The net asset method of valuation of shares is among the most used methods to calculate the fair value of a company’s shares. It calculates the worth of equity shares by considering the company’s net assets, i.e., total assets minus liabilities. The method is vital in financial decision-making, mergers and acquisitions, and liquidation. The requirement for shares to be valued occurs in various scenarios, such as investment analysis and regulatory requirements. Understanding the Net Asset Method gives a good indication of a company’s financial well-being.

What is Net Asset Value?

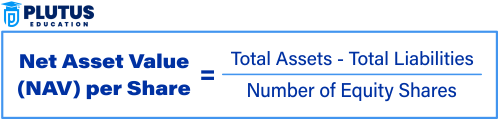

Net asset value (NAV) is the per-share worth of a firm, by subtracting assets and liabilities. It is a basic principle of the share valuation techniques employed to find the fair value of a stock or a mutual fund.

Net Asset Value Formula

The net asset value (NAV) formula determines a mutual fund or company’s per-share worth by dividing the difference between total assets and liabilities by the outstanding shares.

Factors Affecting Valuation of Shares

Share valuation depends on factors determining a company’s market value and investor confidence. Companies and investors must consider these critical factors to make the appropriate financial decisions. Below are five of the most important factors that affect share valuation.

- Company Performance: A company’s profit, growth rate, and revenue determine its share price. Strong financial performance means greater confidence amongst investors and higher valuations.

- Market Conditions: Interest rates, stock performance, and economic trends drive the value of shares. An improving economy drives valuations higher, while uncertainty is known to lower them.

- Earnings and Dividends: Businesses that yield consistent earnings and declare frequent dividends tend to get more investors. Greater earnings give more confidence, which results in improved share valuation.

- Industry Trends: The industry’s performance as a whole influences stock prices. Firms in expanding industries such as technology and healthcare tend to receive better valuations.

- Risk Factors: High debt, market competition, and business risks affect share value. Firms with good financial stability and low risks enjoy better valuations in the market.

Net Asset Method of Valuation of Shares Example

Let us compute the net asset value (NAV) per share of a mutual fund in Indian Rupees (₹). Let’s assume that the fund has invested ₹800 crore in various securities, whose values are computed per the day’s closing prices. The fund has outstanding shares of 40 crore.

Moreover, the fund also has ₹56 crore in cash and cash equivalents, ₹32 crore in cumulative receivables, and ₹6 crore as day’s accrued income. The fund also has liabilities in the form of ₹104 crore short-term liabilities, ₹16 crore long-term liabilities, and ₹0.8 crore as day’s accrued expenses.

Step 1: Calculate Total Assets: Total Assets= ₹800+₹56+₹32+₹6=₹894 crore

Step 2: Calculate Total Liabilities: Total Liabilities=₹104+₹16+₹0.8=₹120.8 crore

Step 3: Determine the Fund’s NAV: NAV=Total Assets−Total Liabilities.

NAV=₹894−₹120.8=₹773.2 crore

Step 4: NAV per Share = ₹773.2 crore/ 40 crore share

NAV per Share = ₹19.33

Need For Valuation of Shares

Valuation of shares is essential for financial institutions, investors, and companies to make wise decisions. Valuation of shares assists in financial reporting, risk management, mergers, and investment planning. The following are the most significant reasons businesses and investors need share valuation.

- Enabling Investment Choices: Share valuation enables investors to choose whether or not to purchase a stock based on its actual value. It assists in comparing various stocks to select the most lucrative ones. An accurately valued stock lessens the possibility of overpayment and results in improved investment returns.

- Facilitates Mergers and Acquisitions (M&A): Share valuation assists firms in setting fair prices when merging, buying, or entering into collaborations. Share valuation enables organisations to secure better deals and prevent financial loss. Proper valuation guarantees both sides gain from the deal while enjoying long-term stability.

- Securing Correct Financial Reporting: Part of financial reporting, share valuation normally affects balance sheets and income statements. This serves to ensure openness and adherence to reporting requirements. Correct valuation allows companies to ensure investor confidence and regulatory compliance without discrepancies.

