Control techniques are one of the most crucial tools and methods that managers use to monitor, measure, and adjust activities within an organization. The performance can thus be assured to act in conjunction with planned objectives and help businesses gain efficiency and attain success by using the control techniques. Deviations are noted, risks can be minimized, and corrective action can be taken by using control techniques to get back on track. From traditional budgeting to modern data analytics, these are at the core of managing the organization successfully.

What are Control Techniques?

Control techniques are systematic approaches applied by an organization to govern activities, evaluate performance, and check for conformance to the established objectives. Techniques are therefore the checkpoint to help businesses follow the progress in a particular process and make changes when necessary.

Every organization needs to have controls in place to execute its plan well. Control techniques fulfill this requirement by providing a structured framework to monitor activities and address deviations quickly. Whether it is evaluating financial performance or improving quality, control techniques play an important role in organizational success.

In control techniques, managers set standards, measure the performance, and compare with the standards. Then, they identify gaps and implement corrective action to bridge those gaps. For instance, if the sales figures bring out something that falls below the expectations of that sales figure then the managers will analyze the cause, adjust their strategies, and reallocate the resources. Thus, performance always stays within goals.

Process of Control Techniques

The process of control techniques involves setting clear standards, measuring actual performance, and comparing it with benchmarks. Managers then take corrective actions to address deviations and improve outcomes.

| Process of Control Techniques | Explanation |

| Set Standards | Define clear, measurable goals for performance. |

| Measure Performance | Regularly track actual results against benchmarks. |

| Identify Deviations | Detect areas where performance lags behind expectations. |

| Take Corrective Action | Implement solutions to address gaps and improve results. |

This structured approach ensures that all organizational functions contribute to achieving overall objectives effectively.

Traditional and Modern Control Techniques

Control techniques have developed over time. Traditional techniques rely on proven practices whereas modern techniques use technology for real-time information and sophisticated analysis.

Traditional Control Techniques

These traditional control techniques rely on established methods that bring stability and a very logical approach to managing an organization’s performance. Such techniques are easy to administer and quite viable in most business environments.

- Budgetary Control: Budgetary control involves making budgets and comparing the actual performance with the budgets. This helps in the effective use of resources and in the identification of areas where more money is being spent than budgeted for. For example, a company can budget for a marketing campaign and monitor the amount spent to avoid overspending.

Budgets are very specific and help business organizations focus and avoid financial management mistakes. At the same time, they serve as a control that allows the managers to track their performance periodically.

- Standard Costing: Standard costing establishes standard costs for specific activities, which may be a production or a purchase activity. Managers compare the actual costs against standards to identify and correct variances. Standard costing and budget control are different in their aspects.

For example, a manufacturing firm may set a standard cost for the production of a unit of product. When actual costs are higher than the standard, managers identify and correct inefficiencies. Standard costing enhances operational efficiency by keeping control over costs.

- Statistical Quality Control: Control employs statistical techniques to monitor product quality. Control charts, sampling, and process capability analysis control the productions at acceptable quality limits.

For example, an automobile parts manufacturing factory can use control charts to detect defects at the early stages of production. SQC prevents waste, increases the reliability of products, and achieves customer satisfaction.

- Direct Supervision and Observation: Direct supervision and observation refer to the management overseeing activities in real time. Managers monitor employees and processes in real time, ensuring that standards are followed and deviations are detected on time.

For example, a store manager can watch how customers interact with the employees of the store so that the latter will be reminded to follow the protocols of the company. It is a practical approach that ensures instant feedback and correction, leading to better overall performance and discipline.

- Financial Statements: Financial statements-balance sheet, income statement, and cash flow statements-are essentials that must be accounted for in judging the financial position of an entity. From all these statements, managers can draw revenues, expenses, and profitability that they are obliged to know.

For instance, through an income statement, a manager can detect a downward trend in profit margin that can lead him or her to change pricing or cost strategies. Financial statements make the case transparent to support informed decision-making.

- Break-Even Analysis: A break-even analysis helps in determining at which point the total revenues are equal to the total costs. The tool is specifically very effective in assessing new project feasibility and assessing price strategy.

