Medium-term sources of finance constitute an important constituent of the whole business framework, which can support stability and growth. The term is defined based on a period of one to five years; hence, the same can be suited for asset financing, expansion purposes, and other working capital requirements. It gives finance to an organization as a short-term bridge or gap till medium-term sources can be devised as an alternative between short and long. Therefore, this paper explores the same term in detail, including all its meaning, types, advantages, and disadvantages, and critically analyses its role in business performance without over-leveraging liabilities on the books of the organization.

Medium Term Sources of Finance Definition

Medium-term sources of finance are loans which between repayment, take durations ranging from one to five years in duration. This is normally applied to fixed assets purchasing, re-tooling or refreshing existing structures, or managing the cycle of working capital. It can be distinguished as not being in the short-term finance category, to be repaid within a shorter period, or in the long-term finance category that spans decades; medium-term finance provides a gap for businesses set on moderate-term goals. Thus, it caters to fill the gap left between short operational needs and longer strategic investments.

It is actually used very often by business enterprises in order to stabilize cash flows while undertaking growth initiatives. It is very highly suitable for projects that require instant funding but are likely to reap returns in a relatively short time span. Such examples include setting up modern machinery, establishing warehouses, or enhancing production facilities. This, therefore, renders medium-term finance an indispensable tool for emerging enterprises.

Sources of Finance

When selecting the right medium-term option, there is a significant need to be aware of different sources of finance. A firm can raise funds through internal sources, external sources, equity, debt, or hybrid instruments. Each source of finance offers some advantages and disadvantages that should complement the financial goals of the business and the business’s operational needs.

1. Equity Finance

Equity finance generates capital by issuing shares of the company. Equity finance is not repayable and does not increase the company’s debt burden. However, it may result in diluted ownership and control. Start-ups and high-growth businesses often rely on equity finance to fund expansion. Unlike debt, equity finance passes some of the risks on to investors, making it an attractive option for ventures that are unsure about cash flow stability over the short term.

2. Debt Finance

Debt financing is raising funds on a promise to return the same along with interest. The most common instruments are loans, debentures, and credit lines. Though ownership is retained, the financial liability increases. Debt finance will be stable and predictable for firms with stable cash flows. Through debt options, firms can even bargain for attractive terms based on their creditworthiness.

3. Hybrid Instruments

Hybrid instruments, for example, convertible debentures, embody characteristics of equity and debt simultaneously. They can be repaid as well as owned by more flexible businesses firms may issue hybrids in order to match their strategic need for risk matching and flexibility. Hybrids are thus attractive both to conservative investors and growth-oriented investors; this makes funding options of businesses flexible. Medium-term finance is either debt or hybrid finance that offers the project with scheduled repayments of the medium-term period.

Types of Medium Term Sources of Finance

The sort of medium-term financing method implemented is dependent upon the financial scenario of the enterprise, its objective, and risk capacity. The important types of finance are as follows:

