The internal sources of finance refer to the funds a business generates from within its operations to meet its financial needs. Unlike external sources, internal finance does not involve borrowing or raising capital from outside the organization. Instead, businesses utilize profits, savings, or existing resources to fund their activities. To achieve sustainable growth, businesses should balance internal and external finance options while managing resources efficiently. These sources are essential for maintaining financial independence and ensuring stability in both day-to-day operations and long-term projects.

What is Internal Sources of Finance?

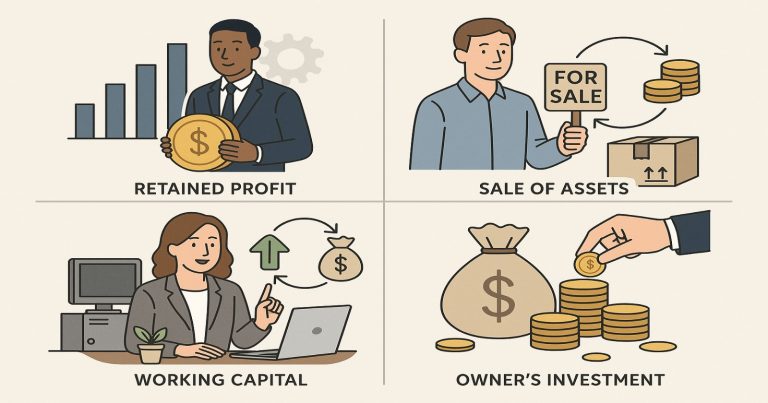

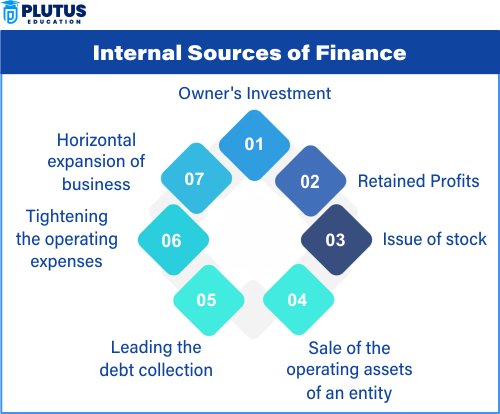

Internal sources of finance are funds that businesses derive from their resources to meet financial requirements. These sources do not rely on external lenders or investors, ensuring that businesses maintain complete control over their finances. Common internal finance sources include retained earnings, sale of assets, and working capital.

Importance of Internal Sources of Finance

Internal sources of finance play a key role in helping businesses manage funds effectively. They provide a cost-effective and sustainable way to support growth without relying on external borrowing.

- Financial Independence: Internal finance eliminates the need for external borrowing, reducing dependency on lenders.

- Cost Efficiency: Since businesses use their resources, they avoid interest payments or loan repayment obligations.

- Sustainability: Internal finance ensures the company can reinvest profits or resources, enabling stable growth over time.

Internal Sources of Finance

The internal sources of finance provide businesses with the flexibility and autonomy to fund their activities. However, they also come with limitations. Understanding the advantages and disadvantages of each source helps businesses make informed decisions.

Retained Earnings

Retained earnings refer to the portion of profits a business saves rather than distributing as dividends. Companies reinvest these funds to expand operations, purchase equipment, or develop new products.

Advantages of Retained Earnings

- Cost-Effective: No interest or repayment obligations.

- Encourages Growth: Funds can be reinvested to boost operations or enter new markets.

- Strengthens Financial Position: Retained earnings improve the company’s reserves, ensuring stability during downturns.

Disadvantages of Retained Earnings

- Limited Availability: Depends on the company’s profitability.

- Opportunity Cost: Funds used for reinvestment cannot be distributed as dividends, potentially dissatisfying shareholders.

- Risk of Over-Reliance: Solely depending on retained earnings may limit growth opportunities.

Sale of Assets

Businesses can sell unused or non-core assets, such as old equipment, vehicles, or properties, to generate funds. This is a quick way to access finance without incurring debt.

Advantages of Sale of Assets

- Immediate Cash Flow: Provides quick access to funds.

- Optimizes Resource Use: Converts idle assets into productive financial resources.

- No Interest or Repayment: Selling assets eliminates the burden of loans or interest payments.

Disadvantages of Sale of Assets

- Loss of Assets: Reduces the company’s resources, which may impact future operations.

- Limited Amount: Funds raised depend on the value of assets sold.

- One-Time Solution: Selling assets does not provide a recurring source of finance.

Working Capital

Working capital refers to the difference between current assets (like cash and receivables) and current liabilities (like accounts payable). Businesses can optimize their working capital to meet short-term financial needs.

Advantages of Working Capital

- Improves Liquidity: Frees up funds for immediate expenses.

- No Additional Costs: Uses existing resources without incurring debt.

- Promotes Efficiency: Encourages better management of inventory and receivables.

Disadvantages of Working Capital

- Short-Term Focus: Funds are limited to covering day-to-day operations.

- Risk of Over-Extension: Mismanagement can lead to cash shortages.

- Reduced Operational Flexibility: Excessive reliance may limit funds for other areas.

Depreciation Savings

Depreciation is a non-cash expense that reduces the book value of assets over time. Businesses often allocate funds equivalent to depreciation as savings, which they can use for reinvestment.

Advantages of Depreciation Savings

- Cost-Free: Utilizes existing resources without requiring external funds.

- Supports Asset Replacement: Ensures funds are available to replace outdated equipment.

- Reduces Tax Liability: Depreciation lowers taxable income, indirectly saving money.

Disadvantages of Depreciation Savings

- Limited Availability: Savings depend on the depreciation value of assets.

- Not a Standalone Solution: Insufficient for significant investments.

- Requires Proper Management: Businesses must allocate savings wisely to avoid misuse.

Internal Sources of Finance FAQs

What are internal sources of finance?

Internal sources of finance are funds generated within a business, such as retained earnings, sale of assets, or working capital, used to meet financial needs.

Why are internal sources of finance important?

They reduce reliance on external borrowing, lower costs, and provide financial independence, enabling businesses to manage their resources efficiently.

What is an example of internal finance?

Retained earnings, which are profits saved and reinvested into the business, are a common example of internal finance.

What are the disadvantages of selling assets as a source of finance?

Selling assets may reduce a company’s resources, limit future operational capacity, and is only a one-time solution.

Can internal finance support long-term growth?

Internal finance can support long-term growth if managed efficiently, but businesses may need to combine it with external sources for larger projects.