The internal rate of return formula is one of the primary financial calculations applied to investment analysis and capital budgeting. The internal rate of return formula determines the profitability of prospective investments by finding out the discount rate at which the NPV of all cash flows becomes zero. Since this knowledge regarding the internal rate of return formula would mean making an informed investment decision, a business uses it to see if an investment is worthwhile and compare the available investment opportunities. An internal rate of return formula calculates the returns breaking even for an investment. The formula for the Internal Rate of Return is given by submission of cash inflow divided by the internal return rate in addition to one to the power of the period.

When the internal rate of return exceeds the minimum required rate of return, the project will be taken as economically viable. Internal rate of return assists in better investment choices for management by comparing investment returns. It is commonly used in corporate finance, private equity, and venture capital to assess new projects.

What is Internal Rate of Return?

The IRR refers to the discount amount that makes a project’s net present value equal to zero. The IRR expresses the expected annual return for an investment. This is a significant measure in capital budgeting, often used for comparing the profitability of alternative projects.

The IRR helps firms evaluate whether an investment would result in positive returns. The higher the IRR, the more valuable the project; the lower the IRR, the less attractive the investment. IRR is then determined against a required return to decide whether to accept or reject a project. The project may be accepted if the IRR exceeds the capital costs.

However, IRR has some disadvantages that make it inadequate. It does not factor in size, length of execution, or susceptibility to external danger. It also assumes that reinvestment occurs at IRR, which is often unacceptable. All these factors continue to create problems for investment analysis with IRR.

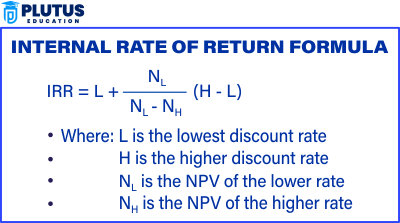

Internal Rate of Return Formula

The internal rate of return formula defines the discount rate that sets cash flows’ net present value (NPV) to zero. The IRR formula is:

With the above formula, cash flow from an investment is thus internally compared. Since analytically solving for IRR is impossible, solving the IRR equation requires either trial and error or a software tool.

Assumptions of Internal Rate of Return Formula

The IRR formula has several assumptions underlying it. These assumptions can generate this metric into an untrustworthy investment analysis standard. These assumptions further reveal the inadequacies of IRR and show why businesses should look at other evaluative measures, such as net present value (NPV), in evaluating their future investments.

- Reinvestment at IRR: The IRR method assumes that future cash flows are reinvested at the calculated IRR. This assumption is often unrealistic since businesses reinvest at the cost of capital.

- Stable Discount Rate: While it is true that IRR assumes the discount rate remains stable over the entire lifetime of a project, in reality, interest rates fluctuate and significantly affect investment returns.

- Positive Cash Flows: The formula assumes that cash flows will always be positive after the initial investment; however, many projects experience negative cash flows in some years.

- Singularity of IRR Value: The method assumes only one IRR value exists. Nonetheless, projects experiencing unconventional cash flows may possess more than one IRR, rendering such projects very hard to evaluate.

- Equal Time Frame of Comparison for Projects: IRR does not recognize the time difference when assessing two real or hypothetical projects. As a result, the comparison appears to be misleading.

Internal Rate of Return Example

Suppose ABC Ltd has an initial outflow of cash as 15 lakh and further inflows as the following. To calculate the IRR, one has to use the formula of hit and trial as

0 = [inflows/(1+r)^t]+ [inflow/(1+r)^t]+ ……. nth^t

| Year | Cash Flow (INR) |

| 0 | -15,00,000 |

| 1 | 4,00,000 |

| 2 | 5,00,000 |

| 3 | 6,00,000 |

| 4 | 7,00,000 |

Using the internal rate of return formula, the IRR is computed to be approximately 14.89%.

Advantages of Internal Rate of Return

Despite the disadvantages, there are several advantages to IRR. It is most commonly used in capital budgeting because it is a relatively easy way to evaluate the return on investment. The five main advantages are as follows:

- Easy to interpret: IRR expresses profitability in percentage terms, an easily understood scale for investors to make relative comparisons across projects.

