The various forms of cost of capital are integral components in making financial decisions. Organisations must find out how expensive it has become to raise funds that can fund their operations. Cost of capital refers to the return that a company must earn to recover the cost of its sources of funding. Usually, the cost of capital consists of different forms, such as the cost of debt, equity, and retained earnings. These components help the companies decide on investment projects, capital budgeting, and financial strategies. Understanding the cost of capital in financial management helps make sound investment decisions, maximizing returns.

What is Cost of Capital?

The capital cost is the return the company must earn to cover the cost of using outside or internal funding. This is a yardstick to measure investment opportunities against what they hold regarding financial feasibility under the specific project consideration. Companies collect the required funds from external sources such as debt, equity, and retained earnings. Costs involved in Capital calculations include costs of each source of finance blended to obtain the weighted average cost of capital.

The cost of capital formula would enable businesses to evaluate the bare minimum required return on investment. Businesses that make a return higher than their cost of capital can create wealth, while anybody whose return is lower will reduce wealth. The measurement of capital cost is essential for businesses that are planning long-term financial decisions.

Weighted average cost of capital is one of the most commonly used methods of calculating the cost of capital, as it considers the proportion of that specific funding source. In addition, firms will compare the price of capital vs the discount rate to determine whether the investment decisions meet the financial expectations.

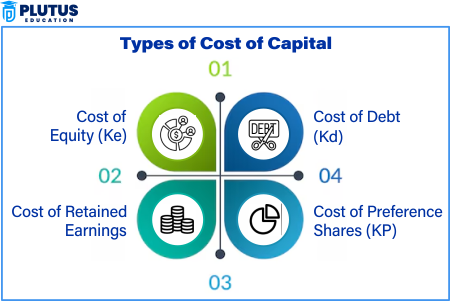

Types of Cost of Capital

The cost of capital for a company consists of different components. The significant types of capital costs are debt, equity, and retained earnings. However, Each component has advantages and disadvantages that organizations must weigh when planning their capital structures.

Cost of Debt (Kd)

The cost of debt is the cost a company bears on borrowing money. It consists of interest payable to lenders and other related financing charges. However, firms generally prefer debt financing because of tax treatment on financial charges, although excessive debt increases financial risk.

Debt financing includes loans, bonds, and credit facilities. They must assess good terms of debt before they decide to borrow. An organisation with too much debt could be unable to keep its repayment obligations and fall into financial distress. However, moderate debt should help a company grow without diluting ownership.

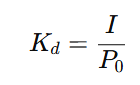

Cost of debt refers to an effective rate payable by a company over its borrowed funds.

Before-Tax Cost of Debt:

Where:

- Kd = Cost of debt

- I = Annual interest expense

- Po = Net proceeds from the debt issuance

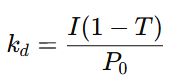

After-Tax Cost of Debt:

Where:

- T = Corporate tax rate

(Since interest expenses are tax-deductible, after-tax cost is lower.)

2. Cost of Equity

The cost of equity is the compensation for investors who give the firm equity capital by purchasing its stock. The cost of equity is greater than the cost of debt because equity investors assume a more significant risk than those who lend. Companies are permitted to raise equity capital by selling common or preferred stock.

Investors expect higher returns for providing funds as equity holders bear more risks than lenders. Equity financing does not require fixed payments like debt, but it does dilute ownership. Too much share issuance by the company would lead to existing shareholders being less able to control business decisions.

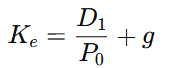

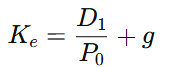

Dividend Discount Model (DDM):

Where:

- D1 = Expected dividend per share

- P0 = Current market price per share

- g = Growth rate of dividends

3. Cost of Retained Earnings

The cost of retained earnings is an expected return on reinvested profits. Companies do not pay interest or dividends on retained earnings, but they are required to provide these returns to the investors in that these returns could have been earned by those investors elsewhere.

