Currency exchange hedging is a strategy businesses, investors, or traders use to avert foreign exchange risk. By operating globally, businesses have international transactions with fluctuating exchange rates. Because of a sudden change in currency values, costs may increase, or profits may diminish. This reduced uncertainty; lock-in rates through financial instruments or offsetting positions can be used to hedge currency. Using the forex hedging strategies, stable financing is secured, thereby preventing losses arising from volatility in the market. This is an excellent preparatory step to managing exposure to forex risk for businesses engaged in international trade because it gives financial protection and predictability in cash flows.

Currency Exchange Hedging

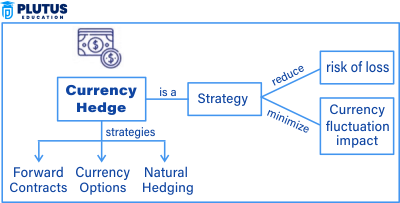

Different businesses and investors use foreign exchange hedging strategies to safeguard themselves from such risks. When a company imports or exports goods, the currency value of that transaction is closely linked to how the exchange rate changes. The result is that a falling domestic currency increases the costs for imports, while a rising domestic currency reduces the income from exports. Hedging against currency risk helps businesses forecast their financial outcomes with certainty and reduces unpleasant surprise losses. Many techniques, such as currency derivatives, forward contracts, and options, manage forex risk.

Understanding Currency Risk Management

Forex risk management is how businesses and investors mitigate losses from fluctuating exchange rates. Companies use various Foreign exchange hedging techniques to reduce the risks of international trade. If a company receives payments in foreign currency, it may be deemed a loser if the exchange rate depreciates before payment is received. Hedging currency risk provides stability to profits and guarantees profit through locking exchange rates beforehand.

FX risk mitigation includes identifying exposure, selecting an effective hedging strategy, and using financial instruments to offset potential losses. Companies often utilise currency derivatives like forward contracts, futures, and options to hedge market fluctuations.

Corporate Forex Hedging

Corporate forex hedging is the internal currency management for a multinational corporation, which typically deals with a multiplicity of currencies. Their hedge used different foreign exchange hedging instruments to manage their exposure to those various currencies. Some companies may have currency risk hedging for every transaction, while some only hedge when the risk becomes significant. It can be as easy as invoicing in domestic currency or as complicated as forward contracts and Foreign exchange options.

To ensure that companies properly hedge their risks about foreign exchange, they must assess their exposure, identify the best hedge strategy, and monitor the currency markets consistently. Businesses also use FX hedging techniques like currency swaps and futures contracts to reduce uncertainty.

Forex Forward Contracts and Options for Currency Hedging

The two most popular methods for hedging against foreign exchange risk include forex forward contracts and currency options for currency hedging. These two financial products allow an enterprise to lock in its exchange rate and remove any uncertainty about its international transactions. One or both options come into play amid such foreign exchange exposure, where these companies can achieve financial stability.

Forex Forward Contracts

A forward contract is an agreement between two parties to deliver an amount of a specified currency against an opposite transaction of another currency at an agreed rate on a future date. Forward contracts are widely used in international trade hedging because they act to eliminate risks of currency changes. Companies engaged in import and export use forward contracts to lock the exchange rate and guarantee predictability in costs.

Forex forward contracts assure businesses’ accurate budgeting. If an importer knows the future exchange rate that will be paid, it avoids the risks of sudden financial losses. While spot deals may require an immediate currency exchange, forward contracts are always followed until the term.

Options for Currency Hedging

Options for currency hedging give companies the flexibility to hedge against adverse currency fluctuations while retaining the possibility of profiting from favourable movements. Unlike forward contracts, which tie counterparties to a defined exchange rate, options allow the money to buy currency at a known price or sell it without obligation.

Options come in handy when there is uncertain information surrounding future rate movements. If the market swings favourably for a company, it may decide not to execute the option and capitalise on better rates. This option-like nature is, therefore, the quintessential reason why options are favoured by companies that want to cap downside risk while leaving room for upside potential.

Currency Swap Strategies

A currency swap involves exchanging principal or interest payments in one currency for another over a specified period. Multinationals and financial institutions commonly use the method to compensate for foreign exchange risks in long-term projects.

