A substantive audit procedure consists of tools that auditors utilize to ascertain if financial records are accurate, complete, and valid. Substantive audit procedures are methods audit firms use to gather sufficient and reliable evidence to audit the accounts of companies. This procedure is the foundation of the financial audit, and it ensures that financial reports are what auditors would refer to as accounting in a language where the terms are accounting principles and regulations. Substantive procedures are used to provide reasonable assurance to auditors that financial statements are presented relatively concerning an entity’s financial position.

Firms should keep adequate records to support their transaction documentation. Directly, auditors perform substantive testing to assess the trustworthiness of financial data. This would include examining the supporting documents of accounting entries recorded, validating invoices, and confirming balances with third parties. These tests aid auditors in determining whether the financial statements are error-free or fraudulent.

What is Substantive Audit Procedure?

Substantive audit procedures provide transparency through the financial reports. They assure investors, creditors, and stakeholders about what the company is worth. Under an audit plan, substantive procedures are included alongside control testing and risk assessment. They will also enhance the credibility of finance, through which a greater level of trust will be entrenched in an organization’s reports.

Auditors also use substantive procedures in line with the financial statement auditing risk assessment. In high-risk areas, more intensive testing is applied. Substantive procedures generally deal with affirming balances and transactions through direct evidence but help auditors build up an opinion on financial statements and compliance to accounting standards.

Objective of Substantive Audit Procedure

Substantive procedures are not the same thing as control testing. Control testing assesses the adequacy of internal controls, while substantive procedures substantiate financial information. Auditors will perform these tests when they decide their control tests are insufficient.

Companies must conduct a more comprehensive substantive procedure on accounts with weaker internal controls. The auditors, therefore, undertake the tests to verify the financial statement’s veracity. The substantive procedures for the financial report should be correctly and appropriately implemented.

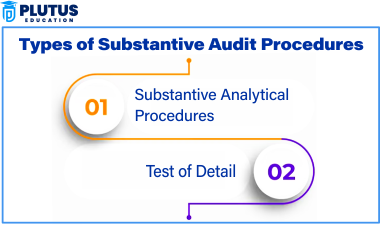

Types of Substantive Audit Procedures

Substantive procedures used in auditing may be classified broadly into two types: substantive analytical procedures and tests of detail. They assist auditors in confirming financial records and identifying material misstatements.

Substantive Analytical Procedures

Substantive analytical procedures are an analysis of relationships among data in a study. About the auditor’s current financial data, trend references against prior periods, industry averages, or expected results are made. These procedures disclose unusual relationships that may signify fraud or error.

For example

An auditor compares the sales revenues over five years, and if sudden increases or decreases are observed, they will trigger further investigation by the auditor. Calculations of expenditure ratios at different times have aided auditors in identifying contrary trends. Gross profit margin comparisons with industry norms can raise financial anomalies.

Test of Detail

The examination of details constitutes the test of more information. To ascertain correctness, auditors check invoices, contracts, bank statements, etc..

For Example

- Verification by sales invoices of recorded revenue.

- Verification through payroll records of salary expenses.

- Verify the inventory records for stock valuation.

| Criteria | Substantive Analytical Procedures | Test of Details |

| Purpose | Identify unusual trends or fluctuations | Verify individual transactions and balances |

| Method | Comparing financial data and ratios | Inspecting supporting documents |

| Example | Analyzing revenue growth over time | Checking invoices for recorded sales |

Importance of Substantive Audit Procedures

To a financial auditor, substantive procedure is the most important element. Substantive procedures then help auditors to bring forth misstatements, determine compliance with accounting standards, and make the financial statements more transparent.

Detecting Errors and Fraud

Auditors could also use substantial procedures to detect financial statements. Misstatement of revenues and expenses, or misstatement of assets, could severely mislead the stakeholders. Thus, auditors put in place substantive procedures to ensure that the financial statements are reliable and do not have material misstatements.

Compliance

Financial statements are supposed to abide by accounting standards and rules of law. Auditors, through substantive evidence, would analyze the results based on compliance. Noncompliance may have fines and legal implications.

Enhancing Credibility of Finance

The collection of finances is based on financial statements that the investors and creditors analyze. Thus, substantive procedures add credibility to the correct assertion of economic data. It enhances the credibility and reliability of financial reporting.

Supporting Audit Opinion

Auditors give an opinion based on the quality of financial statements. Substantive procedures provide the evidence that supports the issuance of an audit opinion. Substantive procedures would not be applicable, and without them, the auditors would not have been able to issue a valid opinion on the financial statements.

Improve Internal Control

The substantive procedures allow the entities to improve their internal control system’s adequacy. That enables management to take corrective action in case of errors or fraud. Reducing financial risks and increasing reporting accuracy will follow internal control improvements. Substantive procedures conducted by auditors are linked to the risk during the audit. Areas associated with high risk would require in-depth verification, while areas associated with low risk could use analytical procedures.

Relevance to ACCA Syllabus

Substantive audit procedures are crucial to the ACCA syllabus, particularly in the audit and assurance paper. ACCA candidates must understand these procedures to conduct risk assessments and gather audit evidence effectively. Since financial reporting plays a major role in professional practice, knowledge of substantive audit procedures enables ACCA students to evaluate financial statements accurately and detect misstatements.

