SME finance is necessary for small and medium business survival and growth. This finance facilitates cash management for businesses to expand operations and remain competitive. SME finance defines the financing facilities offered to small and medium enterprises (SMEs) to help them expand their operations and grow their businesses. SMEs are also integral to the economy as they create jobs and contribute to GDP. But, they often struggle with financial issues that limit their growth. SME Finance, which includes credit, loans, investment, etc., is tailored to the needs of small and medium enterprises. However, this can only be achieved if the businesses have enough cash to ensure stability, innovations, and consistency.

What is SME Finance?

SME Finance offers financial services and products to small and medium businesses to finance their operations and growth. It comprises several funding sources like bank loans, venture capital, crowdfunding, and grants from the government. SMEs need finance for working capital, business growth, buying equipment, and day-to-day running expenses.

SME Full Form in Finance

SME stands for Small and Medium Enterprises in Finance. By the nation, these enterprises are classified according to their income, assets, or the number of employees.

SME finance is tailored financing arrangements to fund small and medium-scale enterprises. Short-term and long-term funds are available under the arrangement to accommodate various needs. Growth, survivability, and expansion are of primary focus. Banks, finance companies, and alternative lenders offer the money for SMEs to run the operation and expand as needed.

Why Do SMEs Need Finance?

SMEs require funding for different purposes to run smoothly and develop. They need initial capital to establish companies and working capital to cover regular expenses. Financing aids in increasing business, technology upgrading, and investing in new equipment. SMEs also employ funding to pay debts and consolidate loans.

Importance of SME Finance

SME Finance is key to the development and sustainability of small and medium enterprises. In the absence of suitable funding, SMEs are not able to compete, innovate, and grow.

- Increases Economic Growth: SMEs play an important role in contributing to GDP and employment. Appropriate financial support increases productivity and efficiency. An efficient SME sector results in improved economic stability and increased national income.

- Encourages Innovation and Technology Adoption: Financing enables SMEs to spend on research and development. Firms can update to new technology and automation. This enhances productivity, lowers the cost, and increases long-term growth.

- Enhances Cash Flow Management: Facilitates maintaining a consistent cash flow for day-to-day operations. Avoids financial stress and business closure. Smooth cash flow guarantees uninterrupted operations and on-time payments to suppliers.

- Facilitates Job Creation: SMEs are significant job creators. Finance enables the recruitment and training programs. More extraordinary financial assistance results in more excellent job opportunities and manpower growth.

- Improves Competitiveness: Finance availability enables SMEs to compete with multinational corporations. Facilitates enhancing product quality and customer service. Robust financial support helps SMEs increase their presence in the market.

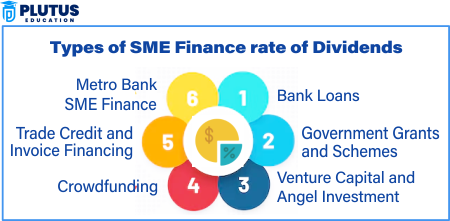

Types of SME Finance

SMEs can access various financial options depending on their needs and eligibility. Each type of SME Finance has its benefits and limitations.

Bank Loans

SME banks provide loans for business growth, working capital, and purchasing assets. They may be secured or unsecured based on the company’s financial condition. Term loans for growth, working capital loans for day-to-day operations, and equipment loans for purchasing machinery are the most common bank loans provided by SME banks. The tenure is 6 months to 10 years, depending on the nature of the loan. Bank loans are a sure means of financing but usually demand a good credit history and financial records.

Government Grants and Schemes

Governments across the globe offer grants, subsidies, and financial assistance to SMEs. The money facilitates business expansion, innovation, and employment generation in targeted sectors or areas. Several programs emphasise technology uptake, environmental sustainability, and rural growth. For instance, the Global SME Finance Forum disseminates information on government-guaranteed SME financing programs. Grants differ from loans because they need not be repaid, so they are a low-cost funding option. However, companies must satisfy stringent eligibility requirements and undergo elaborate application procedures to be considered.

Venture Capital and Angel Investment

Startups and high-growth SMEs can entice venture capitalists and angel investors who invest money in return for company equity. Such financing is best suited for innovative companies with great potential for quick growth. Investors look for sound business plans, scalable models, and long-term profitability before they invest. Venture capital enables businesses to grow fast but at the cost of surrendering partial ownership and decision-making authority. Companies must negotiate terms of investment with caution to maintain control while acquiring required funds.

