A capital rationing problem is most likely when a firm has to select the investment projects it would undertake, given its limited finances. Though many investment opportunities exist, some cannot be financed as budgets impose constraints. In such a case, the firm is supposed to pick investments that can return high attention to capital. Thus, capital rationing obtains maximum returns through the best possible utilization of limited resources. This concept finds widespread application in capital investments and rationing, bringing better reasoning for companies in finance matters. Knowledge of capital rationing in finance allows firms to run investment portfolios while being aware of uneconomic risks.

An example of capital rationing can be understood in a company having $1 million for investment with project proposals worth $2 million. Since the company cannot finance all projects, it must select the most profitable ones using capital rationing techniques. This becomes critical to finance management, whereby such a process will facilitate business in effectively using resources with a minimum risk attached.

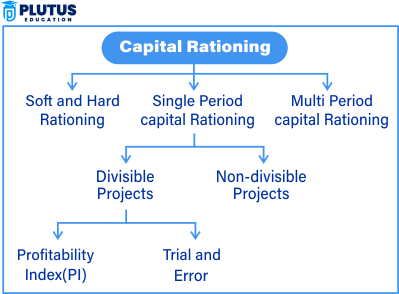

Types of Capital Rationing

Capital rationing is broadly invoked to advise financial decision-making and is intended to regulate how companies allocate limited funds across various investment opportunities. Two main types of capital rationing are considered: hard and soft capital rationing. Making an informed investment decision necessitates a good understanding of these two. The investment decision a company makes, and its financial stability is contingent upon the type of capital rationing it has adopted.

Hard and Soft Capital Rationing

A hard capital rationing situation would be one where considering outside factors fetters the company’s ability to raise funds. Such considerations may include high interest rates, depression, or even the unwillingness of investors. The firm could not afford to go out of limited capital in the face of hard capital rationing. Hard capital rationing will also have very selective investing decisions, targeting only projects that promise high returns.

Soft capital rationing happens when a company should restrict investments to mitigate different internal risks associated with its operations. The company may decide to limit new investments due to internal policies even when these investments are financed in principle. Such a view ensures that investment is made in a disciplined fashion and that unnecessary future financial obligations are avoided.

Capital Rationing Problems and Solutions

Arguably, capital rationing problems provide a formidable challenge to companies whose investment decisions are affected. Among the common challenges are the following:

Limited Investment Capital

The limitation of investment capital is the major problem of capital rationing. At any point in time, there could be several prospective investment opportunities, but due to capital budget limitations, the firms can finance only a small number of them.

Difficulty in Project Selection

With limited funds, choosing the right investment project may become a problem. Companies must rely on capital budgeting techniques such as Net Present Value (NPV), Internal Rate of Return (IRR), and Profitability Index (PI) to determine which projects will get funded.

High Cost of Capital

The cost of obtaining funds through loans or equity is high. If interest rate levels are high or business conditions are deemed unfavorable, raising funds goes against the companies’ wishes and limits other investment opportunities.

Risk and Uncertainty

Investing in new projects poses possible financial risks. Companies may face difficulty determining future cash flows, leading to uncertainty concerning the decision.

Conflict Between Short-Term and Long-Term Goals

Companies frequently find themselves at a crossroads between short-term profitability and long-term investment growth: some projects provide quick returns but are not aligned with long-term strategic thrusts.

Management-Imposed Restrictions

With soft capital rationing, businesses may find the management refusing to sanction any investment, even one that is necessary. Management policies may impose limits on expansion opportunities, impacting long-term profitability.

Solutions for Capital Rationing

Corporations have a set of strategies that could be deployed for capital rationing problems, with a view of maximizing the revenues or investment within the limits imposed.

Priority to Projects with Higher Returns

Companies have to invest some funds in projects that will earn them returns. This can be achieved by establishing ranks of different investment opportunities based on profitability using NPV, IRR, and PI.

Application of Capital Rationing Techniques

A company can apply any capital rationing technique to analyze investments before making decisions based on the profitability Index (PI), which measures project profitability concerning investment amounts. Net Present Value (NPV) measures future cash flows to be converted into their present values; Internal Rate of Return (IRR) provides the required rate of return that is viewed as the reak-even of these measures.

Sourcing Alternative Financing

Companies may explore alternative funding sources for capital constraints. For example, Venture capital or private equity Capital market securities such as bonds or shares Negotiate better terms of loans with the banks.

