Fire insurance is an important financial safety net protecting the lives of individuals and businesses from the loss that can be caused by fire-related events. This form of insurance is founded on several key principles that help to ensure that there is a sense of equity, trust, and clarity between the insurer and the insured. The principles of fire insurance detail how policies are issued, claims are settled, and rights and responsibilities are maintained. Fire insurance safeguards your property and assets from fire-related losses. It ensures financial protection, providing peace of mind in unforeseen circumstances. Explore its features, principles, and types for informed decisions.

Meaning of Fire Insurance

Fire insurance provides coverage against damages and losses caused by fire. It compensates for property damage, loss of assets, and other fire-related financial liabilities. Fire insurance provides a formal mechanism to protect property and other assets against losses due to fire. This policy offers peace of mind by ensuring the insured party does not bear the full brunt of unexpected fire-related disasters.

Features of Fire Insurance

Fire insurance provides a formal mechanism to protect property and other assets against losses due to fire. Its characteristics emphasize the specific nature of coverage, financial protection principles, and mutual agreement between the insurer and the insured. Below are the detailed explanations of its key features:

- Indemnity-based: This actual loss compensation paid under fire insurance helps restore the insured to their previous financial position, which existed prior to the happening of the loss.

- Time-Bound Policies: Fire insurance policies are normally issued for a term. The policyholder must renew the contract periodically so that he does not lose coverage and is protected in case of fire hazards.

- Contract of Good Faith: The insured and the insurer both have to behave in good faith and disclose all material facts at the inception of the policy. Concealing major information, like previous fire outbreaks, may cause the claim to be rejected or the policy might be canceled.

Principles of Fire Insurance

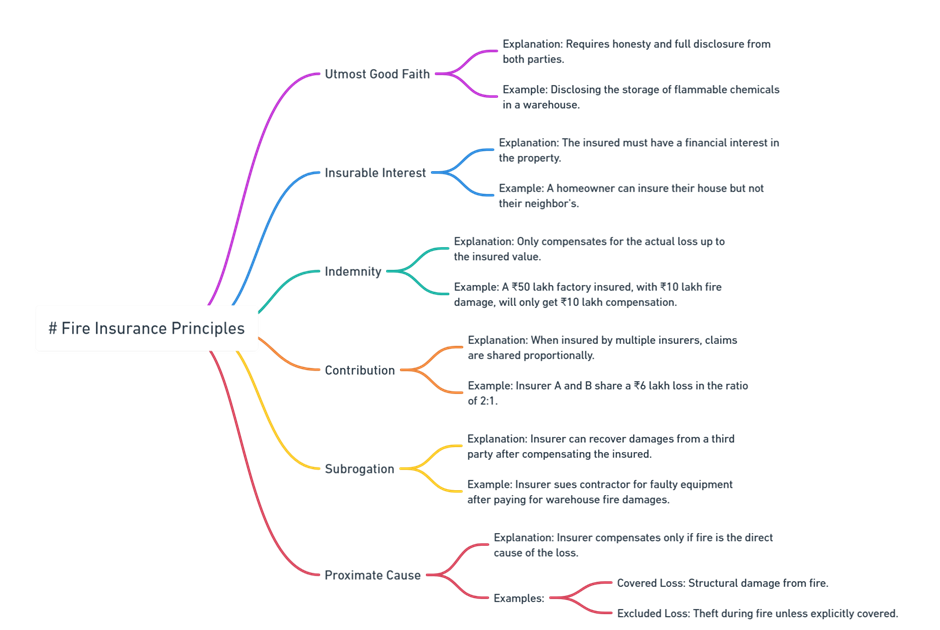

Fire insurance is a crucial aspect of property and casualty insurance, designed to protect policyholders from financial losses due to fire-related damages. It covers the costs associated with repairing or replacing property that has been damaged or destroyed by fire. The principles of fire insurance are grounded in risk management and financial protection, ensuring that individuals and businesses can recover from devastating events. Key principles include indemnity, insurable interest, subrogation, and utmost good faith, each playing a vital role in how fire insurance operates and provides security for policyholders. Understanding these principles helps in effectively navigating the complexities of fire insurance coverage.

Principle of Utmost Good Faith

This principle requires that both parties involved, the insurer and the insured, act honestly and disclose information to each other. The insured is expected to provide accurate details about the property, its usage, the nature of risks involved, and the history of prior claims. Similarly, the insurer should clearly communicate the terms and conditions of the policy.

Example:

Honesty from the Insured: If a business owner applies for fire insurance for a warehouse storing flammable chemicals, they must disclose the type and quantity of chemicals stored. Failure to do so might result in the rejection of a claim if a fire occurs.

Principle of Insurable Interest

The principle is that the insured must have a financial interest in the property being insured. In other words, they should be able to suffer a direct financial loss if the property is damaged or destroyed by fire. This principle ensures that only those with a legitimate interest can seek coverage.

Example:

A home owner can insure his house since he owns it and would be financially affected if his house caught fire and was destroyed. Nevertheless, a neighbor or tenant cannot insure the same house unless he, too, has an interest in that house, such as valuable possessions in the house.

