Credit risk analysis is the method of analysing the creditworthiness of persons or organisations to assess their capacity to repay loaned money. Banks, lenders, and investors utilise credit risk analysis models to predict the likelihood of default and reduce financial loss. The ability to perform credit risk analysis is crucial for banks and companies that involve lending or credit-based transactions. By applying systematic evaluation methods, businesses can make effective judgments when issuing loans or giving credit.

What is Credit Risk Analysis?

Credit risk analysis evaluates the probability that a borrower will fail to repay a loan or financial obligation. It assists lenders in deciding if an individual or business is financially sound enough to repay borrowed money on time. Lenders use corporate credit risk analysis to evaluate businesses seeking loans, verifying financial stability before granting credit.

Factors Considered in Credit Risk Analysis

Credit risk analysis allows lenders to assess borrowers’ ability to repay loans and minimise financial risk. It considers their credit history, level of debt, collateral, and economic conditions to determine the loans offered and at what rates. The following are the primary risks considered while doing credit risk analysis.

- Borrower’s Credit History: Payment history and credit score establish the borrower’s credibility. A good credit history improves the chances of loan approval. Lenders like borrowers with regular payment habits. A bad credit history can result in higher interest rates.

- Debt-to-Income Ratio: The ratio compares the overall debt levels with the income level to be able to pay back. A lower ratio is considered more financially favourable. And lenders use this to make sure that the borrower can take on new debt. High levels of debt decrease the likelihood of being approved for loans.

- High-Value Assets: Collaterals are those assets pledged against security for the loan. Collateral secures risk to the lender on the ability to repay. Having valuable assets can enhance your loan terms and lower the interest rate. You would get higher loan amounts with stronger collateral.

- Economic Conditions: Market trends affecting the ability to repay impact lending. Downturns increase the financial risk that lenders and borrowers assume. When market conditions are stable, borrowing is easier.

Purpose of Credit Risk Analysis

Credit risk analysis is crucial in financial decision-making. It assists lenders, companies, and investors in minimising the risks involved in credit transactions. Financial institutions and companies analyse credit risk to guarantee prudent lending and financial safety.

- Helps in Loan Approval Decisions: Evaluate whether the borrower qualifies for a loan. Pruthvi set the correct interest rates based on the risk levels. Responsible lending comes from a careful analysis of risk. All these combined mean a lesser risk of loan defaults.

- Protects Lenders from Default: Prevents banks and financial institutions from suffering loan losses. Pinpoints high-risk borrowers before lending. Detection of risk early on averts financial instability. Lenders can dictate loan terms depending on the risk levels.

- Provides Business Stability: Corporate credit risk analysis helps businesses assess customers before granting credit translation and charge them interest. Minimises unpaid invoices burdening cash flow. Good risk management enhances financial planning. It allows businesses to have a stable income.

- Enhances Investment Decisions: Investors review their credit risk before investing in bonds and other securities. Aids in determining the financial soundness of a company and its capability to meet repayment obligations. Investments get safer because of lower credit risk. By picking financially sound companies, investors can save themselves from huge losses.

- Ensures Regulatory Compliance: Banks and financial institutes must comply with regulatory lending guidelines. Ensures adherence to risk management policies. Following rules avoid breaching the law. Building trust with regulators and investors through proper risk assessment.

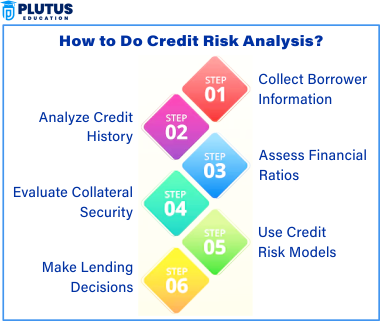

How to Do Credit Risk Analysis?

Performing credit risk analysis requires a structured approach to evaluate borrower reliability. Lenders and financial institutions follow these steps to minimise credit risk and ensure responsible lending.