Retained earnings are a critical source of internal finance for a company. Instead of distributing profits as dividends, companies reinvest them for expansion. However, if shareholders believe the reinvested funds will not generate high returns, they may prefer dividend payments.

Retained earnings are the opportunity cost of reinvesting profits instead of distributing them as dividends. It is often calculated as:

Factors Affecting Cost of Capital in Financial Management

The cost of capital, which is more or less expensive, determines the various factors affecting the price. The influencing factor(s) account for a lot in terms of the general finance strategy and the choice of sources for funding. Every consideration must, therefore, be given to these with a lot of scrutiny on the part of companies before they make any decisions related to finances.

Market Conditions

Market conditions attributed to its financial status are a primary determinant of capital costs. Under high interest rates, other factors remain the same, and the cost of debt would go up, making borrowing more expensive. In a downturn in the economy or when the stock market is unstable, equity costs may increase, impacting overall financial management.

Business Risk Profile

Arab companies having greater operational or financial risks would likewise add some cost into capital costs. Higher capital costs would more often than not mean increased rates of return expected from an investor due to the higher risk involved in investment. Conversely, lower capital costs belong to companies whose earnings remain stable and there is little to no debt at which they are financed.

Financial Structure

The capital structure, composed of debt, equity, and retained earnings, basically affects the cost of capital to the company. Excessive debt would result in high-interest payments, whereas excess equity financing leads to dilution of ownership, lowering earnings per share.

Creditworthiness and Ratings

High Ratings High credit ratings result in lower borrowing costs for the organization. Other than that, lenders and investors carry the firm’s financial strength record along with their consideration for the capital. These corporations will be burdened with paying higher interest with stricter lending terms before gaining access to the capital rendered by lending institutions. This would thereby increase the cost of capital to such firms.

Tax Rates

Affecting the cost of debt and thus overall capital costs, the tax system is at play in such a framework. Interest on debt is tax-deductible, which means a reduced effective cost of debt. Nonetheless, changes in tax laws or regulations will modify the financial plan, thereby contributing in one way or another to the increased cost of funding.

Trends in Industry and Economy

The industry under which a firm operates affects the cost of capital; in highly volatile and uncertain sectors, firms are expected to pay higher capital costs. Economic trends like inflation, recession, or growth cycles also affect financing options and expenses.

Relevance to ACCA Syllabus

Relating to the ACCA syllabus, types of capital costs can be essential in financial management and strategic decisions. This topic is addressed within the Financial Management (FM) and Advanced Financial Management (AFM) papers. They need to understand how the company determines its cost of equity, cost of debt, and WACC to make relevant investment and financing decisions.

Types of Cost of Capital ACCA Questions

Q1. What does the Weighted Average Cost of Capital (WACC) represent?

A) The rate at which a firm borrows funds only

B) The average return required by all investors in a company

C) The cost of debt financing only

D) The return required only by equity holders

Ans: B) The average return required by all investors in a company

Q2. If a firm finances a project with retained earnings, which cost of capital should it consider?

A) Cost of debt

B) Cost of preferred stock

C) Cost of retained earnings

D) Risk-free rate

Ans: C) Cost of retained earnings

Q3. Which factor is adjusted for the cost of debt when computing WACC?

A) Operating profit

B) Tax rate

C) Dividend yield

D) Liquidity ratio

Ans: B) Tax rate

Q4. Which of the following methods is commonly used to calculate the cost of equity?

A) Gordon Growth Model

B) Price-to-Earnings Ratio

C) Debt-to-Equity Ratio

D) Dividend Payout Ratio

Ans: A) Gordon Growth Model

Q5. What is the impact of increasing financial leverage on WACC, assuming debt is cheaper than equity?

A) WACC increases

B) WACC decreases

C) WACC remains constant

D) WACC is unaffected by financial leverage

Ans: B) WACC decreases

Relevance to US CMA Syllabus

In the US (Certified Management Accountant) CMA syllabus, the cost of capital is an essential topic in Financial Decision Making. CMA professionals must assess financing alternatives, calculate WACC, and make capital budgeting decisions based on the cost of debt and equity.