Cash Management at the External Level

Proper financial planning creates checks on how the available cash is utilized. This helps in the improvement of cash management within the business by reducing unnecessary expenses,; optimizing working capital, Reinvestment of profits strategically,

Adopting Balanced Investments

Companies should not only invest in short-term investments. Still, they should balance this investment with long-term investments, with sustainable growth being one of the greatest keys to avoiding potential instabilities that can lead to financial instabilities.

Revisiting Capital Rationing Decisions Regularly

Regularly reviewing investments allows companies to realign investments in a changing environment with time. Capital rationing procedures should be periodically examined to optimize the firm’s financial performance.

These should help business organizations overcome capital rationing-related challenges and introduce effective management of finances.

Techniques in Capital Rationing

They include various selection techniques that help organizations develop the best investment projects. These methods can be used to assess the viability of any particular project against capital rationing criteria and to ensure the proper effective use of capital resources. With such capital rationing techniques, it is possible to ensure that investments are made in those projects that can yield the highest financial constraints.

Profitability Index (PI)

One very prevalent capital rationing technique is the profitability index. Using it is standard because it measures the profit a particular project can generate over a period divided by the initial investment. PI .gt;1 denotes profitable periods ahead while PI, one less period ahead, denotes it may be a poor project to pursue.

Net Present Value (NPV) Per Unit of Investment

Net Present Value (NPV) is a concept that utilizes future cash flow and puts its values in the recent term. It is beneficial to a business entity. It is calculated for all companies when considering limited capital. Therefore, it would be the dollar amount invested, generally determining which projects rank highest in per-dollar value.

Internal Rate of Return (IRR) Ranking

The other important reckoning technique for ranking an investment project is the Internal Rate of Return (IRR). It refers to the rate at which a project breaks even. Projects are thus preferred based on the highest IRR according to the principle of rationing capital.

Capital Rationing Investment Appraisal

Investment Appraisal will evaluate any project based on financial and non-financial factors. A corporation can make an informed investment decision by analyzing the cash flows, risk factors, or strategic importance from the enterprise’s perspective.

Relevance to ACCA Syllabus

Capital rationing is essential in ACCA’s Financial Management (FM) and Advanced Financial Management (AFM) papers. It allocates limited financial resources to investment projects while maximizing shareholder value. Understanding capital rationing helps ACCA candidates analyse project viability using techniques such as Net Present Value (NPV) and Internal Rate of Return (IRR), which are crucial for making strategic investment decisions under financial constraints.

Capital Rationing Problems and Solutions ACCA Questions

Q1: What is capital rationing in the context of investment decision-making?

A) The process of issuing more shares to finance new projects

B) The limitation on the amount of funds available for investment

C) A method of ensuring all projects receive equal funding

D) A way to increase debt financing for expansion

Ans: B) The limitation on the amount of funds available for investment

Q2: When a company faces capital rationing, which technique is most appropriate for selecting projects?

A) Payback Period

B) Accounting Rate of Return (ARR)

C) Net Present Value (NPV) per unit of investment

D) Gross Profit Margin

Ans: C) Net Present Value (NPV) per unit of investment

Q3: In capital rationing scenarios, which type of project ranking approach is commonly used?

A) IRR ranking without capital constraints

B) Profitability Index (PI) ranking

C) FIFO method of project selection

D) Maximizing total investment without considering constraints

Ans: B) Profitability Index (PI) ranking

Q4: Which of the following is a possible reason for capital rationing?

A) Unlimited access to external financing

B) Economic downturn reducing available capital

C) A company deciding to lower costs through increased investment

D) An increase in tax incentives for significant investments

Ans: B) Economic downturn reducing available capital

Q5: In soft capital rationing, what restricts investment decisions?

A) Government-imposed credit limits

B) Internally imposed constraints by management

C) Bank-imposed lending restrictions

D) A lack of profitable investment opportunities

Ans: B) Internally imposed constraints by management

Relevance to US CMA Syllabus

The US CMA syllabus covers capital rationing in the Strategic Financial Management section. It helps candidates understand how firms allocate scarce capital resources among competing projects. Capital budgeting decisions, including evaluating investment opportunities using NPV, IRR, and Profitability Index, are central to corporate finance and financial strategy in the CMA examination.

Capital Rationing Problems and Solutions US CMA Questions

Q1: In capital budgeting, what is the primary goal when dealing with capital rationing?

