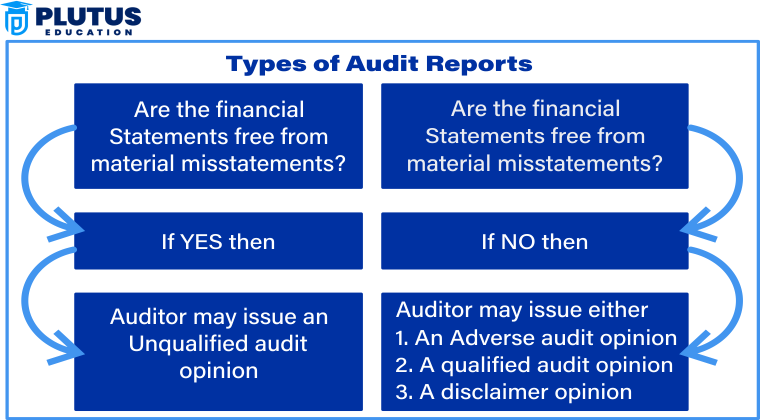

An unmodified opinion is the best assurance the independent auditor could give concerning a company. It states that the financial statements are free from material misstatements and present the company’s financial position and performance concerning accounting standards fairly, in all material respects. This opinion assures the investors, regulators, and stakeholders that the financial information is being presented relatively and is free from material misstatement. An audit of that nature conveys the most high opinion that the organization would receive regarding the auditor reflecting strength in areas of financial integrity, transparency, and compliance with relevant industry standards.

Unmodified Opinion

An unmodified opinion is given when the auditor, having examined a company’s financial statements, finds that these statements present an accurate and fair view of the state of affairs in all material respects per the applicable financial reporting framework. This means that the financial statements are set out by Generally Accepted Accounting Principles (GAAP) or the International Financial Reporting Standards (IFRS), thereby lending transparency and credibility to the stakeholders.

Unmodified Opinion vs Modified Opinion

An unmodified opinion is the best opinion issued by an auditor in terms of the outcome for the audited company. It says that the financial statements are free from material misstatement and conform to applicable accounting standards. Therefore, it is a fair presentation of the company’s financials to its stakeholders.

The auditors perform an in-depth examination of the financial statements of an entity. They lay on an independent viewpoint dictating an assurance level on the numbers. An unmodified opinion is thus an independent judgment on the conditions of an entity and its financial position.

An independent evaluation of financial statements is crucial for investors and lenders. They base their decisions on this truthful appraisal. An unmodified opinion earns trust and credibility in the company’s market.

| Feature | Unmodified Opinion | Modified Opinion |

| Meaning | Financial statements are correct and fair | Errors or misstatements are present |

| Compliance | Follows accounting standards | Deviates from standards |

| Investor Confidence | High | Lower than unmodified opinion |

| Auditor’s Assurance | Positive | Cautionary |

| Financial Impact | Builds trust | Raises concerns |

To receive an unmodified opinion is one way of realising the reputation a company desires. A neutral review reflects fair treatment of audits on financial statements. Without exceptions, if the auditor finds evidence of an issue, they will issue a modified opinion that may affect investors’ trust.

Real-Life Examples of Unmodified Opinions in Audits

Unmodified opinion is commonplace for companies that keep clean records. Here, auditors extract data from financial statements for an expert appraisal. Real-world examples are as follows:

Example 1: Big Companies

XYLimiteded, a multinational, has a very stringent accounting policy under which it submits complete financial records covering all expected accounts to its auditor. Following an independent assessment, the auditor will approve or present an unmodified opinion, which increases investor confidence and boosts stock prices.

Example 2: Government Organizations

Undergoing audits are conducted annually, and the auditors will scrutinise all transactions. Because the agency follows the directives regulating financial activity, it is therefore granted an unmodified opinion by the auditors. Thus, public trust is ensured and transparency maintained.