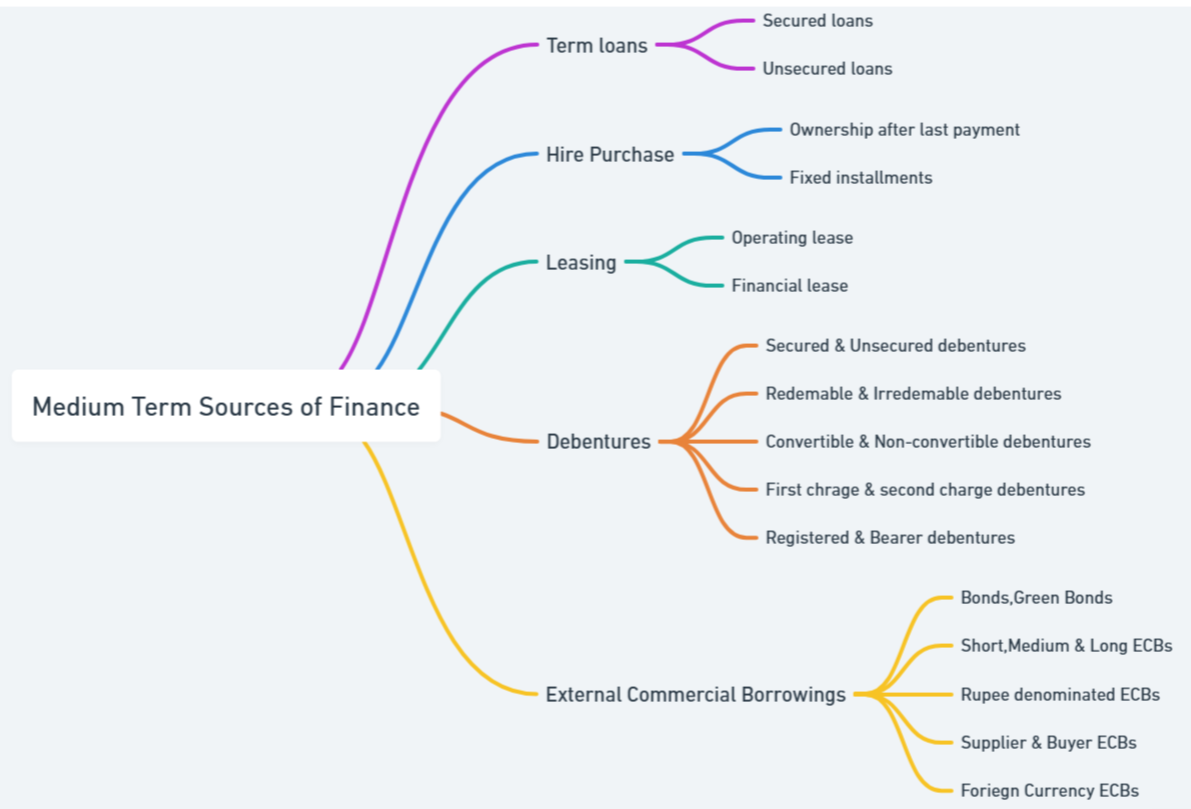

1. Term Loans: Term loans are the most typical form of medium-term loan supplied by commercial banks and finance firms.

- Terms: Fixed rates of interest, fixed-rate repayment cycle

- Uses: Acquisition of machinery, vehicles, or machines.

- These loans normally have fixed-term repayment periods; hence, one can plan according to them.

Businesses can utilize it to fulfill the specific need for funding without sacrificing their liquidity. Term loans may also be so structured to allow the borrower’s repayment capacity without creating an undue burden of the installment.

2. Hire Purchase:

- Definition: This is an agreement whereby the business acquires assets by paying installments while utilizing them.

- Ownership: Ownership only passes on at the final payment installment

- Viability: Small operators who merely hire or lease equipment and, or vehicles but do not hire purchase.

This will give the company the much-needed cash savings to generate cash without using it at the point of purchase. Hiring and purchasing will always be an immediate cash-intensive outlay and often cannot happen together.

3. Leasing: Leasing is an asset used for a specified time against payment of prearranged agreed rentals.

- Leases: There are two broad categories of leases – operating and finance.

- Operating Lease: Short-term, where ownership remains with the lessor.

- Finance Lease: Long-term, often leading to asset ownership.

- Advantages: Initial cost is less than outright purchase.

Leasing contracts offer flexibility in operations, especially for firms expecting technology upgradation. Businesses can avoid asset obsolescence risks while reaping the benefits of lower initial costs.

4. Debentures

- Definition: A type of debt security offered by companies to investors, which carries a fixed rate of interest.

- The different types of Debentures are listed below

- Secured Debentures: Backed by specific assets as collateral.

- Unsecured Debentures: Not backed by any collateral; relies on issuer’s credibility.

- Redeemable Debentures: Repaid after a fixed period.

- Irredeemable Debentures: No fixed maturity, remain outstanding indefinitely.

- Convertible Debentures: Can be converted into equity shares.

- Non-Convertible Debentures: Cannot be converted into equity shares.

- First Charge Debentures: Have priority claim on company assets.

- Second Charge Debentures: Claim assets only after first charge holders are paid.

- Registered Debentures: Issued in the name of a specific holder.

- Bearer Debentures: Freely transferable without registration.

- Repayment: The principal amount is repaid after a given period.

- Use Case: Best suited for companies that do not want to face immediate equity dilution.