Crowdfunding

Crowdfunding enables SMEs to use online platforms to raise funds from many investors or the public. It particularly benefits new products, creative ventures, and social enterprises. Reward-based, equity-based, or donation-based crowdfunding can be used by businesses to raise funds. A good campaign, clear business vision, and good marketing strategy are critical to success. It may be difficult to achieve fundraising targets, and businesses need to interact with investors to build trust and support actively.

Trade Credit and Invoice Financing

SMEs can obtain short-term finance using trade credit and invoice financing. Trade credit enables companies to purchase goods and services on credit and settle later, enhancing cash flow. Invoice financing allows SMEs to acquire loans based on outstanding invoices, providing constant working capital. These arrangements enable companies to finance liquidity and minimize the need for bank loans. SMEs need strong credit relationships with suppliers and buyers to access good trade terms.

Metro Bank SME Finance

Examples include lending products like business loans, overdraft facilities, and asset financing from Metro Bank. Repayment periods are flexible, interest rates are competitive, and a one-to-one banking service will help expand the business. Metro Bank is popular among SMEs because it specializes in getting facilities and tailored funding options approved quickly. Its funding options help businesses manage cash, grow the business, and invest in new projects.

Challenges of SME Finance

Though loan solutions are offered, SMEs grapple with inadequate collateral, interest, complex loans, and the challenge of accessing funds.

- Limited Collateral and Credit History: Most SMEs do not have assets to present as collateral. Lack of sufficient credit history makes it challenging to get bank loans. Lenders prefer companies with a good financial track record, which makes it more difficult for new SMEs to access funds.

- High Interest Rates and Fees: Banks and other financial institutions impose high interest on SME loans. Extra processing charges and concealed fees add to the economic weight. Small enterprises mostly cannot afford them, and their profitability suffers.

- Complicated Loan Application Process: Long documentation and approval processes hold up access to capital. Financial literacy and compliance needs are problematic for many SMEs. Time-consuming processes discourage firms from applying for much-needed credit.

- Unawareness regarding Financial Alternatives: SMEs usually lack accessible financing schemes and grants. Most companies do not look into other modes of funding, such as crowdfunding. There is a lack of knowledge that keeps them from gaining access to superior sources of financing.

- Cash Flow and Debt Management Problems: Inefficient cash flow management results in loan defaults. Excessive debt lowers business profitability. With inadequate financial planning, SMEs cannot sustain stable operations and meet loan repayment obligations on time.

How Does SME Finance Work?

SME Finance links small firms with banks, investors, and alternative lenders. The steps involved are:

- Identifying Financial Requirements: SMEs assess their financial requirements, either for working capital, expansion, or technology upgradation. Identifying the exact financial requirements helps you choose the right kind of financing. Definite purpose ensures maximum use of funds and better loan sanction rates.

- Venturing into Sources of Finance: Firms compare sources of finance such as government schemes, venture capital, or bank loans. They contrast interest rates, repayment terms, and the ease of qualifying for these sources. The right funding option reduces financial pressures and increases long-term business stability.

- Application and Documentation: SMEs approach lenders for loans with the documents required, such as financial records, business proposals, and credit reports. Documenting appropriately expedites the loan processing and reduces rejection opportunities. Proper records help secure good funding options.

- Approval and Disbursement: The application is screened by lenders regarding creditworthiness and risk considerations. Approved money is credited to the SME account. Building lender confidence requires timely utilization of funds and reasonable financial prudence.

- Loan Repayment and Monitoring: SMEs repay loans in fixed instalments or according to agreed terms. Effective financial management guarantees timely repayment and business development. Cash flow and expense monitoring prevents financial distress and ensures effortless loan repayment.

Relevance to ACCA Syllabus

SME (Small and Medium Enterprise) Finance is treated under Financial Management (FM) and Advanced Financial Management (AFM) of the ACCA syllabus. ACCA examines study sources of finance available to SMEs, management of working capital, risk management, and financial reporting of SMEs. Knowledge about SME finance is important as it helps businesses maintain cash flow, raise external financing, and carry on long-run growth.

SME Finance ACCA Questions

Q1: Which of the following is a common financing source for SMEs?

A) Treasury bonds

B) Venture capital

C) Sovereign wealth funds

D) Central bank loans

Ans: B) Venture capital

Q2: Which financial ratio is most important for SMEs when seeking short-term financing?