Example 3: Public Companies

A public company is fiduciary in supplying accurate information and financial reports. If the auditor gives no significant problems, the auditor can issue an unmodified opinion. Thus, investors can depend on this neutral judgment before making financial decisions. These examples have shown that unmodified opinion is a reflection of the moral values of the company. It states the financial statements and then says they are accurate and fair.

Why Auditor Gives Unmodified Opinion?

The auditor’s examination brings out charging for an unmodified opinion. That financial records are complete and accurate. Factors held by auditors are:

- Compliance with the Accounting Standards

- The financial statements have to comply with either IFRS or GAAP accounting rules.

- Precision of Financial Data

- Correct accounting must accompany every transaction.

Internal Controls

A company must have a sound system of checks and balances to stop fraud. Under all these circumstances, an independent opinion will offer an insight into a company’s financial aspect. It would work toward providing a good name for the companies that receive it in the market.

- No Significant Misstatements

- Material misstatements are not in the financial reports.

- Proper Information Disclosure

- All necessary financial disclosures must be provided.

Affect of Unmodified Opinion

An unmodified opinion directly relates to the financial statements and some decisions made by investors. Simply put, an unmodified opinion asserts that the financial information about a company is exact. Attract investors to a company with an unmodified opinion. Investors have faith in financial reports and can make informed decisions based on this opinion while enhancing its image.

Impact on Financial Statements

- To ensure the proper prescription of financial data

- Increases accountability and transparency

- Shows good governance and financial stability

Investor Impact

- Increases trust in performance

- Encourages funds investment and new partnerships

- Lowers financial fraud risk

Relevance to ACCA Syllabus

Unmodified opinion is a key concept in ACCA’s auditing syllabus, including the Audit & Assurance (AA) and Advanced Audit & Assurance (AAA). It ensures that the students understand the conditions under which an auditor gives a clean opinion to financial statements. This knowledge further helps ACCA candidates assess audit risks, evaluate financial reports, and ensure compliance with regulatory standards.

Unmodified Opinion ACCA Questions

- When an auditor issues an unmodified opinion, it means that:

A) The financial statements contain material misstatements

B) The financial statements are free from material misstatements and fairly presented

C) The auditor was unable to obtain sufficient audit evidence

D) The auditor disagrees with management on accounting policies

Answer: B) The financial statements are free from material misstatements and fairly presented

- Which of the following is a key requirement for issuing an unmodified opinion?

A) The financial statements comply with applicable accounting frameworks

B) The auditor has detected fraud and reported it

C) The auditor has no responsibility for misstatements

D) The auditor provides financial advice to the company

Answer: A) The financial statements comply with applicable accounting frameworks

- Under which of the following circumstances would an auditor issue an unmodified opinion?

A) The company has failed to maintain proper accounting records

B) The financial statements are prepared in compliance with IFRS and contain no material misstatements

C) The auditor has identified material misstatements but ignored them

D) The financial statements contain errors that significantly impact users’ decisions

Answer: B) The financial statements are prepared in compliance with IFRS and contain no material misstatements

- Which standard guides forming an unmodified audit opinion?

A) IFRS 15

B) ISA 700

C) GAAP 501

D) IAS 16

Answer: B) ISA 700

- What is the primary purpose of an auditor’s report containing an unmodified opinion?

A) To express doubts about management’s ability

B) To assure investors of future profitability

C) To confirm that financial statements provide an accurate and fair view

D) To highlight material fraud detected

Answer: C) To confirm that financial statements provide an accurate and fair view

Relevance to US CMA Syllabus

The (Certified Management Accountant) CMA syllabus emphasises external financial reporting and the role of auditors in ensuring financial integrity. Understanding unmodified opinions helps CMAs interpret financial statements and assess external audits for internal financial decision-making.

Unmodified Opinion CMA Questions

- What does an unmodified opinion in an audit report indicate?

A) The company has achieved financial success

B) The financial statements present an accurate and fair view

C) The auditor has identified internal control deficiencies

D) The company has no financial risks

Answer: B) The financial statements present an accurate and fair view

- Who is responsible for issuing an unmodified opinion on financial statements?

