Business valuation refers to the calculation of the economic value of a business. Business valuation assists in making sound financial decisions about investment, mergers, acquisitions, and tax compliance. Business owners, investors, and financial planners utilise valuation to determine a company’s market status and growth potential. It’s a pivotal part of all financial planning, whether selling your business, securing loans, or making strategic decisions, so business valuation is necessary. To deliberately assess your company’s value according to its financial and market growth conditions, familiarise with concepts of the various business valuation approaches.

What is Business Valuation?

Business valuation is the accounting process of establishing a business’s fair market value based on its assets, liabilities, income, and potential growth opportunities. It approximates a business’s value and assists stakeholders in making financial decisions.

Factors Affecting Business Valuation

Business valuation is based on several factors determining its market and investment value. The major factors, such as revenue, market trends, assets, competition, and growth potential, are responsible for determining the real value of a business. The following are the main factors influencing business valuation.

- Revenue and Profitability: Greater earnings contribute to a higher business valuation. Businesses with healthy profits gain more investors. Regular revenue growth enhances financial stability.

- Market Trends: Economic conditions and industry demand influence valuation. An increasing market enhances the value of businesses. Evolving consumer needs also influence long-term success.

- Assets and Liabilities: They are determined by the assets’ net worth and value after deducting liabilities. Companies with higher-value assets are in a better financial position. Value is increased with minimising liabilities.

- Competitive Position: A company’s brand equity and market share can impact valuation. Too much competition can impact pricing power. Customers are confident of a company with a powerful brand, and its value is higher.

- Growth Potential: The growth potential of the company is very important as well. Companies with novel schemes get higher valuations. Long-term profitability comes from expansion prospects.

How Business Valuation Works?

Business valuation is performed by analysing financial data, assessing market conditions, and employing valuation models. Business valuation is a complex calculation that helps make effective financial decisions. Learning how to value a business ensures that a company’s worth is evaluated correctly.

- Gathering Financial Information: The data room for financial information should comprise balance sheets, income statements and cash flow statements. Examine past earnings, trends in revenue, and predictions. Truth in financial data leads to truth in the valuation process. It reveals the company’s virtues and vices.

- Valuation Method Selection: Choose a suitable business valuation method depending on the industry and finance structure. Use varying valuation models for an in-depth evaluation. The right method enhances accuracy. It makes the business value represent its real market worth.

- Market and Industry Analysis: Benchmark the business against industry standards and competitors. Assess demand, growth potential and economic clout. Realistic valuation relies on knowledge of market trends. Strong business positioning adds value to the business.

- Calculating the Business Value: Use financial computation and valuation models to calculate business worth. Account for risk factors, market forces and economic stability.” Reasonable valuation is a good calculation. It helps investors and owners to make better decisions.

- Final Valuation Report: Prepare findings as a final valuation report. In this context, you should make recommendations to investors, buyers/entrepreneurs. An open report provides greater transparency. It aids in negotiations and strategising planning.

Business Valuation Methods

Different business valuation methods provide insights into a company’s financial standing. These methods vary based on industry type, economic data, and valuation purposes.

Asset-Based Valuation Method

The asset-based valuation Method determines the value of a business by subtracting its liabilities from total assets. It considers the company’s physical and financial assets, including property, machinery, and inventory. This method is most suitable for companies with large tangible assets, such as manufacturing or real estate companies. It is unsuitable for service or technology companies that use intangible assets like goodwill and intellectual property.

Market-Based Valuation Method

The market-based valuation approach estimates a business by comparing it to comparable companies in the market or applying industry multiples. It usually depends on the Price-to-Earnings (P/E) ratio, which calculates the business value based on market expectations. The approach is most suitable for publicly traded businesses and industries with distinct market benchmarks. It might not be suitable for small businesses with limited comparable market data.

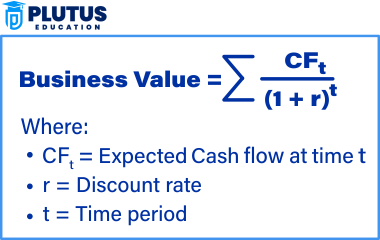

Income-Based (Discounted Cash Flow) Valuation Method

The discounted cash flow (DCF) method or income-based valuation method estimates the value of a business by discounting its future cash flows to its present value. It considers the time value of money and is appropriate for growth businesses with certain future earnings. It demands precise revenue forecasts and discount rates and is thus inappropriate for startups with indefinite cash flows.

