Fire insurance is an insurance cover for damages incurred due to fire accidents. It gives protection in the form of repairing, replacing, or reconstructing costs. The advantages of fire insurance are important both for businesses and individuals because it provides protection against monetary loss due to fires. Fire insurance protects property owners, whether commercial or residential, from unwanted financial burdens resulting from fire incidents. This cover does not only provide for losses but also allows reconstruction, reducing risk and ensuring continuation. Balancing coverage with cost allows for optimal management of risk and peace of mind.

What is Fire Insurance?

Fire insurance is a contract between the insurer and the insured, where the insurer agrees to compensate the insured for losses or damages caused by fire within a specified period. It plays a critical role in protecting assets like property, machinery, stock, and other valuables from unforeseen fire accidents. The policyholder pays a premium to secure this protection.

Features of Fire Insurance

Fire insurance provides financial protection against losses caused by fire and related risks, ensuring quick recovery for individuals and businesses. With specific coverage terms, premium payments, and exclusions, it offers a structured way to safeguard valuable assets. Understanding its features helps in choosing the right policy.

- Specific Peril Coverage: This policy protects against fire-related damages, including destruction caused by smoke, heat, or extinguishing efforts. It ensures that businesses and individuals recover from fire incidents without facing financial ruin.

- Indemnity Principle: The insurer compensates the exact amount of the loss, preventing unfair gains from claims. This principle ensures fairness and keeps premiums affordable for all policyholders.

- Subject Matter: Fire insurance typically covers physical assets like homes, offices, stock, or machinery. It ensures that essential property is safeguarded against unforeseen fire damage.

- Time-Bound Contract: The policy protects a specific term, usually one year, with an option to renew. This structure helps both the insurer and the insured manage risks effectively.

- Premium Payment: The insured pays a premium calculated based on the value of assets and their fire risk. This payment structure ensures affordability while offering adequate coverage.

- Exclusions: Risks like war, nuclear disasters, or intentional damage caused by the insured are excluded from the policy. These exclusions are clearly outlined to avoid confusion during claims.

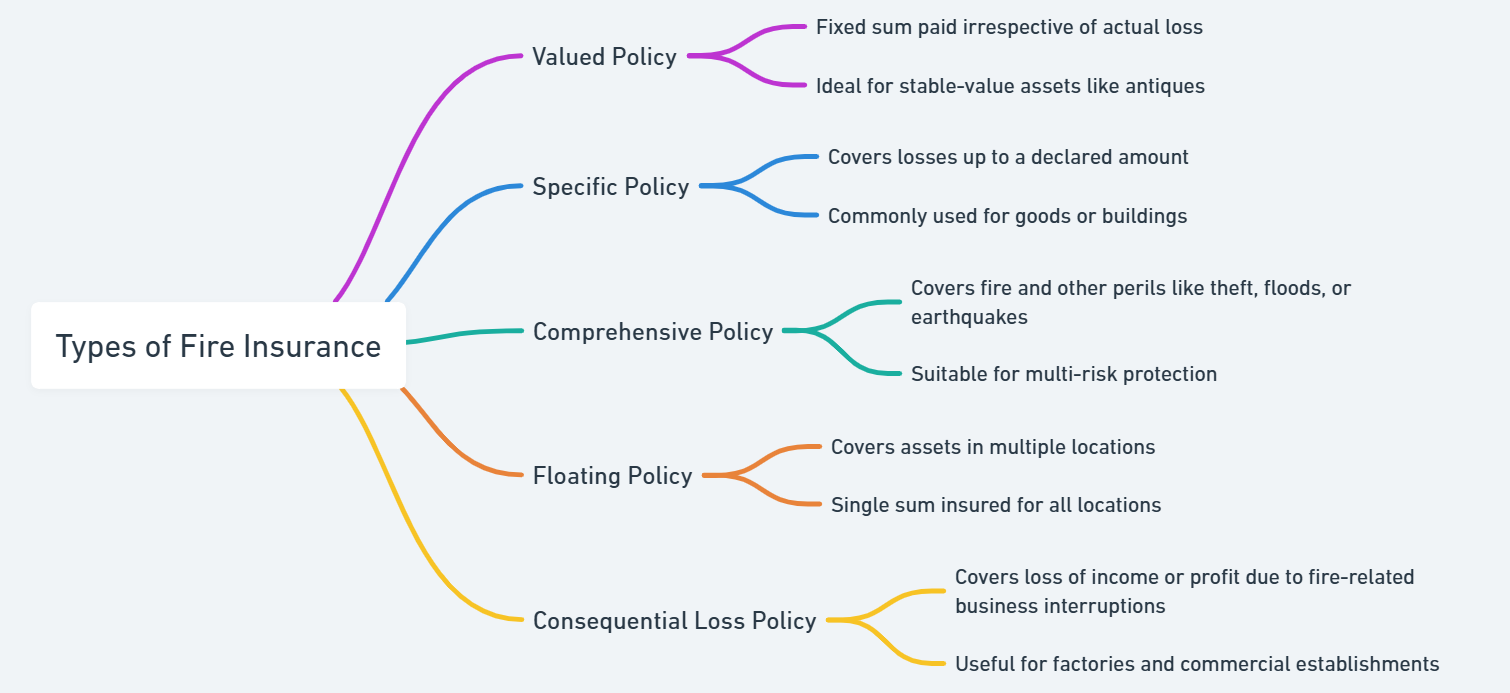

Types of Fire Insurance

Fire insurance policies come in various types to meet diverse needs, offering coverage tailored to specific assets and risks. From fixed-value protection to multi-location coverage and income recovery, these policies provide flexibility and security. Understanding their features helps businesses and individuals choose the best option.