A) Chief Financial Officer (CFO)

B) Internal Auditor

C) External Auditor

D) Board of Directors

Answer: C) External Auditor

- Which of the following is NOT a reason for issuing an unmodified opinion?

A) The financial statements comply with GAAP

B) There is sufficient and appropriate audit evidence

C) There are material misstatements in the financial statements

D) The audit procedures have been performed as per standards

Answer: C) There are material misstatements in the financial statements

- Which regulatory body oversees the audit profession in the US to ensure proper issuance of audit opinions?

A) IFRS Foundation

B) Securities and Exchange Commission (SEC)

C) Public Company Accounting Oversight Board (PCAOB)

D) Financial Accounting Standards Board (FASB)

Answer: C) Public Company Accounting Oversight Board (PCAOB)

- An auditor provides an unmodified opinion when the financial statements are:

A) Incomplete but reliable

B) Free from material misstatements

C) Showing positive financial results

D) Based on management’s estimates alone

Answer: B) Free from material misstatements

Relevance to US CPA Syllabus

The Certified Public Accountant (CPA) exam covers auditing in the AUD (Auditing & Attestation) section. It requires candidates to understand audit reports, including unmodified opinions, to ensure accurate financial reporting and compliance with GAAP and PCAOB regulations.

Unmodified Opinio CPA Questions

- Which type of audit opinion states that the financial statements present a fair and accurate view?

A) Qualified opinion

B) Adverse opinion

C) Unmodified opinion

D) Disclaimer of opinion

Answer: C) Unmodified opinion

- What is the key requirement for issuing an unmodified opinion?

A) Financial statements are materially misstated

B) Financial statements are free from material misstatements

C) The auditor disagrees with management’s estimates

D) The company has a weak internal control system

Answer: B) Financial statements are free from material misstatements

- Under which circumstances would an auditor NOT issue an unmodified opinion?

A) The financial statements comply with GAAP

B) The company lacks proper financial disclosures

C) The audit evidence is sufficient and appropriate

D) There are no material misstatements in the statements

Answer: B) The company lacks proper financial disclosures

- Which of the following standards governs the auditor’s report in the US?

A) IFRS 9

B) PCAOB AS 3101

C) IAS 36

D) GAAP 502

Answer: B) PCAOB AS 3101

- What does an unmodified opinion assure investors?

A) The company is free from financial risk

B) The financial statements are fairly presented

C) The company will be profitable in the future

D) The auditor guarantees the financial results

Answer: B) The financial statements are fairly presented

Relevance to CFA Syllabus

The Chartered Financial Analyst (CFA) program includes financial statement analysis, making audit opinions crucial for investment decisions. Understanding unmodified opinions helps CFAs assess a company’s credibility and economic health.

Unmodified Opinion CFA Questions

- Why is an unmodified opinion important for investors?

A) It guarantees future profitability

B) It indicates the company has good governance

C) It confirms that financial statements are free from material misstatements

D) It predicts stock market trends

Answer: C) It confirms that financial statements are free from material misstatements

- Which type of audit opinion is most desirable for stakeholders?

A) Adverse opinion

B) Qualified opinion

C) Unmodified opinion

D) Disclaimer of opinion

Answer: C) Unmodified opinion

- How does an unmodified opinion affect financial statement analysis?

A) It ensures statements are reliable for decision-making

B) It increases company profits

C) It eliminates financial risks

D) It replaces internal audits

Answer: A) It ensures statements are reliable for decision-making

- Which auditing standard supports the issuance of unmodified opinions under IFRS?

A) IAS 1

B) ISA 700

C) IFRS 9

D) GAAP 304

Answer: B) ISA 700

- An unmodified opinion does NOT mean that:

A) The financial statements are fairly presented

B) The auditor guarantees financial success

C) The audit was conducted according to standards

D) There are no material misstatementsAnswer: B) The auditor guarantees financial success