All activities in a business require financial resource input for their execution. Short-term funds management is more known as working capital management. It ensures the company has enough finances to pay its expenses and invest in growth. Specific factors affecting working capital management include the nature of the business, credit policies, inventory management, and economic aspects. These will determine how much working capital a business requires.

Working capital comprises cash, receivables, inventory minus payables, and other liabilities. These heads ensure that a business runs smoothly and stays financially stable. Poor working capital management can lead to either a cash shortage or the other extreme of excessive funds, making the business unproductive and potentially inefficient.

Define Working Capital Management

Working capital management involves the policies and decisions applied to effectively control a company’s short-term assets and liability. This consists of managing cash, inventories, receivables, and payables. Maintain sufficient cash flow and avoid financial troubles.

A working capital is Working capital=Current assets-current liabilities. Proper working capital management ensures the availability of required finances to meet the short-term expenditures of a company while preventing excess finances from remaining inactive. A business should always look to maximize working capital so that profitability and efficiency are augmented.

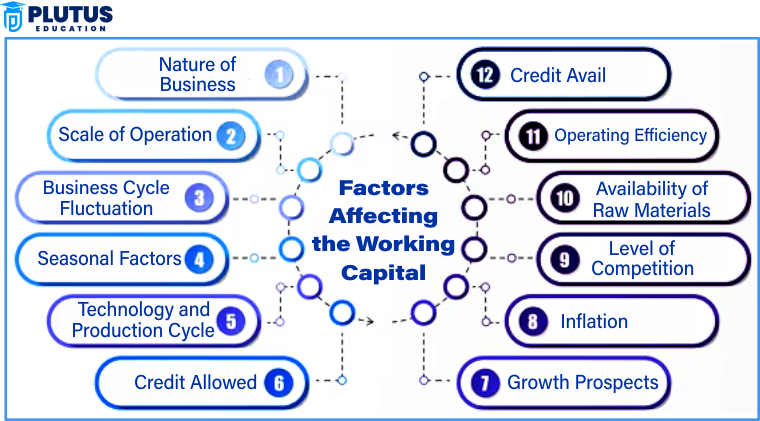

Factors Affecting Working Capital Management

Companies should thoroughly analyse their financial requirements and prevailing external market conditions to manage their working capital best. There are many factors determining the amount of working capital a business requires;

Nature of Business

A business, by its nature, has differing working capital requirements. While manufacturing companies need more capital to stock their raw materials and inventory, service-oriented companies spend most of that capital on human resources.

- A retail business feeds on high working capital to maintain its inventory stock.

- A software company would need little because it has physical assets.

- One must generally analyse the nature of the business and project the relevant working capital levels.

Size of Business

Usually, more prominent companies cash in on extensive resources to run their corporations. However, small companies can operate with low capital. The rate at which a company is developing and the geographic area of market outreach influence the working capital requirements of a company.

- A large corporation can have very high working capital to keep afloat its supply chains.

- A small-scale business would require very little since operations would be much limited.

Operating Cycle

The operating cycle is defined by the conversion period of raw materials into finished products and their eventual sale. This increases working capital requirements since it is time-consuming.

- They have a short cycle and, in that case, lower working capital requirements.

- The heavy machinery manufacturer has a long cycle, requiring more working capital.

Seasonal Demand

Most businesses have seasonal demand fluctuations, which affect their working capital requirements. Thus, the company has to plan appropriately.

- A toy company usually works on higher working capital before a festive season.

- An umbrella manufacturer would require more funds before the season of rain.

Credit Policy

A company’s credit policy will influence the credit status of the company. A policy that is liberal in its credit provision will enable the company to maximise sales, but its inflow of cash will take a longer time. Therefore, higher capital will be required. Cash flow is better in a restrictive credit policy, but sales can dwindle.

Inventory Management

Volumes of inventory affect working capital. High inventory levels mean a higher capitalization requirement. An insufficient number of inventories may cause a halt in production activities.

- JIT minimizes capital needed in inventory keeping.

- Capital requirements grow in the traditional inventory system.

Inflation and Economic Conditions

Demand for working capital increases due to rising inflation due to raw material costs, wages, and overheads. Devaluation of the economy is sure to lower sales and may affect the cash inflow. Working capital is affected by government regulation, tax, and duties. Reduction in cash due to high tax rates is nonexistent. Changes in government policies may also hamper business operations.