For instance, a start-up launching a new product may find out how many units need to be sold to break even through the use of break-even point calculation. Break-even analysis provides insights into financial planning as well as risk assessment. Financial planning and risk assessment.

| Traditional Techniques | Description |

| Budgetary Control | Allocates resources and compares expenditures to ensure financial discipline. |

| Standard Costing | Sets cost benchmarks and identifies variances for improved efficiency. |

| Statistical Quality Control | Uses statistical tools to monitor and maintain product quality. |

| Direct Supervision and Observation | Managers oversee activities in real time to ensure adherence to standards. |

| Financial Statements | Evaluates financial health using balance sheets, income statements, and more. |

| Break-Even Analysis | Determines the point where revenues equal costs for better decision-making. |

These traditional techniques offer practical and reliable ways to monitor organizational performance and maintain control. Combining them with modern tools can further enhance their effectiveness.

Modern Control Techniques

Modern control techniques employ current tools and methods to manage today’s complex business environment. The technique gives real-time information, increases flexibility, and enables strategic decisions.

- Balanced Scorecard: The balanced scorecard is a measure of the performance of an organization from four perspectives: financial, customer, internal processes, and learning and growth. It provides an all-rounded perspective of success because it aligns activities with strategic goals.

For instance, a software company can view the scores of how the customers are satisfied along with the increase in revenue. Therefore, it can retain its profits while sustaining a good user experience.

- KPI: KPI refers to the short form of key performance indicators. It is interpreted as measurable specific factors that enable it to understand how the company is working. KPIs aid in measuring the companies as they are always put under review. Therefore, it aids in making suitable decisions.

For example, an e-commerce business could use KPIs such as website conversion rates and average order values to assess the effectiveness of marketing.

- Data Analytics: Data analytics is the process of analyzing large data sets to identify trends, predict results, and optimize processes. Organizations use it to make better decisions and allocate resources more effectively.

For example, a logistics company might analyze delivery data to reduce delays and enhance customer satisfaction.

- Return on Investment: ROI calculates a return on the investments based upon the net gains acquired in comparison with the costs accrued. The technique lets managers judge and allocate resources where the project or investment seems worthy.

For instance, a digital campaign marketing head may determine whether to further ramp up a project by computing ROI. A strong ROI indicates successful investment whereas a low ROI has to be studied again.

- Management Audit: A management audit is the systematic assessment of an organization’s policies, procedures, and practices to determine whether they are aligned with objectives. It determines inefficiencies, improves operations, and ensures that there is compliance with the regulations.

For instance, the company’s training programs may not meet the recommended requirements, which would provoke management to improve employee development work.

- PERT and CPM Methods: PERT and CPM are project management techniques through which large projects are planned, scheduled, and managed. They identify critical activities of a project while optimizing the time allocated to use resources.

Example: A building construction company would use PERT to anticipate the time required to finish a project. It would then use PDP for critical-path activities that may cause project delays.

- Self-Control: Self-control gives employees the power to determine their performance and act accordingly as per the design of the organization. Self-control is a concept of personal control and autonomy.

Example: The organization would offer dashboards for performance. Employees would track their performances and correct them without the manager interfering.

- Responsibility Accounting: Responsibility accounting defines specific budgets and performance targets to specific managers or departments to achieve the results. It increases transparency and accountability all over the organization.

Example: A budget for a campaign is assigned to the marketing department, and its manager is responsible for getting a specific ROI. In case of failed achievement of goals, corrective measures are adopted.

| Modern Techniques | Description |

| Balanced Scorecard | Measures performance across multiple dimensions to align with strategic goals. |

| Key Performance Indicators | Tracks specific metrics to assess progress and effectiveness. |

| Data Analytics | Analyzes large datasets to optimize decision-making and predict outcomes. |

| Return on Investment (ROI) | Measures profitability to evaluate investment success and guide resource allocation. |

| Management Audit | Evaluates organizational policies and practices to ensure efficiency and compliance. |

| PERT and CPM Techniques | Plans and monitors large projects by identifying critical tasks and timelines. |

| Self-Control | Encourages employees to regulate their performance and take responsibility. |

| Responsibility Accounting | Assigns accountability for budgets and targets to managers or departments. |

Modern control techniques help an organization react speedily to change, employ resources effectively, and attain strategic objectives. It is well-balanced and comprehensive in its application with traditional controls.

