Intimidation threats occur when an individual is under pressure—under fear or coercion, compromising their ability to act objectively. Intimidation threats can occur in many areas, including auditing, accounting, and business ethics. An intimidation threat to independence is a serious concern in these professional domains. Wherein the ensuing environment of integrity and impartial decision-making is paramount.

An intimidation threat in self-governance will occur when an auditor feels pressured. Either by one or more of the clients. Also, from an employer or overriding authority. It is to modify their work and/or ethical standards. Thus, these threats could and will deprive the auditor of the independence and ability to assess objectively. For example, if an auditor fears losing his job . Or he is being demoted; such fear would restrain him. He would be restrained from informing the authorities of any financial irregularities.

We need to understand what a threat of intimidation is. Also how it affects professional judgment. Organizations should implement a buttressing structure. It is to prevent such threats and resist the temptation of laying aside ethics. The article will thus define the intimidation threat and explain how it works, the ethics behind it, examples, and safeguards.

What is Intimidation Threat?

A person can be said to be under an intimidation threat when some pressure or coercion exists. This can adversely affect his capacity to make an unbiased decision. In situations like these, intimidation threats are prevalent in professional settings when individuals are subjected to influence by senior authorities, clients, or colleagues.

Intimidation Threat in Auditing and Accounting

In auditing and accounting, an intimidation threat is the risk that an auditor’s independence may be compromised. This is due to fear of consequences. If auditors believe they will suffer retaliation for reporting errors, they may not disclose financial misstatements, weakening the reliability of the financial statements and damaging public trust in financial reporting.

Intimidation threats also extend to accountants preparing financial statements. An accountant might feel compelled to manipulate financial information under intense pressure from senior management. Such behaviors can constitute financial fraud and invite criminal prosecution.

Impact on Professional Independence

An intimidation threat directly affects an individual’s independence. The threat of intimidation is an issue of great concern in professions where impartiality is of utmost essence. Auditors, accountants, and financial analysts should be able to reach independent judgments. It should be free from the fear of retaliation. When one feels threatened by intimidation, one’s professional scepticism and objectivity will be compromised.

Therefore, organizations should take the birth of the intimidation threat. It should institute measures to protect employees from undue influence. Maintaining this understanding is very vital for safeguarding ethical professionalism.

How Does Intimidation Threats Work?

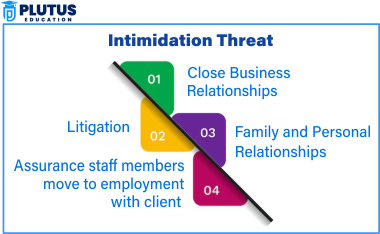

The intimidation threat determines decision-making and performance in an environment drenched with fear. If individuals fear the repercussions of adverse decisions, they tend to avoid acting ethically. The intimidation threat can either be direct or indirect in worksites. Types of intimidation include:

Direct Threat

Employees are directly warned regarding their job security, promotion, or reduction in salary. Employees are told by their immediate heads that their non-compliance will cost them their jobs. Promotions/salary increments are issued as carrots for employees to obey unethical requests. Sometimes, employees are told that any negative performance evaluations will follow unless they do what they have been instructed. Officials would hint at an indirect threat to their careers should any whistle-blower come up against unethical behavior. People may have references blocked, limiting future job prospects in selected industries.

Indirect Pressure

Employers or clients will be less direct in proposing that unfavorable decisions may result in negative consequences. At times, and often, managers have used ‘backdoor’ communication to suggest that non-compliance may harm an employee’s future growth. Employees may thus be marginalized when participating in essential projects or professional growth opportunities. Implicitly, the expectation may arise to follow unethical practices without an overt command. Professionals who resist intimidation may also consequently be subjected to scrutiny or micromanagement. It will be as if there was never really a threat, to begin with, and failure to speak up will seem unnecessary or even detrimental.

Harassment from Co-workers

Providing a work environment that condones unethical behavior means that employees in that work environment always feel pressured to do the wrong thing. Unethical behavior in the workplace is an environment that puts constant pressure on employees to “go along. Co-workers become the ones who’d shun others who would resist being intimidated or give them worthless jobs. Even third parties might be implicated while evaluating the ethical conduct of employees. Such reports would threaten the moral choices of these employees. Unethical behavior within the workplace creates a hostile environment characterized by low productivity and trust among its staff. In an intimidation-threat audit, fearing that reporting financial irregularities would result in conflict with clients or superiors puts pressure on auditors to lower the quality of their professional judgment.

Effects on Decision-Making

Many effects of threat in intimidation on decision-making are as follows:

Reduces objectivity in job security over tops ethical standards for employees. Employees turn blind eyes to ethics regarding decisions based on self-preservation. Financial stability has a weightier account besides reporting the wrongdoing. Counselling dilemmas tighten in the navigation under job security threats. Some of the employees consider their unethical behavior to be necessary for their very survival. Objectivity swings downwards, and the employees may justify their rationale gradually. Conform to unethical requests- Employees agree with the orders even when not within professional ethics.

