Financial service leasing is becoming one of the most used ways of financing by private and corporate consumers to use something without owning it. Rather than paying for the asset in full, the user pays the owner, a lessor, for instalments over time. This means of agreement allows businesses to utilise expensive machinery, real estate, or vehicles when they cannot generate enough capital to purchase outright.

Leasing is one of the significant factors in business growth for financial services. The main reasons are that it maintains liquidity, and assets can be replaced/added with ease; additionally, asset deprecation risk is bypassed. The agreement and contract can vary between types of leases, payment structures, and ownership rights. This article provides a detailed understanding of leasing, including its meaning, definition, types, relevance in India, key contents of the lease agreement, and its advantages and disadvantages.

Meaning of Leasing in Financial Services

Leasing is a financial transaction whereby the owner of an asset, known as the lessor, grants to another party, the lessee, the right to use an asset for a specific period in return for periodic payments. The lessor owns the asset, but its benefits are available to the lessee without taking the entire burden of the quintet.

Leasing in financial services helps companies gain access to high-cost assets without affecting the working capital. This method is prevalent in manufacturing, construction, transportation, and technology, where expensive equipment and machinery are needed for operation. Instead of investing a considerable amount upfront, companies opt for leasing to enhance cash flow and financial stability. Leasing is also preferred for assets that require frequent upgrades, such as IT infrastructure and office equipment.

Definition of Leasing in Financial Services

Leasing is defined as a lease contract in which the lessor legally allows a different person – who could thus be called lessee – for some predetermined amount of time the right to utilise an identified asset by paying for instalments; this gives him the right over the assets in question. However, the title shall remain in the lessor: the terms, including the conditions within which this will be used, accompanied by payment schedules, define the Lease Agreement.

Structured financing in financial services allows companies to acquire assets without significant capital investment. This aids in maintaining financial flexibility for companies, reduces tax liabilities, and avoids risks associated with depreciating assets. Lease agreement structures vary according to the asset type, lease duration, and the lessee’s goals as per the institutions and leasing companies.

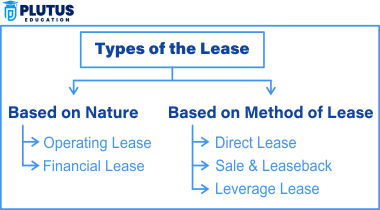

Types of Leasing in Financial Services

Leasing agreements vary, considering the factors that include ownership rights, duration, and financial obligations. The most common types of leasing in financial services include finance leases, operating leases, sale and leaseback, direct leases, leveraged leases, and cross-border leases.

1. Finance Lease

A finance lease is a long-term leasing contract where the lessee bears all the risks and rewards of ownership while paying periodic lease payments. Although the lessor retains ownership, the lessee has to pay for maintenance, insurance, and repairs. This lease is used for heavy machinery, industrial equipment, and vehicles.

It benefits firms that require an asset in the long run but do not want to purchase it at full price. Most of the asset’s life is covered by the lease term, so the company can use the equipment without having the burden of high prices. The lessee may have a right to buy the asset at the nominal value after the lease period has ended.

2. Operating Lease

An operating lease is a short-term one wherein the lessor retains the ownership right, and he bears all the cost of maintaining and repairing the asset. Operating leases are preferred when an asset is needed only for a short period, like renting office space, construction equipment, or a fleet of vehicles for specific project completion.

Since operating leases have no transfer of ownership risk, they are superb for businesses needing flexibility. When the lease ends, companies can turn to the most recent equipment without significant financial loss. The payments of an operating lease are also mentioned in the books and, therefore, are taxable.

3. Sale and Leaseback

In a sale and leaseback arrangement, an asset is sold to a leasing firm, and the company then takes it on a lease for continuing usage. In this way, businesses can unfetter capital from assets while its usage is never interrupted.

For example, instead of a loan, a manufacturing firm could sell its factory premises to a leasing company and lease it back. In this situation, the firm may use the property while simultaneously creating liquidity for expansion or debt repayment.

4. Direct Lease

In direct leasing, the leasing company passes the asset to the lessee without diaries. The application of direct leases is highly acknowledged and popularly used in real estate and equipment leasing. Companies acquire vital assets for their use instead of purchasing them.

The leasing process is streamlined since direct leasing involves fewer pieces of paper and takes less negotiation time. Clear lease terms and fixed schedules make payments more predictable, while the availability of assets over long periods without owning them benefits businesses.

5. Leveraged Lease

A leveraged lease is a multi-party agreement involving the lessor, lessee, and lender. Under a leveraged lease, a lessor raises finance to obtain the asset. The advantage for businesses acquiring high-value equipment or infrastructures is zero or minimum upfront investment.

Majorly, the leased-out leases are practised in industries such as aviation shipping and power generation, which require a lot of assets but can not raise high-value funds internally. Lessees and lessors benefit from tax advantages using the leased-out lease while efficiently using capital.

6. Cross Border Lease

A cross-border lease involves a leasing agreement among parties operating from different countries. Cross-border leases are also mainly used by businesses in global operations, where businesses buy industrial equipment, aircraft, and transportation fleets across borders.

Cross-border leasing in financial services helps multinational companies optimise tax benefits and reduce operational costs. However, it requires compliance with international financial regulations and taxation policies.

Leasing in Financial Services FAQs

1. What is leasing in financial services?

Leasing in financial services is the agreement where an asset is leased to a business or individual for a certain period instead of its purchase. Periodic lease payments are made to the lessor by the lessee while utilising the asset.

2. What are the types of leasing in financial services?

The major types of leasing in financial services are finance lease, operating lease, sale and leaseback, direct lease, leveraged lease, and cross-border lease. Each type serves different business needs.

3. What is the difference between lease and rent?

A lease is a long-term contract, usually for equipment or real estate, while rent is a short-term agreement with flexible terms. Leasing typically includes fixed terms, while rent agreements can change frequently.

4. What is a lease agreement?

A lease agreement is signed between a lessor and a lessee that cites the terms, payment structure, responsibilities, and conditions for leasing an asset.

5. What are the benefits of leasing in financial services?

Leasing has cost-saving benefits, tax advantages, and flexibility, and it removes the risk of depreciation. It can use assets without significant capital investments.