Advantages and Disadvantages of Control Techniques

Control methods have several benefits but still come with some drawbacks. Businesses, however, know this position and make proper utilization of it.

Advantages Of Control Techniques

Control techniques enhance organizational performance by offering clear benchmarks, optimizing resources, and ensuring accountability. These methods enable managers to make informed decisions and maintain efficiency.

- Better decision making: Control methods enhance the process of making decisions because, through the control techniques, the managers acquire some essential information to formulate their decisions. Monitoring regularly keeps the businesses proactive and responsive to change.

- Benefit from KPI: KPIs will come in handy to identify the areas that need to be developed in laggard regions by evaluating the sales. The managers would then be able to focus on areas that need improvement.

- Accountability and Transparency: The control methods ensure that the employees are answerable for their tasks. The regular evaluation makes the role and responsibility of the people involved clear, thus fostering a trustful and transparent atmosphere. For example, internal audits inform the management of errors in the financial accounts, and therefore, the organization will always be fraud-free.

Disadvantages Of Control Techniques

Despite the benefits, control techniques have some limitations, such as high implementation costs, resistance from employees, and time-consuming processes. These limitations need careful planning and management to overcome.

- Resource-Intensive: Sophisticated control techniques require a lot of time, money, and effort. Small-scale organizations do not use complex tools such as balanced scorecards or AI-based analytics.

- Resistance to Change: New controls may be viewed as intruders and therefore resisted by employees. Effective communication and training can also overcome these problems.

As mentioned above, a real-time monitoring tool alters the pattern of workflow of staff, and hence it is also a source of resistance in initial stages.