Importance of Working Capital Management

The importance of working capital management can never be overemphasised. It is critical to the financial health of a business. Companies with a decent working capital management system can avoid financial trouble and remain positive export houses.

Smoothen Business Operations

For any business, cash is one of the main requirements for handling day-to-day expenses, such as salaries, rent, and raw materials. Proper working capital management ensures adequate cash flow to meet these daily expenses without disruption.

Working capital management helps maintain the cash flow at a level that allows the organization to honor its obligations regarding the payment of suppliers, labour, and debts.

Maximum Profitability

With effective working capital management, the organization will maximize its resources’ utilization, preventing unnecessary costs and ensuring that one has spent every penny correctly. This translates into more significant profits and sustainable growth.

Increased Credibility

Companies can pay their debts on time because efficient working capital management improves their creditworthiness; thus, they can borrow funds and attract investors.

Objectives of Working Capital Management

The major objectives of working capital management include stabilizing liquidity, maximization of manoeuvrability, and profit creation. Let us discuss the main goals in detail.

- Liquidity Maintenance: The consensus is that a business should maintain liquidity for its obligations. Working capital management arrives at the timely intervention of liquidity in defraying its operational expenses and obligations.

- Profitability Maximization: Working capital will thereby have continued inefficient operations at the lowest associated costs while profit generation will be enhanced. A company will attempt to balance holding liquid assets and investing in more revenue-generating operations or projects.

- Financial Stability: It is one of the signs of a financially stable company that can withstand economic downturns. Therefore, the company ensures stability against business depressions through proper working capital management.

- Minimization of Financial Risks: Poor working capital management creates a financial risk of being insolvent or unable to pay its creditors. The greater the working capital, the lesser the risks involved.

- Enrichment of Operational Efficiency: Enhanced cash flow grants credit facilities, leading to operational effectiveness over improved accounts receivable and inventory management. This, in general, translates into improved productivity and growth.

Types of Working Capital Management

Working Capital Management varies, and the above-discussed types can change from business needs to financial policy strategies.

- Permanent Working Capital: This is the bare minimum amount of working capital a firm will be required to maintain all operations. This will involve the basic overhead costs that the company must confront every month, such as salaries, rent, utilities, etc.

- Temporary Working Capital: Temporary working capital must be maintained to meet seasonal or short-term demands. It keeps changing according to the business activity or even the market conditions.

- Gross Working Capital: Gross working capital refers to all current assets available for a corporation, that is, cash, accounts receivable, and inventory.

- Net Working Capital: Net working capital equals current assets minus current liabilities. This gives an idea of the company’s ability to satisfy short-term obligations.

- Positive and Negative Working Capital: Positive Working Capital: When current assets exceed current liabilities, this state is termed good for the company. Negative Working Capital is if the current liabilities exceed current assets, it indicates that the company may soon face financial turbulence.

Relevance to ACCA Syllabus

Working capital management is a crucial aspect of financial management under the ACCA syllabus. It ensures that businesses maintain adequate cash flow for daily operations while optimising liquidity and profitability. The ACCA covers cash management, credit policies, inventory control, and short-term financing as part of the Financial Management and Advanced Financial Management papers.

Factors Affecting Working Capital Management ACCA Questions

- What is the primary objective of working capital management?

A) Maximizing profitability

B) Ensuring liquidity and operational efficiency

C) Minimizing tax liabilities

D) Reducing long-term debt

Ans: B) Ensuring liquidity and operational efficiency - Which of the following is NOT a component of working capital?

A) Accounts Payable

B) Accounts Receivable

C) Long-term Debt

D) Inventory

Ans: C) Long-term Debt - Which financial ratio is commonly used to assess a company’s liquidity?

A) Debt-to-Equity Ratio

B) Return on Assets

C) Current Ratio

D) Earnings per Share

Ans: C) Current Ratio - A company with a high working capital turnover ratio indicates:

A) Inefficient use of assets

B) Overcapitalization

C) Efficient working capital management

D) High financial leverage

Ans: C) Efficient working capital management - Which of the following policies would improve a company’s cash conversion cycle?