Types of Cost of Capital – US CMA Questions

Q1. What is the cost of capital measured for a firm?

A) The profitability of the company

B) The interest rate charged by banks

C) The required return to finance investments

D) The total cost of production

Ans: C) The required return to finance investments

Q2. When calculating WACC, which source of financing is generally considered the most expensive?

A) Debt

B) Equity

C) Preferred Stock

D) Retained Earnings

Ans: B) Equity

Q3. What happens to the cost of equity if the risk-free rate increases?

A) It decreases

B) It remains the same

C) It increases

D) It depends on the level of leverage

Ans: C) It increases

Q4. If a company’s capital structure shifts towards more debt financing, what happens to its financial risk?

A) It decreases

B) It increases

C) It remains unchanged

D) It depends on interest rates

Ans: B) It increases

Q5. Why is the cost of debt lower than the cost of equity?

A) Debt holders have a higher risk than equity holders

B) Debt interest payments are tax-deductible

C) Companies issue debt more frequently

D) Debt has no risk premium

Ans: B) Debt interest payments are tax-deductible

Relevance to US CPA Syllabus

In the US (Certified Public Accountant) CPA syllabus, the cost of capital is relevant in Financial Management and Business Environment & Concepts (BEC). CPAs must understand WACC, financial leverage, and investment valuation to guide corporate financial strategies.

Types of Cost of Capital – US CPA Questions

Q1. Which of the following is an example of a firm’s cost of capital?

A) The cost of goods sold

B) The weighted average return required by investors

C) The net income after dividends

D) The operating expense ratio

Ans: B) The weighted average return required by investors

Q2. Which factor influences a company’s cost of equity the most?

A) Corporate tax rate

B) Dividend policy

C) Market risk premium

D) Inventory turnover

Ans: C) Market risk premium

Q3. A company raises capital by issuing new shares. This cost of equity is known as:

A) Retained earnings cost

B) Flotation cost

C) External equity cost

D) Internal rate of return

Ans: C) External equity cost

Q4. What is the relationship between capital structure and cost of capital?

A) Higher debt financing decreases WACC initially

B) Higher equity financing always reduces WACC

C) Debt and equity financing have no impact on WACC

D) More debt increases WACC permanently

Ans: A) Higher debt financing decreases WACC initially

Q5. What does the Capital Asset Pricing Model (CAPM) help determine?

A) The cost of equity

B) The cost of debt

C) The firm’s liquidity ratio

D) The asset turnover ratio

Ans: A) The cost of equity

Relevance to CFA Syllabus

The CFA (Chartered Financial Analyst) syllabus covers the cost of capital under Corporate Finance. CFA candidates must evaluate capital structure, estimate required returns, and assess investment risk in financial markets.

Types of Cost of Capital – CFA Questions

Q1. Which of the following is the Capital Asset Pricing Model (CAPM) used to estimate?

A) The cost of debt

B) The cost of equity

C) The company’s net profit margin

D) The total revenue of the firm

Ans: B) The cost of equity

Q2. What does Beta represent in the CAPM formula?

A) Market return

B) Risk-free rate

C) Systematic risk

D) Dividend yield

Ans: C) Systematic risk

Q3. Why is the risk-free rate used in cost of equity calculations?

A) To represent the return on government bonds

B) To estimate interest expenses

C) To determine the dividend payout ratio

D) To calculate operating leverage

Ans: A) To represent the return on government bonds

Q4. What is the primary assumption behind using WACC in valuation?

A) The capital structure remains constant

B) Interest rates will always decline

C) Debt financing is riskier than equity financing

D) Equity financing has no cost

Ans: A) The capital structure remains constant

Q5. In financial modelling, the cost of capital is primarily used for:

A) Forecasting product sales

B) Evaluating investment projects

C) Managing supply chain efficiency

D) Calculating working capital requirements

Ans: B) Evaluating investment projects