A) Earnings Per Share (EPS)

B) Current Ratio

C) Price-to-Earnings Ratio (P/E)

D) Dividend Yield

Ans: B) Current Ratio

Q3: What is a major disadvantage of equity financing for SMEs?

A) High interest costs

B) Dilution of ownership

C) Requires collateral

D) Fixed repayment schedule

Ans: B) Dilution of ownership

Q4: Which of the following is NOT a typical SME financing option?

A) Bank loans

B) Trade credit

C) Initial Public Offering (IPO)

D) Government grants

Ans: C) Initial Public Offering (IPO)

Relevance to US CMA Syllabus

SME Finance is one of the building blocks of Corporate Finance and Risk Management in the US CMA Part 2 examination. CMA aspirants review financing strategies, financial planning, and SMEs’ cash management. They assess various sources of financing, such as bank loans, venture capital, and trade credit, enabling SMEs to manage their financial composition efficiently.

SME Finance US CMA Questions

Q1: What is the primary advantage of using trade credit in SME financing?

A) No interest cost

B) Requires a long approval process

C) Reduces equity ownership

D) Increases financial risk

Ans: A) No interest cost

Q2: A small business wants to improve its working capital management. Which of the following would help achieve this?

A) Reducing accounts payable period

B) Increasing inventory holding period

C) Extending accounts receivable collection

D) Negotiating longer payment terms with suppliers

Ans: D) Negotiating longer payment terms with suppliers

Q3: What is the key benefit of factoring as a financing option for SMEs?

A) Immediate access to cash

B) Lower financing cost than bank loans

C) No need for collateral

D) No impact on balance sheet

Ans: A) Immediate access to cash

(Factoring allows SMEs to sell receivables for quick cash flow.)

Q4: Which government-backed loan program is often used by SMEs in the United States?

A) FDIC-backed loans

B) Federal Reserve SME Program

C) Small Business Administration (SBA) loans

D) SEC SME Investment Fund

Ans: C) Small Business Administration (SBA) loans

Relevance to US CPA Syllabus

The Financial Accounting and Reporting (FAR) and Business Environment and Concepts (BEC) areas of the CPA exam discuss SME finance within business financing, financial planning, and cash flow management. Candidates should be familiar with loan facilities, government incentives, and SME financial reporting standards to advise small businesses appropriately.

SME Finance US CPA Questions

Q1: Which financial statement is most important for evaluating an SME’s ability to repay debt?

A) Income Statement

B) Statement of Financial Position (Balance Sheet)

C) Cash Flow Statement

D) Statement of Retained Earnings

Ans: C) Cash Flow Statement

Q2: What is a common financial risk that SMEs face?

A) Limited access to capital

B) High stock market volatility

C) Low government regulation

D) Unlimited liability protection

Ans: A) Limited access to capital

Q3: An SME wants to expand but lacks the capital. Which of the following is a potential long-term financing option?

A) Trade credit

B) Angel investment

C) Bank overdraft

D) Accounts payable

Ans: B) Angel investment

Q4: What is one advantage of debt financing for SMEs compared to equity financing?

A) No repayment obligation

B) Interest payments are tax-deductible

C) No collateral is required

D) Owners retain full control

Ans: B) Interest payments are tax-deductible

Relevance to CFA Syllabus

SME Finance is one of the key subjects of Corporate Finance and Investment Management in the CFA Level 1 and Level 2 examinations. CFA candidates examine how SMEs finance their operations using equity financing, debt financing, and government subsidies. They also learn how SMEs struggle to raise investment and control liquidity risks.

SME Finance CFA Questions

Q1: Which of the following is the most significant challenge for SMEs in obtaining bank loans?

A) High stock market volatility

B) Lack of credit history and collateral

C) High public shareholder expectations

D) Excess cash reserves

Ans: B) Lack of credit history and collateral

Q2: Which alternative financing option allows SMEs to raise funds from multiple small investors?

A) Venture capital

B) Crowdfunding

C) Private equity

D) Commercial paper

Ans: B) Crowdfunding

Q3: Which factor do banks consider when assessing an SME’s loan application?

A) Market share growth

B) Management team’s experience

C) Government policies

D) Political stability

Ans: B) Management team’s experience

Q4: Which of the following is a short-term financing option for SMEs?

A) Convertible bonds

B) Term loans

C) Bank overdraft

D) Preferred Equity

Ans: C) Bank overdraft