Valued Policy

- Fixed Payment: Offers a pre-agreed sum regardless of the actual damage, ensuring predictable compensation.

- Special Assets: Designed for items like antiques, paintings, or collectibles whose value does not fluctuate.

- Example: An antique vase insured under a valued policy guarantees the owner receives the fixed insured amount even if the loss assessment differs.

Specific Policy

- Declared Coverage: Pays up to the specified limit set when the policy is purchased, covering partial or total losses.

- Common Use: Frequently used for insuring specific assets like warehouses, factories, or stored goods.

- Example: A warehouse insured for ₹50 lakhs ensures coverage up to that amount in case of fire or damage.

Comprehensive Policy

- Broad Protection: Extends coverage beyond fire to include risks like natural disasters, theft, or accidents.

- Versatile: Ideal for businesses or individuals needing all-around protection for valuable assets.

- Example: A business insures its office under a comprehensive policy to cover damage from fire, theft, and floods.

Floating Policy

- Multiple Locations: Covers assets spread across various locations under a single policy, reducing administrative hassle.

- Cost-Effective: Offers flexibility and consolidated coverage, especially useful for businesses with regional or global operations.

- Example: A retail chain uses a floating policy to ensure goods are stored in warehouses across different cities.

Consequential Loss Policy

- Income Protection: Compensates for loss of revenue or profit caused by business interruptions due to fire damage.

- Business Recovery: Helps cover fixed costs like rent, salaries, or loan repayments during downtime.

- Example: A factory uses a consequential loss policy to recover lost profits and cover employee wages while repairs are underway.

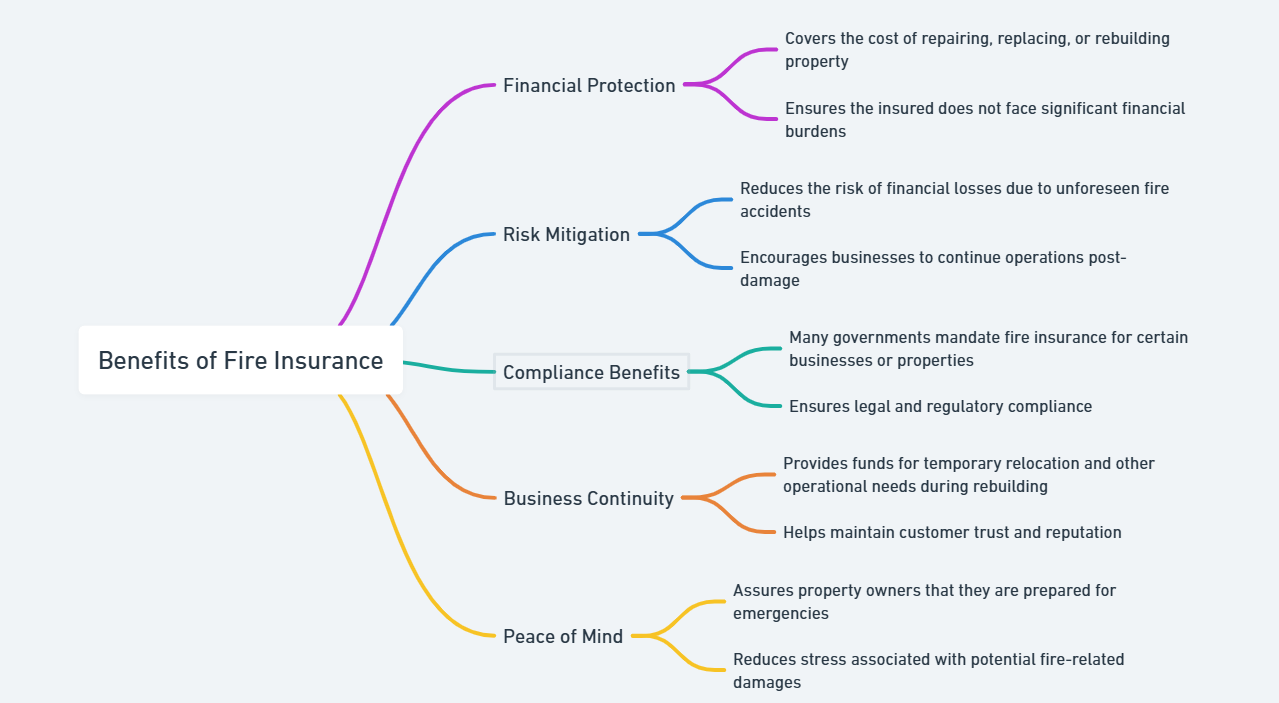

Advantages of Fire Insurance

Fire insurance provides essential financial support and protection against fire-related damages. It helps property owners, businesses, and families recover quickly by covering repair and replacement costs.