Step 1: Collect Borrower Information

Lenders typically begin by gathering the borrower’s personal and financial information, including income, employment status and assets. Lenders also pull credit reports from Experian, Equifax or TransUnion to understand consumer’s economic history. This helps assess the borrower’s value before further analysis.

Step 2: Analyze Credit History

Lenders assess the borrower’s payment record, liabilities and credit use. They look for late payments, loan defaults, or bankruptcies, all signs of financial trouble. An applicant with a good track record of repayment has a higher chance of getting the loan than someone with a poor credit record, where there are possibilities of being denied or having to pay higher interest rates.

Step 3: Assess Financial Ratios

Financial ratios are the next in line to measure the borrower’s financial condition. Debt-to-income ratio (DTI) compares total debt with income, indicating the borrower’s capacity to handle additional debt. Liquidity ratio tracks a company’s cash available to pay its debts. These ratios give lenders visibility into how much they can afford and their risk level when offering loans.

Step 4: Evaluate Collateral Security

In the case of secured loans, lenders will assess the borrower’s assets, such as real estate, vehicles, or savings, to establish if they can be collateral. They evaluate the market value of these assets and their liquidation possibilities. A well-secured loan reduces the lender’s risk and is therefore accompanied by interest on the loan and better terms.

Step 5: Use Credit Risk Models

Lenders use credit-risk analysis models such as the probability of default model credit scoring. These models draw upon statistical measurements and financial metrics to estimate risks to repayment. Informed lending decisions are made using data and advanced financial modelling, which helps to minimise the risk of delinquent loans.

Step 6: Make Lending Decisions

Lenders accept, deny, or adjust loan terms based on the risk assessment. Low-credit-risk borrowers are extended better loan terms, while high-risk borrowers may be hit with higher interest rates or more difficult terms. Risk assessment is also the backbone of the credit appraisal process because a well-structured risk assessment guarantees responsible lending and financial security for both borrowers and lenders.

Why is Credit Risk Analysis Important?

Credit Risk Analysis is essential to financial stability and risk management. It assists lenders and companies in making sound decisions while granting credit.

- Avoids Financial Losses: Pinpoints borrowers most likely to default on loans. Stunts the buildup of bad debt in financial institutions.

- Enhances Lending Decisions: Assists banks and lenders in approving or rejecting loans. Enables lenders to charge suitable interest rates depending on risk.

- Strengthens Business Continuity: Shields businesses from unpaid invoices and credit default. It helps you make prudent trade credit decisions.

- Supports Risk Management Strategies: Assists financial institutions in balancing their loan portfolio. Ensures compliance with credit risk management policies.

- Helps in Regulatory Compliance: Financial regulations imposed on banks require them to follow risk assessment processes. Avoids penalties of legal grade and financial due to risk bad assessment.

Credit Risk Analysis Models

Several credit risk analysis models assist lenders and companies in determining borrower risk. These models rely on financial information, statistical methods, and machine learning techniques. Lenders utilise credit risk analysis models to enhance decision-making and minimise loan default risks.

Credit Scoring Models

Credit scoring models provide a numerical value to borrowers based on their credit history, payment history, and financial health. FICO Score and VantageScore are typical models used by lenders to determine levels of risk. A high credit score (750+) reflects low risk, while a low score (less than 600) reflects high risk, resulting in more stringent loan conditions.

Probability of Default (PD) Models

Probability of default models estimate the chance of a borrower defaulting on a loan. Such models use historical financial data, market trends and borrower history to assess risk. Using PD models, lenders can flag high-risk applicants and approve loans only for financially stable borrowers.

Altman Z-Score Model

The Altman Z-Score Model is a credit risk analysis model used to predict the bankruptcy risk of an enterprise. It uses financial ratios like working capital, retained earnings, and total assets to evaluate stability. Firms that have low Z-scores are at greater risk of financial distress, so this model has utility for both investors and lenders.