Currency swaps would help secure stable financing not under domestic interference in foreign markets and eliminate uncertainties relating to interest rate and exchange rate changes. Companies involved in international trade transactions and hedging operations frequently use swaps to balance income and expenses in currency, allowing smooth financial operations.

Foreign Exchange Hedging Instruments

In a different sense, foreign exchange hedging instruments provide businesses with a means to counter the risk caused by the fluctuation in foreign currency. These hedging mechanisms ensure financial stability by enabling firms to project future transactions without fear of exchange rate variations.

Currency Derivatives

Using currency derivatives such as forwards, futures, and options can serve the objective of hedging currency risk. It can also fix an exchange rate if the company is to enter into a series of transactions at the same exchange rate, or it can provide flexibility when exchange rates fluctuate.

If, on the one hand, they safeguard companies in markets that are volatile to limit the risk of losses, the company would need to plan to incorporate these financial transactions. Companies would use these tools per the principles they formulated regarding risk appetite and economic strategy.

International Trade Hedging Techniques

International trade hedging is a risk management practice for companies that spread their operations in different regions. By applying hedging techniques in the form of forward contracts, options, or swaps, companies can address the effect of exchange-rate fluctuations on their financial results.

Import-competing and -exporting companies use international trade hedging to stabilise cash flows, protect operating margins, and improve financial planning. Properly executed hedging helps companies maintain competitive pricing and stable growth opportunities in global markets.

Foreign Exchange Risk Mitigation

To mitigate currency exchange risk, enterprises should analyse the nature of exposure, devise sound strategies for hedging, and closely monitor developments in the intraday market. The companies should consider using the appropriate hedging instruments concerning the transaction sizes, risk tolerance and financial objectives.

By opportunely hedging forex exposure, businesses shelter themselves against unwarranted currency instability and try to remain profitable. It would be better for them to regularly reassess their hedging strategies to ascertain their appropriateness regarding the changing market conditions and business requirements.

Relevance to ACCA Syllabus

Currency exchange hedging is essential in the ACCA syllabus, particularly within Financial Management (FM) and Advanced Financial Management (AFM). ACCA students learn how businesses manage foreign exchange risk using forward contracts, options, and swaps. The knowledge of currency risk management is crucial for multinational corporations and financial reporting, as companies must mitigate the risks associated with fluctuating exchange rates.

Currency Exchange Hedging ACCA Questions

Q1: Which of the following is an external hedging technique used to manage foreign exchange risk?

A) Currency options

B) Leading and lagging

C) Netting

D) Matching

Ans: A) Currency options

Q2: A UK company expects to receive USD in three months. Which derivative instrument can it use to hedge against exchange rate risk?

A) Interest rate swap

B) Forward contract

C) Credit default swap

D) Equity option

Ans: B) Forward contract

Q3: Which of the following best describes the purpose of a money market hedge?

A) To speculate on exchange rate movements

B) To take advantage of arbitrage opportunities

C) To lock in the exchange rate using borrowing and lending

D) To avoid the need for financial derivatives

Ans: C) To lock in the exchange rate using borrowing and lending

Q4: Which financial reporting standard covers hedge accounting in the ACCA syllabus?

A) IFRS 7

B) IFRS 9

C) IFRS 15

D) IFRS 16

Ans: B) IFRS 9

Q5: Which strategy can a multinational company use to reduce exposure to currency fluctuations without financial instruments?

A) Cross-currency swap

B) Leading and lagging

C) Currency futures contract

D) Interest rate swap

Ans: B) Leading and lagging

Relevance to US CMA Syllabus

Currency exchange hedging is covered under the US CMA syllabus in Part 2 – Financial Decision Making. The syllabus emphasises risk management, financial derivatives, and multinational finance. CMA candidates learn to apply hedging techniques such as forward contracts and options to mitigate currency risks that impact financial planning and reporting.

Currency Exchange Hedging US CMA Questions

Q1: A company based in the US wants to hedge its exposure to expected euro payments in six months. Which instrument should it use?

A) Currency swap

B) Forward contract

C) Interest rate future

D) Equity future

Ans: B) Forward contract

Q2: A money market hedge involves:

A) Borrowing and lending in domestic and foreign currencies

B) Speculating on exchange rate movements

C) Buying stocks in foreign companies

D) Entering into a cross-currency swap

Ans: A) Borrowing and lending in domestic and foreign currencies

Q3: Which of the following describes a natural hedge?