Financial Protection

- Cost Coverage: Fire insurance covers repairing, replacing, or rebuilding damaged property due to fire accidents. It ensures quick financial aid to help property owners manage their losses effectively.

- Reduced Burden: The insured does not need to dip into personal savings or take loans to cover the costs of damage. This prevents financial instability for families or businesses.

- Asset Security: Insurance safeguards your assets from complete loss, ensuring you can recover and reinvest after a fire incident.

Risk Mitigation

- Loss Reduction: Fire insurance minimizes economic loss by providing financial aid for damages. It helps businesses and families recover faster from disasters.

- Business Operations: Companies can continue their services without prolonged interruptions, as insurance helps cover immediate repair needs.

- Preparedness: It encourages property owners to stay prepared for potential risks, making them more resilient during crises.

Compliance Benefits

- Government Rules: Fire insurance ensures compliance with legal requirements set by local or national authorities. Non-compliance can lead to penalties or operational restrictions.

- Regulatory Adherence: Many countries mandate businesses or landlords to have fire insurance for safety standards. Meeting these regulations improves credibility.

- Trust Building: Being compliant with fire safety laws increases customer and stakeholder trust in your business or property management practices.

Business Continuity

- Operational Continuity: Fire insurance provides funds for renting temporary workspaces or homes while repairs are underway. This helps businesses avoid shutdowns.

- Customer Retention: By ensuring uninterrupted service, businesses can maintain their reputation and trust with clients or customers.

- Support System: Insurance serves as a financial cushion, allowing businesses to focus on recovery rather than financial stress.

Peace of Mind

- Emergency Preparedness: Property owners feel confident knowing they have a financial backup for fire-related emergencies. This reduces uncertainty and fear.

- Stress Reduction: Knowing damages are covered lowers anxiety about potential losses, allowing families and businesses to plan their futures confidently.

- Secure Environment: A well-insured property provides a sense of security to all occupants, promoting mental well-being and stability.

Disadvantages of Fire Insurance

Fire insurance has limitations that policyholders must understand to avoid unexpected challenges. Knowing the exclusions, risks, and potential drawbacks ensures informed decisions and better preparedness.

Exclusions

- Intentional Damage: Fire insurance does not cover losses caused by deliberate acts like arson or fraud by the policyholder. This ensures ethical practices and discourages misuse of policies.

- Specific Perils: Damages caused by events such as war, nuclear risks, or certain natural disasters are typically excluded unless specified in the insurance policy. Always read the terms carefully before purchasing.

- Wear and Tear: Losses due to gradual deterioration or poor maintenance of property are not included. Insurance focuses on unexpected accidents, not predictable issues.

Underinsurance Risks

- Inadequate Coverage: If the insured value is lower than the actual property value, you may receive partial compensation. This can leave you financially vulnerable during recovery.

- Property Valuation: Regularly update the sum insured to match market rates and avoid underinsurance. Many fail to reassess property value, leading to insufficient coverage.

- Policy Limitations: Understand how underinsurance clauses affect payouts and ensure your policy reflects the true worth of your assets.

High Premiums

- Costly Protection: Properties in high-risk zones, such as industrial areas, often face higher premiums due to the increased likelihood of fire incidents. This can make fire insurance expensive for some.

- Custom Coverage Costs: Adding riders or extra coverage to include specific risks can significantly increase the overall premium. Assess your needs carefully before opting for add-ons.

- Affordability Concerns: High premiums may deter individuals or businesses from purchasing adequate coverage, leaving them unprotected.

Claim Processing Delays

- Extensive Documentation: Filing a claim often requires multiple forms, evidence, and verification processes. This can slow down the settlement process significantly.

- Investigations: Insurers may take time to investigate the cause of the fire, leading to delays in disbursing funds. Be prepared to cooperate fully during this phase.

- Impact on Recovery: Delayed claims can hinder timely repairs or rebuilding, affecting business operations and personal life.

Fire Insurance FAQs

What are the main advantages of fire insurance?

Fire insurance provides financial protection, supports risk mitigation, and ensures business continuity during emergencies.

What are the key features of fire insurance?

Features include comprehensive coverage, flexibility, and repair or replacement costs reimbursement.

Are there disadvantages to fire insurance?

Yes, limitations include exclusions, underinsurance risks, and high premiums.

What types of fire insurance policies are available?

Policies include specific, comprehensive, valued, floating, and replacement policies, catering to various needs.

How can one ensure optimal fire insurance coverage?

Assess property value accurately, choose suitable coverage, and understand policy terms to avoid underinsurance or exclusions.