Debentures are a very good source of raising funds for companies without disturbing the equity ownership. Debentures attract investors as they are safe and certain of their returns.

5. External Commercial Borrowings (ECBs)

- Definition: Loans availed by businesses from foreign lenders.

- Types of External Commercial Borrowings (ECBs)

- Loan Agreements: Standardized foreign loans from banks or institutions.

- Bonds/Debentures: Debt instruments like FCCBs or FCEBs are issued internationally.

- Supplier’s Credit: Credit provided by foreign suppliers for purchases.

- Buyer’s Credit: Loans from foreign institutions for imports.

- Short-Term ECBs: Loans up to 3 years for working capital needs.

- Medium-Term ECBs: Loans for 3-5 years for moderate capital needs.

- Long-Term ECBs: Loans exceeding 5 years for infrastructure or large projects.

- Foreign Currency ECBs: Loans in foreign currencies, subject to exchange rate risks.

- Rupee-Denominated ECBs: Known as Masala Bonds, issued in Indian Rupees.

- Green Bonds: ECBs specifically for environmentally sustainable projects.

- Advantages: ECBs have lower interest rates compared to domestic sources.

- Limitations: ECBs are exposed to exchange rate risks and require regulatory approvals.

For internationally competitive corporations, ECBs provide access to international capital markets, thus attracting large-scale borrowings at competitive market rates.

Advantages of Medium Term Sources of Finance

Medium-term financing provides businesses with a balanced option between short-term and long-term funding, catering to projects or operations requiring moderate investment. These sources offer flexibility, liquidity preservation, and cost-effectiveness for enterprises.

- Flexibility: Suitable for the acquisition of assets up to working capital.

- Availability: Available to the firm either through banks or financial markets

- Cost predictability: Fixed investment and carrying cost of raising funds.

- Supports Growth: Expansion opportunities without long-term commitment of capital or bonds.

These benefits render medium-term finance an attractive opportunity for businesses to avoid losing operational flexibility. Its usage for both short-term and short-to-moderate goals lets businesses respond effectively to changes in the market.

Disadvantages of Medium Term Sources of Finance

Despite their benefits, medium-term sources of finance carry potential risks and limitations, particularly concerning costs and asset-related constraints. Businesses must weigh these challenges carefully.

- Interest Expense: Cash flows are impacted through frequent interest payables.

- Burden of Repayment: Fixed repayments push businesses into a financial crunch.

- Risk of Repossession/ Litigation: Failure to pay back may invite asset repossession or litigation processes.

- Limited Quantities: Medium-term options may not support high-level projects.

These disadvantages are no doubt relevant, but most often,theyt can be accommodated through proper financial planning. A firm needs to determine its ability to repay and should align its funding options with cash flow stability.

Medium Term Sources of Finance: Role in Business

Medium-term finance plays a significant role in business in achieving sustainable growth. It helps firms to:

- Extend Operations: Medium-term loans or leases can be applied for purchasing new machinery or opening up new branches.

- Manage Working Capital: This prevents the business activities from getting stuck due to the shortage of liquidity.

- Maintain Financial Risk: The loan payback can be done over several years, so there is no immediate financial shock.

- Plan Strategically: It meets long-term needs without overtaxing short-term resources.

Proper use of medium-term finance can, therefore, ensure the financial health and resilience of the business against fluctuations in the market.

Medium Term Sources of Finance FAQs

What are the medium-term sources of finance?

Medium-term sources of finance are financing techniques whose repayment time ranges between one to five years. Such finance instruments include term loans, hire-purchase, leasing, debentures, and external commercial borrowings.

What are the advantages and disadvantages of medium term sources of finance?

Advantages: Flexibility, accessibility, and predictable cost. Disadvantages: Re-payment obligation, cost of interest, and risks of default.

What is the difference between hire purchase and leasing?

Hire purchase: ownership changes after the last installment, whereas in leasing, the ownership stays with the lessor but the lessee utilizes the asset for a specific period.

Why is a medium term source of finance important?

They help business organizations meet working capital needs, asset procurement, and business expansion by spreading financial risks.

Is medium-term finance applicable to working capital?

Indeed, businesses commonly use medium-term loans to deal with and maintain the needs of working capital.