- Improving Investor Relations: Most businesses employ valuation metrics to entice investors and stakeholders. It reflects their healthy financial situation as well as growth potential. A sound valuation creates confidence among investors and promotes long-term business growth alliances.

- Risk Management Effectively: Valuation makes asset values clear. It enables companies and investors to make informed decisions and use risk management measures. Knowing a stock’s value enables investors to reduce losses and diversify their portfolios effectively.

NAV and Mutual Funds

Mutual funds collect money from various investors and invest in securities such as stocks, bonds, and money market instruments. Every investor gets shares based on their investment. The cost of these shares is determined by the net asset value (NAV), which is the fund’s total assets minus liabilities divided by outstanding shares.

Unlike stocks that are subject to fluctuations in prices throughout the day, mutual funds have prices set based on their daily closing securities’ values. At the end of every trading day, the fund managers determine the NAV by summing up the value of all securities, adjusting for other assets, subtracting liabilities, and then dividing it by the total outstanding shares.

NAV and Investment Decisions

Investors utilise net asset value (NAV) to gauge the financial soundness of a company and invest accordingly. When NAV is high, it represents good financial solidity, allowing investors to compare several stocks and gauge whether a stock is undervalued or overvalued. A continuously rising NAV also boosts shareholder confidence and invites long-term investors.

For instance, if a firm’s NAV is less than its market value, the stock can be overvalued, while one selling below its NAV might be undervalued. Investors evaluate these facts to determine whether they should buy or sell stock. NAV is significant in the valuation of stocks and aids in the selection of lucrative investment options.

Relevance to ACCA Syllabus

The net asset valuation method of shares is a core subject of ACCA’s Financial Management (FM) and Advanced Financial Management (AFM) papers. The subject enables the student to comprehend how companies set share values according to assets and liabilities. It is especially effective for valuing unlisted businesses, mergers and acquisitions, and liquidation.

Net Asset Method of Valuation of Shares ACCA Questions

Q1: What does the Net Asset Method primarily focus on when valuing shares?

A) Future cash flows of the company

B) Market price of shares

C) Total assets minus total liabilities

D) Dividend payout ratio

Ans: C) Total assets minus total liabilities

Q2: The Net Asset Value (NAV) per share is calculated as:

A) Net Assets / Number of Shares Outstanding

B) Net Profit / Total Revenue

C) Market Price per Share × Earnings Per Share

D) Total Liabilities / Number of Shares

Ans: A) Net Assets / Number of Shares Outstanding

Q3: Which of the following is a limitation of the Net Asset Method?

A) It ignores the company’s asset base

B) It does not consider intangible assets and future earnings potential

C) It is based entirely on market speculation

D) It is only applicable to publicly traded companies

Ans: B) It does not consider intangible assets and future earnings potential

Q4: When is the Net Asset Method most appropriate for valuing a company?

A) When the company has high future growth potential

B) When the company is under liquidation or restructuring

C) When the company has strong cash flow projections

D) When the company is publicly listed with high trading volume

Ans: B) When the company is under liquidation or restructuring

Q5: If a company’s total assets are $500 million and its total liabilities are $200 million, what is the Net Asset Value (NAV)?

A) $300 million

B) $500 million

C) $200 million

D) $700 million

Ans: A) $300 million (NAV = Total Assets – Total Liabilities)

Relevance to US CMA Syllabus

The Corporate Finance and Financial Statement Analysis section of the US CMA syllabus covers the net asset method. CMA candidates employ this method to gauge a company’s financial condition by reviewing the book value of assets and liabilities. The application of this method is significant in capital restructuring, investment appraisal, and financial reporting decisions.

Net Asset Method of Valuation of Shares US CMA Questions

Q1: The Net Asset Method is most useful for valuing companies that:

A) Are experiencing high revenue growth

B) Have significant tangible assets and may be liquidated

C) Have stable dividend payouts

D) Are publicly traded on a stock exchange

Ans: B) Have significant tangible assets and may be liquidated

Q2: Which of the following adjustments may be necessary when using the Net Asset Method?