Machine Learning Models for Credit Risk

Machine learning models employ AI and data analytics to assess borrower risk. These models incorporate data about large datasets, transaction history, and spending behavior to predict risk chances better. Machine learning has streamlined credit assessment that allows lenders to make quicker and more accurate credit decisions, resulting in reduced default rates and improved efficiency of loan procedures.

Credit Migration Models

Credit migration models follow the evolution of a borrower’s credit rating over time. Banks and financial institutions leverage these models to track credit risk trends and determine long-term repayment capacity. A credit rating downgrade can signal increased default risk, while upgrades may imply a stronger financial position.

Relevance to ACCA Syllabus

Credit Risk Analysis is a primary topic for the ACCA exam under Financial Management (FM) and Advanced Financial Management (AFM). The area concentrates on examining the credit default risk of the borrowers and management of the business about credit risk employing tools such as credit scoring model, financial ratios analysis, and credit risk-reducing techniques. The candidates in ACCA understand the measurement of businesses’ credit quality and its employment in making investment decisions and for assessment.

Credit Risk Analysis ACCA Questions

Q1: What is the primary goal of credit risk analysis?

A) To determine a borrower’s likelihood of default

B) To maximize the company’s total liabilities

C) To reduce operational costs

D) To increase a company’s marketing budget

Ans: A) To determine a borrower’s likelihood of default

Q2: Which financial ratio is most commonly used to assess credit risk?

A) Debt-to-Equity Ratio

B) Price-to-Earnings (P/E) Ratio

C) Inventory Turnover Ratio

D) Dividend Payout Ratio

Ans: A) Debt-to-Equity Ratio

Q3: Under IFRS 9, how are expected credit losses (ECL) recognized?

A) Only when a default has occurred

B) Based on a forward-looking model

C) At the discretion of the financial manager

D) Only for companies with a high credit rating

Ans: B) Based on a forward-looking model

Q4: A company assesses credit risk using a customer’s financial statements. Which key factor is most important?

A) Profitability and liquidity ratios

B) Marketing expense ratio

C) Employee turnover rate

D) Dividend yield

Ans: A) Profitability and liquidity ratios

Q5: What is the purpose of a credit rating?

A) To evaluate a company’s likelihood of meeting its financial obligations

B) To measure a company’s operational efficiency

C) To determine its total assets

D) To assess employee productivity

Ans: A) To evaluate a company’s likelihood of meeting its financial obligations

Relevance to US CMA Syllabus

Credit risk analysis comes under Corporate Finance and Risk Management in the US CMA syllabus. CMA candidates evaluate credit risk through financial statement analysis, debt ratios, and cash flow forecasting. Financial managers must ascertain credit policies, maximise working capital, and handle corporate credit exposure.

Credit Risk Analysis US CMA Questions

Q1: What does a high debt-to-equity (D/E) ratio indicate in credit risk analysis?

A) Higher financial risk due to excessive leverage

B) Stronger ability to meet short-term liabilities

C) Lower risk for lenders

D) Higher operating efficiency

Ans: A) Higher financial risk due to excessive leverage

Q2: When assessing credit risk, which of the following is a key indicator of liquidity risk?

A) Quick Ratio

B) Return on Equity (ROE)

C) Price-to-Book Ratio

D) Gross Margin

Ans: A) Quick Ratio

Q3: A lender wants to evaluate a company’s creditworthiness. What is the most relevant financial metric?

A) Cash Flow Coverage Ratio

B) Market Capitalization

C) Advertising Budget

D) Employee Satisfaction Index

Ans: A) Cash Flow Coverage Ratio

Q4: What is the most common method used by companies to reduce credit risk?

A) Offering high-risk loans to maximize profits

B) Diversifying credit portfolios

C) Increasing dividend payments

D) Reducing inventory levels

Ans: B) Diversifying credit portfolios

Q5: If a company has a high probability of default, what action should a lender take?