Principle of Indemnity

Fire insurance is a contract of indemnity, meaning that it indemnifies the insured for only the actual loss incurred up to the insured value of the property. Thus, it will not make a profit from the claim of the insured.

Example:

If a factory worth ₹50 lakh is damaged by fire to the extent of ₹10 lakh, the insurer will pay only ₹10 lakh, even though the policy coverage was for ₹50 lakh. This ensures that the insured is restored to his original financial position without gaining any additional benefit.

Principle of Contribution

When the same property is insured with more than one insurer, the principle of contribution ensures that all insurers share the claim proportionally. This prevents the insured from claiming the full amount separately from each insurer and profiting from the situation.

Example:

A commercial building is insured with two companies: Insurer A for ₹20 lakh and Insurer B for ₹10 lakh. If a fire causes damage of ₹6 lakh, the claim will be shared between the insurers in the ratio of their coverages:

Insurer A pays ₹4 lakh (two-thirds of the loss).

Insurer B pays ₹2 lakh (one-third of the loss).

Principle of Subrogation

The insurer acquires the rights of the insured to seek recovery from any third party responsible for the damage after compensating the insured for the loss. This ensures that the insured does not receive compensation twice for the same loss.

Example:

A warehouse catches fire due to faulty electrical equipment supplied by a contractor. The insurer pays for the damages after compensating the insured. He can sue the contractor for negligence to recover the amount paid.

Cause Proxima or Proximate Cause

The insurer will pay only if the proximate or primary cause of the loss is fire. If the fire indirectly causes other damages, such as theft or additional losses, those damages are generally not covered unless explicitly stated in the policy.

Example:

- Covered Loss: A fire in a storage facility causes structural damage to the building. Since the fire was the direct cause, the insurer compensated for the damage.

- Excluded Loss: The same fire will also cause a theft loss in the case where the thief exploits the open doors and robs the goods of the warehouse unless that policy explicitly includes it.

Elements of Fire Insurance

Fire insurance contracts contain essential elements that outline the scope of coverage, terms, and obligations. Understanding these elements ensures clarity and a smooth policy process.

- Policy Schedule: This is a description of the covered property, giving details on value, location, and type of coverage.

- Policy Document: The policy document provides details of every term, condition, inclusion, and exclusion of coverage. It is a legally binding agreement between the insurer and the insured with the purpose of mutual understanding.

- Premium Payment: The premium is paid by the insured to keep the policy active. The lapse of the policy due to nonpayment of premium will leave the insured unguarded against fire risks.

Types of Fire Insurance

Fire insurance policies are devised to meet the demands of customers that may vary from managing house risks to business-specific risks. Here are the descriptive types:

- Specific Policy: This policy covers damages caused by a fire within an insured amount. If the Policy: A comprehensive policy provides wider cover, which includes not only fire but allied risks such as earthquakes, floods, or storms. This policy is best suited for properties that are exposed to several environmental hazards.

- Valued Policy: In loss is more than the amount covered, the insured cannot claim more than the covered limit. This keeps the boundary in demarcation.

- Floating Policy: Companies whose wares are warehoused at various places are usually favored with a floating policy. All their locations fall under one policy that simplifies their management and reduces costs.

Examples of Fire Insurance

Fire insurance finds practical application in various scenarios, highlighting its significance in real-life situations:

- Residential Fire Insurance: A family’s kitchen suffers fire damage due to a gas leak. The fire insurance policy covers the cost of repair, including replacement of cabinets and appliances, ensuring financial recovery.

- Commercial Fire Insurance: A warehouse holding goods worth ₹50 lakh is engulfed in flames. The insurance compensates for the loss, allowing the business to replenish its inventory and continue operations.

Benefits of Fire Insurance Policy

Fire insurance offers numerous benefits, providing essential financial protection and peace of mind. Here are the key advantages:

- Financial Security: Fire insurance covers losses due to fire, ensuring you don’t face overwhelming financial burdens. It compensates for damages, helping you rebuild without depleting savings.

- Replacement Cost Coverage: Most policies contain replacement cost coverage, allowing you to restore any damaged assets to a like-new state, minimizing losses from fire damages.

- Risk Coverage: Coverage for allied risks such as explosions, natural catastrophes, and civil commotion depending on the terms is common in many fire insurance. This widens the protection that one receives.

Principles of Fire Insurance FAQs

What is covered under fire insurance?

Fire insurance covers damages brought about by fire, smoke, explosions, and connected perils like lightning or riots.

How is the premium for fire insurance determined?

Premium is determined in accordance with the value of the property, place, type, construction, and risk study.

Is there business interruption coverage for fire insurance?

Yes, there are fire insurance policies that cover business interruption due to a fire.

Do homeowners require fire insurance?

Fire insurance is not compulsory but highly recommended for financial protection.

How does a policyholder file a fire insurance claim?

Policyholders must notify the insurer immediately, submit claim forms, and provide evidence of damages for processing.