A) Adjusting asset values to fair market value

B) Ignoring all liabilities

C) Using future projected earnings

D) Applying the P/E ratio to book value

Ans: A) Adjusting asset values to fair market value

Q3: The Net Asset Method of valuation is best suited for:

A) Startups with no physical assets

B) Companies with high intellectual property value

C) Asset-intensive businesses like real estate and manufacturing

D) Firms with volatile stock prices

Ans: C) Asset-intensive businesses like real estate and manufacturing

Q4: What is the key limitation of using book value in the Net Asset Method?

A) It does not reflect fair market value

B) It includes future projected cash flows

C) It considers only intangible assets

D) It relies on investor sentiment

Ans: A) It does not reflect fair market value

Q5: Which of the following valuation methods is an alternative to the Net Asset Method?

A) Price-to-Earnings (P/E) Ratio

B) Dividend Discount Model (DDM)

C) Market Capitalization Model

D) All of the above

Ans: D) All of the above

Relevance to US CPA Syllabus

The US CPA curriculum covers the net asset approach under Financial Accounting and Reporting (FAR) and Business Environment and Concepts (BEC). CPA aspirants need to know how to value a firm’s equity in terms of net assets, especially during liquidation, mergers, and acquisitions.

Net Asset Method of Valuation of Shares US CPA Questions

Q1: Which financial statement is most important in applying the Net Asset Method?

A) Income Statement

B) Statement of Cash Flows

C) Balance Sheet

D) Retained Earnings Statement

Ans: C) Balance Sheet

Q2: If a company is undergoing liquidation, which valuation method is most appropriate?

A) Discounted Cash Flow (DCF) Method

B) Net Asset Method

C) Dividend Discount Model (DDM)

D) Price/Earnings (P/E) Ratio

Ans: B) Net Asset Method

Q3: The Net Asset Method is less effective when valuing which type of company?

A) A real estate company with significant physical assets

B) A technology startup with significant intangible assets

C) A manufacturing company with substantial inventory

D) A firm with substantial plant and equipment

Ans: B) A technology startup with significant intangible assets

Q4: When using the Net Asset Method, goodwill is typically:

A) Ignored unless it has a market value

B) Always included in net asset calculations

C) Treated as a liability

D) Used as the primary measure of company value

Ans: A) Ignored unless it has a market value

Q5: In an acquisition, why might a company’s net asset value differ from its market value?

A) Net assets ignore brand and goodwill value

B) Market value does not include liabilities

C) Net asset valuation is based on stock market trends

D) Market value is always lower than book value

Ans: A) Net assets ignore brand and goodwill value

Relevance to CFA Syllabus

The CFA program details the net asset approach in Equity Investments and Corporate Finance. CFA candidates examine how intangible and tangible assets affect a company’s valuation. The approach finds broad application in valuing private companies, making investment decisions, and examining company balance sheets.

Net Asset Method of Valuation of Shares CFA Questions

Q1: What is the primary limitation of the Net Asset Method in equity valuation?

A) It ignores the company’s earnings potential

B) It includes projected cash flows

C) It only applies to profitable companies

D) It is based on short-term market fluctuations

Ans: A) It ignores the company’s earnings potential

Q2: The Net Asset Method is most useful for valuing companies in which industry?

A) Technology startups

B) Real estate and manufacturing

C) E-commerce businesses

D) Financial services

Ans: B) Real estate and manufacturing

Q3: When adjusting assets under the Net Asset Method, companies should:

A) Use historical cost for asset valuation

B) Adjust to fair market value

C) Ignore depreciation expenses

D) Focus only on cash and receivables

Ans: B) Adjust to fair market value

Q4: Which of the following is a key advantage of the Net Asset Method?

A) It is simple and based on readily available financial data

B) It considers future earnings growth

C) It values intangible assets like brand reputation

D) It adjusts for inflation automatically

Ans: A) It is simple and based on readily available financial data

Q5: If a company’s total net assets are $10 million and there are 1 million shares outstanding, what is the Net Asset Value per share?

A) $5

B) $10

C) $20

D) $50

Ans: B) $10 (NAV per share = Net Assets / Shares Outstanding)