A) Extend more credit to improve the company’s liquidity

B) Demand higher interest rates or require collateral

C) Ignore the risk and approve the loan

D) Increase marketing expenses

Ans: B) Demand higher interest rates or require collateral

Relevance to US CPA Syllabus

The US CPA curriculum incorporates credit risk analysis in Financial Accounting and Reporting (FAR) and Business Environment and Concepts (BEC). CPAs analyse clients’ creditworthiness, identify financial statement risk, and use risk management approaches to reduce credit losses. Audits, financial analysts, and regulatory compliance professionals need credit risk knowledge.

Credit Risk Analysis US CPA Questions

Q1: How does credit risk impact an auditor’s assessment in a financial audit?

A) It increases the likelihood of material misstatements in financial statements

B) It decreases the need for external confirmation

C) It eliminates the need for assessing cash flow statements

D) It improves the company’s overall credit rating

Ans: A) It increases the likelihood of material misstatements in financial statements

Q2: What is the key purpose of the Expected Credit Loss (ECL) model under US GAAP?

A) To recognise credit losses based on historical trends only

B) To apply a forward-looking approach in estimating losses

C) To ignore credit risk when assessing financial statements

D) To record credit losses only when default occurs

Ans: B) To apply a forward-looking approach in estimating losses

Q3: If a company’s accounts receivable turnover ratio is decreasing, what does it indicate?

A) Customers are taking longer to pay, increasing credit risk

B) The company is generating higher sales

C) The company’s credit policies are more effective

D) The company’s inventory turnover is improving

Ans: A) Customers are taking longer to pay, increasing credit risk

Q4: Which of the following is an external method for assessing credit risk?

A) Reviewing credit agency ratings

B) Analyzing employee job satisfaction

C) Measuring advertising effectiveness

D) Assessing internal communication systems

Ans: A) Reviewing credit agency ratings

Q5: How do financial institutions typically mitigate credit risk?

A) Requiring collateral from borrowers

B) Increasing tax liabilities

C) Reducing asset turnover

D) Ignoring debt ratios

Ans: A) Requiring collateral from borrowers

Relevance to CFA Syllabus

The CFA curriculum comprehensively covers credit risk analysis in fixed income, risk management, and corporate finance. CFA candidates learn credit ratings, probability of default, bond credit spreads, and risk-adjusted return analysis. These methods assist investment analysts, credit analysts, and portfolio managers in evaluating the risk exposure of investments and corporate lending.

Credit Risk Analysis CFA Questions

Q1: In fixed-income analysis, credit spreads represent:

A) The difference between yields of risk-free bonds and risky bonds

B) The total amount of outstanding debt

C) The profit margin of a company

D) The tax rate on interest income

Ans: A) The difference between yields of risk-free bonds and risky bonds

Q2: A bond issuer with a lower credit rating will typically offer:

A) Higher interest rates to compensate for increased risk

B) Lower interest rates due to high credit quality

C) A guaranteed return with no default risk

D) The same yield as government bonds

Ans: A) Higher interest rates to compensate for increased risk

Q3: What does a credit rating downgrade indicate about a company?

A) Increased credit risk and potential default concerns

B) Improved financial stability

C) Higher dividend payments

D) Lower operational costs

Ans: A) Increased credit risk and potential default concerns

Q4: Which metric is most useful for assessing the credit risk of corporate bonds?

A) Interest Coverage Ratio

B) Gross Profit Margin

C) Dividend Payout Ratio

D) Inventory Turnover Ratio

Ans: A) Interest Coverage Ratio

Q5: If a firm has a high probability of financial distress, an investor should expect:

A) Lower bond prices and higher yields

B) Increased bond prices and lower yields

C) Reduced stock price volatility

D) Guaranteed returns on equity investments

Ans: A) Lower bond prices and higher yields