Earnings Multiplier Method

Using an industry-specific multiple, the earnings multiplier method values a company based on its net profit. Companies with stable and stable earnings are at an advantage using this method, as it indicates profitability. It is most commonly applied to value well-established companies operating in stable industries. It fails to be useful for firms with unstable earnings or substantial losses.

Book Value Method

The book value method is a valuation based on a company’s net worth, using assets as reported in its financial reports. It divides the difference between total assets and total liabilities by the number of outstanding shares. The method works well for stable financial firms but ignores intangible assets and future growth prospects.

Reasons for Performing Business Valuation

Businesses and investors conduct business valuations for several strategic, financial, and regulatory purposes. Some of the key reasons for business valuation are discussed below.

- Mergers and Acquisitions: Establishes the fair value of a firm before sale or merger. Assists firms in negotiating a better bargain. Proper valuation allows both parties to gain from the deal. It also avoids loss of money on account of inappropriate pricing.

- Investment and Financing: Helps obtain investments and business loans. Gives investors an estimate of returns. A properly valued business attracts more investors and expands financing opportunities. It also enables lenders to gauge financial stability.

- Financial Reporting and Compliance: Necessary for taxation, legal proceedings, and regulatory filings. Provides compliance with financial regulations. Valuation to keep financial records transparent. Proper valuation prevents companies from incurring legal penalties and financial discrepancies.

- Business Restructuring: Facilitates planning for company growth or dissolution. Clarifies financial well-being before restructuring. It helps companies determine profitable areas for expansion. Strong valuation enables more informed decision-making in restructuring strategies.

- Exit Strategy Planning: Business owners decide when to sell their business. Maximises returns on sale transactions. Accurate valuation enables owners to negotiate the optimal deal. It also facilitates a smooth change in ownership.

- Shareholder Disputes and Estate Planning: Applied to resolve disputes relating to ownership between partners or shareholders. Aids in business succession and financial planning. Valuation facilitates an equal distribution of assets. Also aids in conflict resolution and legal settlements.

Relevance to ACCA Syllabus

Business valuation is a major part of ACCA’s Financial Management (FM) and Advanced Financial Management (AFM) papers. It helps students understand various methods of valuation, such as Discounted Cash Flow (DCF), Price/Earnings (P/E) ratio, and Net Asset Value (NAV). These are significant topics in corporate finance, mergers and acquisitions, and investment choices.

Business Valuation ACCA Questions

Q1: Which of the following valuation methods is based on the present value of future cash flows?

A) Price-to-Earnings (P/E) Ratio

B) Discounted Cash Flow (DCF) Method

C) Net Asset Value (NAV) Method

D) Market Capitalization

Ans: B) Discounted Cash Flow (DCF) Method

Q2: The Price-to-Earnings (P/E) ratio is commonly used to value:

A) Fixed assets

B) Debt securities

C) Equity shares

D) Inventory

Ans: C) Equity shares

Q3: If a company’s earnings per share (EPS) is $5 and its stock price is $50, what is its P/E ratio?

A) 5

B) 10

C) 15

D) 25

Ans: B) 10 (P/E Ratio = Stock Price / EPS = 50 / 5)

Q4: Which valuation method considers the liquidation value of a company’s assets?

A) Market-based valuation

B) Discounted Cash Flow (DCF)

C) Net Asset Value (NAV)

D) Price/Earnings (P/E) Ratio

Ans: C) Net Asset Value (NAV)

Q5: What is a key limitation of the Net Asset Value (NAV) method in business valuation?

A) It ignores intangible assets and future earnings potential

B) It always provides a higher valuation than market-based methods

C) It does not consider company liabilities

D) It only applies to large corporations

Ans: A) It ignores intangible assets and future earnings potential

Relevance to US CMA Syllabus

The US CMA syllabus handles business valuation under Corporate Finance and Investment Analysis. CMA aspirants must value a company’s financial value through valuation methods like Earnings Multiples, Discounted Cash Flow (DCF), and Market-based valuation. This is crucial for financial planning, investment, and business strategy decision-making.

Business Valuation US CMA Questions

Q1: What is the primary objective of business valuation?

A) To determine the book value of assets

B) To assess the fair market value of a company

C) To calculate tax liabilities

D) To measure cash flow ratios

Ans: B) To assess the fair market value of a company

Q2: Which business valuation method estimates the total worth of a company by comparing it with similar companies in the industry?

