spotlight is on the right choice of items, which means savings in some avoidable expenses and adequate fulfilment.

ABC Inventory Control Method

The ABC inventory control has been designed to help an organisation or firm maintain its inventory by the most prized articles for each firm. Implementing this method will require a slice of its organisation and inventory management.

Processing Steps

Step 1: Collecting Inventory Data

A data collection process should first be made for all items in the inventory, specifying the pricing per purchase, frequency of demand, and total cost incurred annually. This data will identify the products that generate the most revenue for the business, and the misallocation of resources resulting from inaccuracies in this data would lead to a misclassification of the inventory. Additionally, continuous updating of essential data maintains the storage appropriately categorised with every change.

Step 2: The Annual Consumption Value Must be Calculated

To get the correct classification for their items, businesses must calculate Annual Consumption Value (ACV) by the given formula:

ACV = (Annual Demand) × (Unit Price)

This particular value indicates the level of importance of every product: how much it contributes to revenue. Products with an ACV that exceeds certain value levels are called Category A. Lower ACV levels place products into Categories B and C. The result is a calculation allowing businesses to make decisions based on data on which inventories are strictly monitored and which may be looser.

Step 3: Rank Items from the Highest ACV down to the Lowest

Once the computation for ACV is accomplished, the inventory will be ranked for each unit from the highest to the lowest based on the value. The highest ones will all be grouped into Category A, while the lowest ones will fall under Category C. It will help companies get a clear picture of the product requiring most of their management attention. The misdirected focus will also end up being inefficient in stock management, leading to stock shortages or stock excessiveness.

Step 4: Set Category Percentage

Typically, these categories are distributed:

| Category | Percentage of Items | Percentage of Value |

| A | 10-20% | 70-80% |

| B | 30-40% | 15-25% |

| C | 50-60% | 5-10% |

The situation here is that the percentages differ from business type to business type or industry to industry. Adjusting these percentages per real-time sales and demand allows the business to manage the inventory level and avoid putting money in unwanted inventories.

Step 5: Inventory Management Policy Implementation

- Category A: Items in this category require tight stock control, regular reordering, and more accurate demand forecasting. The stocking should be so stringent that there should be no excess stock. A slight non-availability of category A items can disturb sales and thus affect revenues.

- Category B: With moderate inventory control, the focus lies between costs and availability of Category B items. These items are more popularly demanded but are less profitable than Category A; thus, the company should conduct inventory review cycles to readjust based on stock level trends.

- Category C: Large quantities can be bought, and little control can be exercised to save on management costs. Such recordings can be kept in large quantities to prevent frequent re-ordering and reduce operational costs. Companies must, however, ensure the inventory level does not exceed the required amount to avoid either wastage or obsolescence.

This systematic approach ensures that resources are effectively channelled so that any expenditure that could have been foregone is consigned.

Example of Practical Applications of ABC Inventory Analysis

An example considered under practical applications is the ABC analysis, which refers to how organisations can use this method to improve their functioning.

ABC analysis can be described by taking the example of a retail store. Suppose it is an electronic store selling accessories and small gadgets. The ABC classification method is used for inventory classification.

- Category A: Laptops and smartphones – Very high value and low sale. This tightly controlled commodity requires constant monitoring of the demand. Excess inventory would mean tying up capital. Therefore, these items are kept in stock just in time.

- Category B: The average values and frequency of sales are headphones and power banks—the store’s career rings to ensure product availability. The demand for these products is relatively steady, so keeping a medium stock level would assure revenue but not with too high a storage cost.

- Category C: These are low-cost items with a high sales volume, such as phone cases and charging cables stocked in bulk with little monitoring. Automatic systems ensure timely supply as demand does not vary.

Example of ABC Analysis in Manufacturing

Raw materials in the manufacturing sphere are categorised based on the two parameters of cost and usage:

- Category A: The expensive materials include, say, microchips, receiving strict monitoring. These materials significantly impact production costs, making businesses rely on rigorous order and inventory tracking mechanisms to avoid expenses that are not useful.

- Category B: Moderate-cost materials (like plastic casings) need reasonable control. This material is deemed critical but not expensive enough as an A item. A company would ensure enough stock of these items to keep production running without overstocking.

- Category C: Low-cost materials (like screws) are in bulk and with negligible tracking. These items are cheap and heavily used, so businesses order them in bulk to reduce appending reorders and production delays.

In addition to maximising profitability, it helps firms control inventory effectively and minimise wastage.

Benefits of ABC Analysis in Inventory Management

After all, the benefits of ABC analysis in better inventory management keep the practice well applied in several areas.

Resource Allocation

It is more like ABC Analysis plunges into effective resource allocation in the business. High-value items will need more attention than low-value items, thus giving them a somewhat low priority compared with the others. As a result, this method prevents unnecessary cost burdens caused by poor stock.

Improved Inventory Control

With categories established correctly, overstocking and stockout rates are reduced. Category A is constantly watched to ensure that stockouts do not occur and sales are never compromised.

Cash Flow Optimization

By concentrating on high-value inventory, business cash flow is optimised. The firm puts more money on its well-selling items and cuts expenditure for lower-hanging stocks.

Better Decision-Making

ABC analysis gives direct examples of stock-related trends. Companies can make better decisions concerning ordering, stocking, and frequency of orders.

Reduction in Storage Charges

Minimizing excess stock of lower-value items enables the business to cut storage costs. Therefore, warehouse space is freed for more urgent products. These benefits have helped improve the efficiency and profits of organizations while keeping a balanced tone for all their inventories.

ABC Analysis in Inventory Managemnt FAQs

1. What is ABC analysis in inventory management?

ABC analysis in inventory management is a method for categorizing the inventory into three groups, B, and based on their value. Category A consists of high-value items, category B includes moderately valuable items, and category C contains low-value items. By categorizing their resources, organizations will prioritize the resources most necessary for their efficient reorder of stock.

2. How does the Reorderingfication in inventory management increase efficiency?

ABC classification in inventory management increases efficiency by ensuring businesses focus on high-value items that contribute considerably to reordering. It avoids the overstaying of low-value items and increases the optimization of resource distribution.

3. Can the ABC inventory control method be applied to all industries?

The ABC inventory control method can be applied to retail, manufacturing, hospital, and e-commerce industries. Any business that manages inventory can use this model of classification.

4. An example of ABC inventory analysis in the pharmaceutical industry?

In the pharmaceutical industry, Category A includes expensive, life-saving drugs; Category B consists of commonly used medicines; and Category C includes generic, over-the-counter medications.

5. How does the ABC inventory management system reduce costs?

The ABC inventory management system reduces costs by constraining low-value items’ excess stock to save storage costs. Fast-moving, high-value items are kept for sale even while managing appropriate inventory levels.