A) Increasing the credit period offered to customers

B) Delaying supplier payments as long as possible

C) Holding higher inventory levels

D) Reducing accounts payable turnover

Ans: B) Delaying supplier payments as long as possible

Relevance to US CMA Syllabus

The Certified Management Accountant (CMA) syllabus includes working capital management as part of Financial Decision Making. CMA topics emphasise cash flow optimization, short-term financing, and efficiently managing receivables, inventory, and payables.

Factors Affecting Working Capital Management US CMA Questions

- Which of the following is a measure of short-term liquidity?

A) Acid-Test Ratio

B) Price-to-Earnings Ratio

C) Dividend Payout Ratio

D) Return on Investment

Ans: A) Acid-Test Ratio - Which factor is most likely to reduce a firm’s cash conversion cycle?

A) Extending customer credit terms

B) Reducing inventory turnover

C) Negotiating longer payment terms with suppliers

D) Increasing accounts receivable days

Ans: C) Negotiating longer payment terms with suppliers - A company that maintains a large cash balance may suffer from:

A) High profitability

B) High liquidity risk

C) Lower return on assets

D) Reduced creditworthiness

Ans: C) Lower return on assets - Which of the following best describes a conservative working capital policy?

A) Using short-term financing to fund long-term assets

B) Maintaining high levels of current assets

C) Keeping low inventory levels to minimize costs

D) Relying on just-in-time (JIT) inventory management

Ans: B) Maintaining high levels of current assets - Which of the following is a key advantage of just-in-time (JIT) inventory management?

A) Higher holding costs

B) Reduced carrying costs

C) Increased working capital requirements

D) Greater risk of stockouts

Ans: B) Reduced carrying costs

Relevance to CFA Syllabus

The CFA curriculum includes working capital management under Corporate Finance. It emphasizes the impact of working capital decisions on a firm’s financial health, efficiency, and shareholder value.

Factors Affecting Working Capital Management CFA Questions

- Which of the following is an example of aggressive working capital management?

A) Holding minimal cash reserves

B) Extending customer credit terms generously

C) Maintaining excess inventory to avoid stockouts

D) Relying on long-term financing for short-term needs

Ans: A) Holding minimal cash reserves - Which component is NOT part of net working capital?

A) Accounts Receivable

B) Inventory

C) Accounts Payable

D) Fixed Assets

Ans: D) Fixed Assets - Which financing strategy is most suitable for seasonal businesses?

A) Aggressive financing strategy

B) Conservative financing strategy

C) Matching (hedging) financing strategy

D) Just-in-time financing strategy

Ans: C) Matching (hedging) financing strategy - A company with a negative cash conversion cycle:

A) Faces high liquidity risk

B) Collects cash from customers before paying suppliers

C) Requires higher working capital investment

D) Needs long-term financing for short-term needs

Ans: B) Collects cash from customers before paying suppliers - Which of the following policies would likely increase a company’s working capital?

A) Offering discounts for early customer payments

B) Reducing credit terms for customers

C) Increasing inventory turnover

D) Extending payment terms to suppliers

Ans: B) Reducing credit terms for customers

Relevance to US CPA Syllabus

The US CPA covers working capital management under Financial Management and Business Environment & Concepts (BEC). It optimises liquidity, cash flow, and managing current assets and liabilities efficiently.

Factors Affecting Working Capital Management US CPA Questions

- Which of the following best defines working capital?

A) Current Assets – Current Liabilities

B) Total Assets – Total Liabilities

C) Fixed Assets – Current Liabilities

D) Cash + Accounts Payable

Ans: A) Current Assets – Current Liabilities - An increase in accounts receivable turnover generally indicates:

A) Improved cash flow management

B) Increased risk of bad debts

C) Reduced sales volume

D) Higher credit period offered to customers

Ans: A) Improved cash flow management - Which financing source is most commonly used for working capital needs?

A) Equity issuance

B) Long-term bonds

C) Short-term bank loans

D) Retained earnings

Ans: C) Short-term bank loans - A company following a conservative working capital policy is likely to:

A) Have high liquidity but lower profitability

B) Reduce cash reserves to maximize investment

C) Maintain minimal inventory levels

D) Use short-term financing to fund fixed assets

Ans: A) Have high liquidity but lower profitability - Which of the following is a key disadvantage of aggressive working capital management?

A) Increased cash reserves

B) Reduced financial risk

C) Higher risk of liquidity shortages

D) Lower return on investment

Ans: C) Higher risk of liquidity shortages