Substantive Audit Procedures ACCA Questions

- Which type of substantive procedure is used to verify individual transactions?

A) Substantive analytical procedures

B) Test of details

C) Control testing

D) Internal audit procedures

Answer: B) Test of details

- Why do auditors perform substantive procedures?

A) To ensure compliance with tax regulations

B) To assess control effectiveness

C) To detect material misstatements in financial statements

D) To reduce management’s workload

Answer: C) To detect material misstatements in financial statements

- What is the main purpose of a substantive analytical procedure?

A) To confirm bank balances

B) To analyze trends and ratios in financial data

C) To inspect individual invoices

D) To document management assertions

Answer: B) To analyze trends and ratios in financial data

- When are substantive audit procedures required?

A) Only when fraud is suspected

B) When financial statements carry a high risk of misstatements

C) When control testing is sufficient

D) When no financial errors exist

Answer: B) When financial statements carry a high risk of misstatements

- Which document guides substantive procedures?

A) ISA 500

B) IFRS 15

C) IAS 36

D) FASB Concept Statement

Answer: A) ISA 500

Relevance to US CMA Syllabus

The US CMA syllabus covers substantive audit procedures under financial statement analysis and risk assessment. CMAs must understand these procedures to verify financial records, detect fraud, and ensure compliance with regulatory standards. Knowledge of substantive procedures enhances decision-making and risk mitigation in financial management.

Substantive Audit Procedures US CMA Questions

- What is the primary objective of substantive procedures?

A) To test the reliability of internal controls

B) To detect misstatements in financial statements

C) To optimize cost management

D) To improve operational efficiency

Answer: B) To detect misstatements in financial statements

- What type of substantive procedure involves financial ratio analysis?

A) Test of details

B) Analytical procedures

C) Control testing

D) Compliance procedures

Answer: B) Analytical procedures

- When should substantive procedures be performed in an audit?

A) At the beginning of the financial year

B) Only when fraud is suspected

C) When assessing material misstatements

D) Only for large organizations

Answer: C) When assessing material misstatements

- Which method is most effective for identifying fraudulent transactions?

A) Trend analysis

B) Bank reconciliations

C) Reviewing management reports

D) Examining supporting documentation

Answer: D) Examining supporting documentation

- What is a limitation of substantive analytical procedures?

A) They are ineffective in detecting fraud

B) They require excessive time and effort

C) They rely on accurate historical data

D) They do not provide financial insights

Answer: C) They rely on accurate historical data

Relevance to US CPA Syllabus

US CPA candidates learn substantive audit procedures in financial auditing and assurance. These procedures help CPAs assess risk, verify financial transactions, and ensure compliance with GAAP. Mastery of substantive procedures is essential for expressing audit opinions on financial statements.

Substantive Audit Procedures US CPA Questions

- Why do auditors use substantive procedures?

A) To replace internal controls

B) To assess financial statement reliability

C) To improve cash flow

D) To eliminate errors

Answer: B) To assess financial statement reliability

- What is a test of details?

A) A review of financial trends

B) A comparison of industry benchmarks

C) An inspection of supporting documents

D) An evaluation of internal controls

Answer: C) An inspection of supporting documents

- Which statement about substantive procedures is true?

A) They are only used in small audits

B) They provide direct evidence of financial transactions

C) They assess control effectiveness

D) GAAS does not require them

Answer: B) They provide direct evidence of financial transactions

- When are substantive procedures more commonly used?

A) When internal controls are weak

B) When internal controls are strong

C) When there is no risk of misstatements

D) When an audit is not required

Answer: A) When internal controls are weak

- What is the key focus of substantive procedures?

A) Evaluating employee performance

B) Detecting material misstatements

C) Verifying compliance with HR policies

D) Assessing company strategy

Answer: B) Detecting material misstatements

Relevance to CFA Syllabus

The CFA syllabus covers substantive audit procedures as part of financial reporting and analysis. Understanding these procedures helps CFA candidates assess financial statement reliability, detect financial misstatements, and evaluate investment risks.

Substantive Audit Procedures CFA Questions

- Why are substantive procedures important for investment analysis?

A) They improve stock price predictions

B) They ensure the reliability of financial statements

C) They enhance credit ratings

D) They prevent economic recessions

Answer: B) They ensure the reliability of financial statements

- Which substantive procedure is most useful for financial forecasting?

A) Revenue recognition testing

B) Trend analysis

C) Asset verification

D) Fraud detection

Answer: B) Trend analysis

- How do substantive audit procedures benefit investors?

A) By predicting future earnings

B) By verifying the accuracy of financial statements

C) By eliminating investment risks

D) By ensuring stock prices remain stable

Answer: B) By verifying the accuracy of financial statements

- What type of substantive procedure helps detect financial fraud?

A) Internal control assessment

B) Analytical procedures

C) Substantive testing of details

D) Budget variance analysis

Answer: C) Substantive testing of details

- Why do CFA professionals need to understand substantive audit procedures?

A) To assess financial statement accuracy

B) To prepare financial statements

C) To manage tax compliance

D) To execute mergers and acquisitions

Answer: A) To assess financial statement accuracy