Fear Losing Benefits

Bonuses or promotions, hence showing compliance. Some employees comply with open unethical orders because they favor the belief that there will not be a change in the end from resistance. This silence creates a culture in which employees will avoid discussing unethical activities. People will feel powerless and assume that speaking out will be futile. Some professionals think unethical decisions are not their responsibility because they follow orders.

Creates a culture of silence- Fear prevents employees from being exposed to fraud or misconduct.

Demotion or Forced Resignation.

Employees are branded as troublemakers for reporting activities that violate ethics. Usually, the whistleblower experiences demotion or forced resignation. Isolation and retaliation discourage employees from speaking up. In some sectors, silence about misconduct is assumed to be the norm; hence, changing unethical practices becomes detrimental to progress. Along the way, an organization with a culture of silence is deemed to lose credibility and face reputational damage. Understanding how the intimidation threat operates helps professionals identify and mitigate its impact. Organizations must implement safeguards to ensure employees can act without fear.

How to Safeguard Against Intimidation Threats?

The safeguards against intimidation threats help professionals maintain their independence and uphold ethics in decision-making. Organizations or regulatory bodies should develop and implement strong and well-researched policies prohibiting undue influence. Policies and regulations to prevent the intimidation threat. Professional accounting bodies have laid down ethical guidelines to curb intimidation concerning audits. These are some safeguards for the intimidation threat:

Regulatory Frameworks

Ethics codes would be established for auditors to follow when resisting pressures. Such provisions are derived from professional bodies like the International Federation of Accountants (IFAC). Governments have strict policies that block unethical financial reporting.

Auditors keep documents as working papers to justify anything decided in an audit process.

Regulatory authorities review documents and conduct investigations to ensure consistent transparency. Any code of ethics contravened brings legal and professional repercussions.

Protection for Whistleblowers

Employees who expose unethical practices should be protected from victimization. Many countries have incorporated legislation that shields whistleblowers from dismissal and punishment. Anonymous reporting systems enable employees to report unethical practices confidentially. Independent committees should be constituted within organizations to handle cases of whistleblowers. Protection laws safeguard the whistleblower from being targeted without merit. Following misconduct reporting, legal support must be provided to employees subjected to retaliatory behavior.

Training Programs

Educating professionals about intimidation threatens awareness. Companies must train employees to recognize the intimidation tactics used against them. Awareness campaigns emphasize the influence of ethical and unethical behavior on the workplace environment. Employees learn ways to respond to intimidation threats. Such trainings encourage a culture of integrity and moral responsibility. Regular workshops catch up with the reinforcement of ethical standards within the organizations. These measures ensure that professionals can make objective decisions without fear of consequences.

Intimidation Threat Ethics

These threats of intimidation have ethical dimensions, especially in professions with an absolute need for integrity. He gives an ethical indication of the paths people may go concerning intimidation. Ethical principles against intimidation threat. Professional organizations have outlined moral guiding principles that experts should embrace to counter intimidation:

- Integrity-Professional has to be honest regardless of external pressure acceptance.

- Objectivity– One should always make an unbiased decision despite external pressures.

- Professional scepticism– The professional must interrogate and then evidence or document all the information to verify its accuracy.

Real Ethical Dilemmas

These dilemmas arise when competing interests confront a professional. Dilemmas of this nature are well highlighted when the internal audit finds intimidation threats making a cash misstatement since reporting the misstatement could prompt job insecurity. Through the intensity of ethical training, people are equipped to handle these dilemmas well. Preservation of ethical standards is the assurance of transparency and accountability in the work environment.

Intimidation Threat Examples

The above realities illustrate the increase in intimidation threat and its fallout in various industries. Threat of Intimidation in Auditing Their multinational companies pressured External auditors across countries to ignore misstatements in the financial spheres. The external auditors feared losing a big client and hesitated to report the discrepancies. As a result, the multinational corporation suffered fraudulent financial reporting and legal repercussions.

Example in Accounting

In accounting, a finance manager receives an intimidation threat when their manager tells them to change the reports containing financials. If the manager fails to comply, they will face severe consequences in their career. This pressurizes him to decide between ethical integrity and job security. These examples highlight the need for safeguards against threats of intimidation in workplaces.

Intimidation Threat FAQs

1. What does the intimidation threat mean in auditing?

The intimidation threat occurs when the client or employer pressures an auditor to change an honest finding. In this way, the auditor’s independence is compromised, and the quality of financial reporting is jeopardized.

2. How does the intimidation threat affect independence?

An intimidation threat toward independence arises whenever individuals fear potential retaliation for an ethical decision. This pressure actively discourages any outreach toward objectivity and erodes any feeble stature of professional integrity.

3. What are some safeguards for intimidation threats?

Standard safeguards are regulations, ethical training, whistleblower protection, and rigid company policies to resist intimidation and help professionals remain objective.

4. Do intimidation threats occur in internal audits?

An intimidation threat occurs when internal auditors are pressured by management to ignore financial misstatements, which reduces the effectiveness of internal controls.

5. What is an example of an intimidation threat in accounting?

It’s a well-known example of how accountants must tamper with accounting records to meet management expectations. The fear of losing a job discourages the employee from reporting unethical acts.