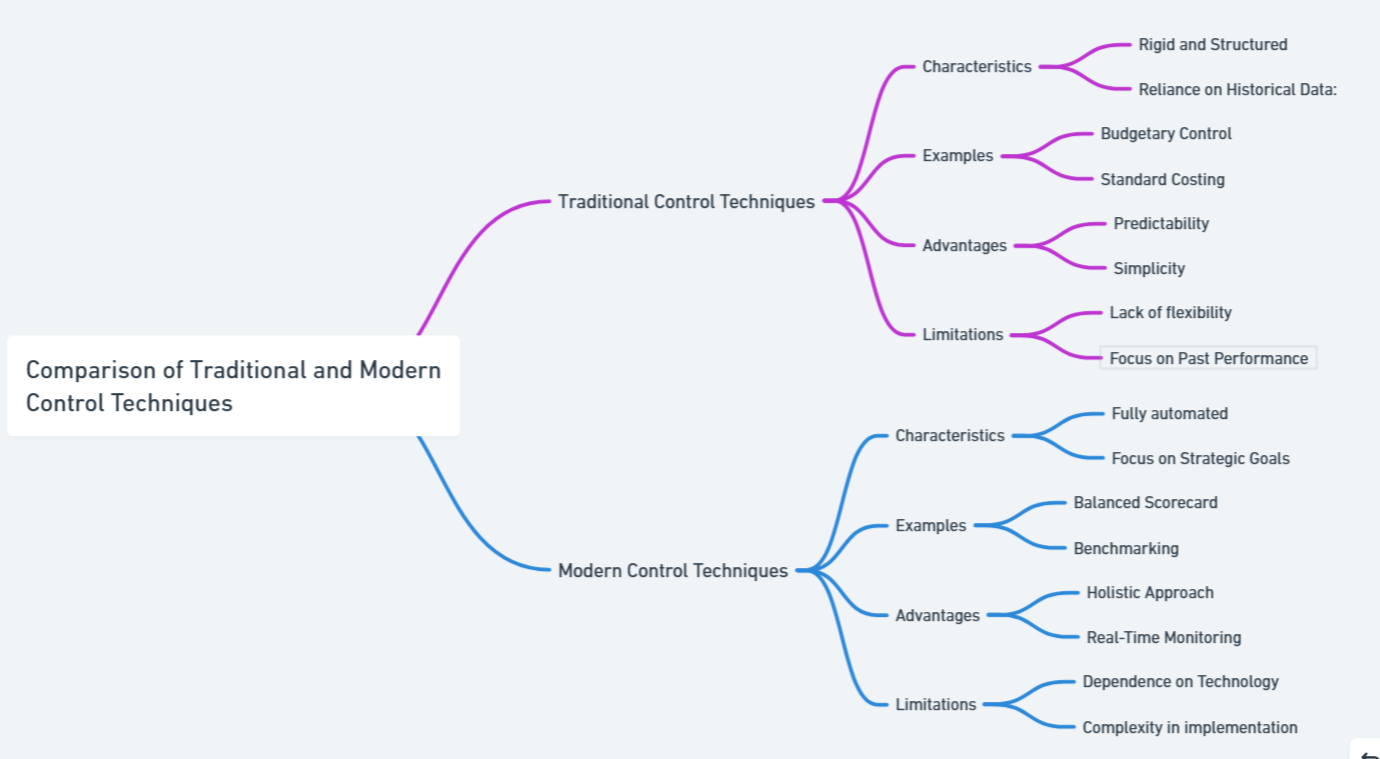

Comparison Between Traditional and Modern Control Techniques

The following table compares the classic and new methods of control against various parameters. It elaborates on the features, strengths, and weaknesses and enables an organization to understand how to apply these methods judiciously. This table examines the parameters such as cost, complexity, adaptability, and employee involvement as well and acts as a guide for selecting the right control techniques appropriate for the organizational needs and objectives.

| Parameter | Traditional Control Techniques | Modern Control Techniques |

| Definition | Established methods used for monitoring and regulating activities based on historical practices. | Advanced methods leveraging technology, data, and strategic frameworks to monitor activities. |

| Complexity | Simple and easy to understand; requires basic managerial skills. | Complex and requires specialized knowledge, tools, and expertise in technology. |

| Focus | Focuses primarily on financial and operational aspects. | Emphasizes strategic alignment, real-time insights, and multi-dimensional performance. |

| Flexibility | Less adaptable; periodic reviews may delay responses to changes. | Highly adaptable; allows for real-time updates and adjustments. |

| Examples | Budgetary control, financial statements, standard costing, direct supervision. | Data analytics, balanced scorecard, KPIs, PERT, CPM, and ROI measurement. |

| Cost | Cost-effective; uses basic tools and methods. | Expensive; requires investment in technology and skilled personnel. |

| Implementation Time | Quicker to implement due to simplicity. | Takes longer to implement due to advanced tools and training needs. |

| Data Use | Relies on historical data and manual records. | Utilizes real-time data and advanced analytics for decision-making. |

| Scope | Limited to monitoring financial health and operational efficiency. | Broader scope, including customer satisfaction, employee performance, and strategic goals. |

| Scalability | Suitable for small to medium-sized businesses. | Scalable for global operations and large organizations with complex systems. |

| Employee Involvement | Low employee involvement; focuses on managerial oversight. | Encourages employee participation through tools like self-control and responsibility accounting. |

| Technology Dependence | Minimal use of technology; relies on manual processes. | High dependence on technology; including AI, automation, and analytics tools. |

| Risk Management | Addresses risks reactively after they occur. | Proactively identifies and mitigates risks using predictive analysis. |

| Transparency | Limited to periodic audits and reports. | Provides transparency through real-time dashboards and continuous monitoring. |

Control Techniques FAQs

What are control techniques in management?

Control techniques include the mechanisms that help managers track activity as well as controls so that they meet the objectives and guidelines given by an organization.

What is the difference between modern control techniques and traditional control techniques?

The traditional control techniques are simple tools, for example, a budget, whereas modern control techniques are sophisticated technology, for example, data analytics providing real-time insights.

Why do control techniques matter?

They assure effectiveness, responsibility, and risk aversion, hence enabling organizations to achieve their aims effectively.

Do control techniques apply to small-scale businesses?

Yes, because quite a few small business-friendly tools are available-including some cloud-based analytics platforms, which makes modern techniques applicable to small businesses.

What are the main limitations of control techniques?

High costs, resistance to change, and resource-intensive implementation are common challenges faced by organizations.