- Time value of Money: IRR accounts for the time value of money and applies proper discounting for future cash flows.

- Useful for Capital Budgeting: IRR aids capital budgeting decisions by contemplating a project’s immediate future viability.

- Independent of Project Size: Other measures require project size information, while IRR can compare projects of any size without such knowledge.

- Considers the cash flow timing: The IRR considers timing regarding cash flows, which is the basis of project evaluation.

Limitations of Internal Rate of Return

The IRR can be accepted as the basis for one more investment decision; nevertheless, it has certain limitations that reduce its reliability. Out of the eight limitations listed below, those are the most notable.

Multiple IRRs

A project with unconventional cash flows may have several IRRs, thus creating difficulties in understanding and selecting the effective rate of return, further confusing the investment decision. A project with alternating cash inflows and outflows has other corresponding discount rates that will satisfy the equation, i.e., NPV = 0, thus creating ambiguities.

Assumes Reinvestment at IRR

The IRR method assumes all future cash flows are reinvested at the IRR. In practice, firms reinvest at their cost of capital, which is invariably less than the IRR. Such false assumptions inflate the estimated returns for decision-making purposes.

Ignores Project Size

Internal Rate of Return does not consider the absolute project size. A smaller investment with a higher IRR may not generate as much profit as a bigger one with a lower IRR. Hence, some other kind of project evaluation parameter/financial metrics must be used to compare among projects effectively.

Difficult for Mutually Exclusive Projects

IRR can produce misleading results when compared to mutually exclusive projects. Thus, it would favor quick returns on a brief duration over long-term sustainable cash flow investments. External risks such as market conditions, inflation, and changes in interest rates have no bearing on the IRR, which tends to be an unreliable indicator on its own.

Net Present Value vs Internal Rate of Return: Key Differences

Both net present value (NPV) and internal rate of return (IRR) are among the most popular capital budgeting methods. Although these methods evaluate possibilities in project profitability, their surrounding techniques and interpretations differ. NPV measures value in absolute dollars added by investment instead of an IRR, which expresses return as a percentage. Therefore, the choice between NPV and IRR depends on the project size, cash flow patterns, and the cost of capital.

| Feature | Net Present Value (NPV) | Internal Rate of Return (IRR) |

| Definition | Calculates the difference between the present value of cash inflows and outflows | Determines the discount rate where NPV equals zero |

| Measurement | Expressed in absolute monetary terms | Expressed as a percentage |

| Decision Rule | Accept if NPV > 0 | Accept if IRR > required rate of return |

| Consideration of Cost of Capital | Explicitly considers the cost of capital | Assumes reinvestment at IRR |

| Handling of Multiple Projects | Works well for mutually exclusive projects | It may give misleading results for mutually exclusive projects |

| Complexity | Requires setting an appropriate discount rate | May have multiple IRRs in complex cash flows |

| Suitability | Better for large-scale investments with varying cash flows | Helpful in comparing projects of similar size and risk. |

Internal rate of Return Formula FAQs

1. What are the advantages of the internal rate of return in capital budgeting?

The internal rate of return is a metric that helps a firm decide on either accepting or rejecting the project. Regarding capital investment, when an IRR is above the cost of capital, it would indicate a profitable venture.

2. What is the difference between NPV vs IRR?

The IRR formula is different from NPV’s as in the former; the discount rate is found such that NPV equals zero, while the latter does a straightforward calculation of the profitability of a project by finding the difference between the initial investment cost and the present value of all cash flows.

3. What are the most important restrictions internal rate of return?

The limitations are multiple internal rate of return calculations, assumptions for reinvestment, and comparison of projects with unequal investment values.

4. Why is IRR important investment decision?

Comparative analysis of expected returns with the cost of capital will facilitate IRR in choosing the most feasible investments with the most attractive market value.

5. Is it possible for the IRR to be negative?

The IRR can be negative if the cash inflows produced from the project underestimate the initial investment, indicating that the project is a loser investment.