A) Using financial derivatives to manage risk

B) Holding assets and liabilities in the same foreign currency

C) Purchasing options to offset currency risk

D) Speculating on exchange rate movements

Ans: B) Holding assets and liabilities in the same foreign currency

Q4: If a US-based company has a payable obligation in GBP, what is the best way to hedge against an appreciation of GBP?

A) Buy GBP forward contracts

B) Sell GBP futures contracts

C) Buy GBP options

D) Take a long position in a currency swap

Ans: A) Buy GBP forward contracts

Q5: When a company uses a forward contract to hedge currency risk, it:

A) Locks in an exchange rate for a future transaction

B) Benefits from favourable exchange rate movements

C) Buys foreign currency at the spot rate

D) Must physically deliver the currency

Ans: A) Locks in an exchange rate for a future transaction

Relevance to CFA Syllabus

The CFA curriculum covers currency exchange hedging under Portfolio Management and Derivatives. CFA candidates learn about the impact of currency fluctuations on investments and financial statements and various hedging techniques, such as futures, options, and swaps, to manage foreign exchange exposure.

Currency Exchange Hedging CFA Questions

Q1: A portfolio manager expects the USD to weaken against the EUR. Which strategy should they use to hedge this exposure?

A) Buy EUR forward contracts

B) Sell EUR call options

C) Take a short position in EUR futures

D) Purchase USD call options

Ans: A) Buy EUR forward contracts

Q2: What is the primary risk associated with currency futures contracts?

A) Credit risk

B) Market risk

C) Liquidity risk

D) Counterparty risk

Ans: B) Market risk

Q3: Which of the following best describes a cross-currency swap?

A) An agreement to exchange principal and interest payments in different currencies

B) A speculative strategy in the foreign exchange market

C) The process of buying and selling the same currency at different times

D) The simultaneous buying and selling of a currency to take advantage of price differences

Ans: A) An agreement to exchange principal and interest payments in different currencies

Q4: If an investor wants to hedge against currency risk but retain upside potential, which derivative should they use?

A) Forward contract

B) Currency swap

C) Currency option

D) Money market hedge

Ans: C) Currency option

Q5: How does a multinational company hedge translation risk?

A) By adjusting operating cash flows

B) By using forward contracts on expected foreign currency transactions

C) By matching assets and liabilities in the same currency

D) By investing in diversified international portfolios

Ans: C) By matching assets and liabilities in the same currency

Relevance to US CPA Syllabus

The US CPA syllabus covers foreign exchange risk under Financial Accounting and Reporting (FAR) and Business Environment & Concepts (BEC). Candidates must understand foreign currency transactions, hedging strategies, and accounting for derivatives under US GAAP and IFRS.

Currency Exchange Hedging US CPA Questions

Q1: Under US GAAP, how are unrealised foreign currency translation gains or losses reported?

A) As part of net income

B) As an adjustment to retained earnings

C) As part of other comprehensive income (OCI)

D) As a direct adjustment to cash flows

Ans: C) As part of other comprehensive income (OCI)

Q2: If a US-based company wants to hedge against a foreign currency payable due in six months, it should:

A) Buy a currency call option

B) Sell a currency futures contract

C) Buy a forward contract on the foreign currency

D) Purchase shares in a foreign exchange-traded fund (ETF)

Ans: C) Buy a forward contract on the foreign currency

Q3: Under hedge accounting, when a derivative is designated as a cash flow hedge, changes in its fair value are reported in:

A) Retained earnings

B) Net income

C) Other comprehensive income (OCI)

D) Deferred tax liabilities

Ans: C) Other comprehensive income (OCI)

Q4: Which of the following is NOT a financial hedge against currency risk?

A) Forward contract

B) Currency swap

C) Leading and lagging

D) Currency option

Ans: C) Leading and lagging

Q5: If a US company expects to receive payments in EUR and is concerned about EUR depreciation, it should:

A) Buy EUR put options

B) Buy EUR futures contracts

C) Sell EUR forward contracts

D) Take a long position in a cross-currency swap

Ans: A) Buy EUR put options