A) Net Asset Value (NAV) Method

B) Discounted Cash Flow (DCF) Method

C) Comparable Company Analysis (CCA)

D) Historical Cost Method

Ans: C) Comparable Company Analysis (CCA)

Q3: When using the Discounted Cash Flow (DCF) method, which rate is used to discount future cash flows?

A) Inflation rate

B) Weighted Average Cost of Capital (WACC)

C) Earnings Before Interest and Taxes (EBIT)

D) Gross Profit Margin

Ans: B) Weighted Average Cost of Capital (WACC)

Q4: The Net Asset Method is most suitable for valuing:

A) High-growth technology startups

B) Asset-intensive businesses like real estate and manufacturing

C) Companies with a high Price-to-Earnings (P/E) ratio

D) Firms with strong brand value and goodwill

Ans: B) Asset-intensive businesses like real estate and manufacturing

Q5: If a company has a market capitalization of $500 million and annual net income of $50 million, what is its P/E ratio?

A) 5

B) 10

C) 15

D) 20

Ans: B) 10 (P/E Ratio = Market Capitalization / Net Income = 500M / 50M)

Relevance to US CPA Syllabus

The US CPA syllabus addresses Business valuation under Financial Accounting and Reporting (FAR) and Business Environment and Concepts (BEC). CPA candidates should know financial reporting, taxation, and advisory services valuation methods. They also study business value in mergers, acquisitions, and fair value accounting (ASC 820 Fair Value Measurement).

Business Valuation US CPA Questions

Q1: Which financial statement is most important for business valuation using the Net Asset Method?

A) Income Statement

B) Statement of Cash Flows

C) Balance Sheet

D) Statement of Retained Earnings

Ans: C) Balance Sheet

Q2: Under US GAAP, which accounting standard governs fair value measurement?

A) ASC 606

B) ASC 842

C) ASC 820

D) ASC 740

Ans: C) ASC 820 (Fair Value Measurement)

Q3: What is the main drawback of the Price-to-Earnings (P/E) ratio in valuation?

A) It does not consider future growth potential

B) It is based on historical earnings, which may not be reliable

C) It only applies to private companies

D) It always overvalues companies

Ans: B) It is based on historical earnings, which may not be reliable

Q4: When valuing a business using the Discounted Cash Flow (DCF) method, which factor is crucial?

A) Current liabilities

B) Cost of goods sold

C) Discount rate (WACC)

D) Revenue recognition policy

Ans: C) Discount rate (WACC)

Q5: A business with stable cash flows and low asset value is best valued using:

A) Net Asset Value (NAV) Method

B) Market Capitalization

C) Price/Earnings (P/E) Ratio

D) Discounted Cash Flow (DCF) Method

Ans: D) Discounted Cash Flow (DCF) Method

Relevance to CFA Syllabus

The valuation of a business is an integral subject area in Equity Investments and Corporate Finance within the CFA program. The candidates in the CFA must be competent with valuation tools like Enterprise Value (EV), Discounted Cash Flow (DCF), Price Multiples, and Comparable Company Analysis. These subjects play a critical role in investment analysis, management of portfolios, and mergers and acquisitions.

Business Valuation CFA Questions

Q1: The Enterprise Value (EV) of a company is calculated as:

A) Market Capitalization + Total Debt – Cash

B) Net Profit + Depreciation

C) Total Assets – Total Liabilities

D) Price/Earnings (P/E) Ratio × Net Income

Ans: A) Market Capitalization + Total Debt – Cash

Q2: Which valuation method best reflects a company’s intrinsic value?

A) Market-based valuation

B) Discounted Cash Flow (DCF) Method

C) Net Asset Value (NAV) Method

D) Dividend Discount Model (DDM)

Ans: B) Discounted Cash Flow (DCF) Method

Q3: The Terminal Value in a Discounted Cash Flow (DCF) model represents:

A) The present value of future dividends

B) The projected residual value of a company beyond the forecast period

C) The cost of capital for the business

D) The market price of outstanding shares

Ans: B) The projected residual value of a company beyond the forecast period

Q4: Which valuation method is commonly used for private companies?

A) Market-based valuation

B) Net Asset Value (NAV)

C) Price-to-Earnings (P/E) Ratio

D) Dividend Yield

Ans: B) Net Asset Value (NAV)

Q5: What does a high P/E ratio generally indicate about investor expectations?

A) Investors expect high future growth

B) The company is facing financial difficulty

C) The stock price is undervalued

D) Investors expect lower dividends

Ans: A) Investors expect high future growth