A) Maximizing project selection based on qualitative factors

B) Selecting projects with the highest total revenue

C) Allocating funds to projects that maximise shareholder wealth

D) Investing in all projects with a positive NPV

Ans: C) Allocating funds to projects that maximise shareholder wealth

Q2: Which financial metric is most helpful in ranking projects under capital rationing constraints?

A) Earnings Before Interest and Taxes (EBIT)

B) Net Present Value (NPV) per unit of investment

C) Depreciation Expense

D) Payback Period

Ans: B) Net Present Value (NPV) per unit of investment

Q3: If a company imposes its investment limits rather than external restrictions, which type of capital rationing is it facing?

A) Hard capital rationing

B) Soft capital rationing

C) Absolute capital limitation

D) Flexible capital management

Ans: B) Soft capital rationing

Q4: How does the Profitability Index (PI) help in capital rationing decisions?

A) It ranks projects based on IRR rather than investment cost

B) It measures the present value of cash inflows per unit of investment

C) It determines payback period efficiency

D) It assesses past project profitability

Ans: B) It measures the present value of cash inflows per unit of investment

Q5: Why is the profitability index (PI) often preferred over the payback period in capital rationing?

A) PI considers the time value of money and maximises returns

B) The payback period accounts for profitability more effectively

C) PI ignores cash flow uncertainties

D) The payback period is more accurate for long-term projects

Ans: A) PI considers the time value of money and maximises returns

Relevance to CFA Syllabus

Capital rationing is a significant topic in CFA’s Corporate Finance and Investment Analysis sections. The CFA focuses on firms making optimal investment decisions under financial constraints. Candidates learn about project selection using NPV, IRR, and PI, which are essential for portfolio management, valuation, and corporate decision-making.

Capital Rationing Problems and Solutions CFA Questions

Q1: How does capital rationing affect corporate investment decisions?

A) It ensures firms invest in all projects with positive IRR

B) It forces firms to choose projects within financial constraints

C) It removes the need for project ranking

D) It allows unrestricted external borrowing for investments

Ans: B) It forces firms to choose projects within financial constraints

Q2: Which financial metric is most helpful in evaluating projects under capital rationing?

A) Earnings Per Share (EPS)

B) Net Present Value (NPV) per dollar invested

C) Quick Ratio

D) Market Capitalization

Ans: B) Net Present Value (NPV) per dollar invested

Q3: If a firm cannot raise additional capital due to external financing restrictions, which type of capital rationing is it experiencing?

A) Soft capital rationing

B) Hard capital rationing

C) Internal capital rationing

D) Absolute project limitation

Ans: B) Hard capital rationing

Q4: Why is Net Present Value (NPV) per unit of investment used in capital rationing situations?

A) It ensures that only large projects are selected

B) It measures investment efficiency with limited capital

C) It ignores the cost of capital

D) It focuses only on revenue generation

Ans: B) It measures investment efficiency with limited capital

Q5: Which capital budgeting technique is most useful when selecting multiple projects under financial constraints?

A) Payback Period

B) Internal Rate of Return (IRR)

C) Profitability Index (PI)

D) Dividend Discount Model (DDM)

Ans: C) Profitability Index (PI)

Relevance to US CPA Syllabus

Capital rationing is covered in the US CPA syllabus under Financial Management and Managerial Accounting. CPA candidates must understand how businesses allocate capital to projects using financial metrics like NPV, IRR, and PI. Capital budgeting principles are essential in decision-making for corporate finance and strategic management.

Capital Rationing Problems and Solutions US CPA Questions

Q1: What is the primary purpose of capital rationing in corporate finance?

A) To select projects that provide the highest ROI under limited capital

B) To invest in all available projects regardless of constraints

C) To ensure equal distribution of funds among all projects

D) To maximise tax deductions through project investment

Ans: A) To select projects that provide the highest ROI under limited capital

Q2: Which method is most commonly used in capital rationing for ranking projects?

A) Payback Period

B) Net Present Value (NPV) per unit of investment

C) Gross Profit Margin

D) Accounts Payable Turnover

Ans: B) Net Present Value (NPV) per unit of investment

Q3: A company facing hard capital rationing is likely experiencing which of the following?

A) Internal budget limitations imposed by management

B) Market-driven restrictions on external financing

C) A lack of suitable investment opportunities

D) Over-reliance on retained earnings

Ans: B) Market-driven restrictions on external financing

Q4: When facing capital rationing, how should a company prioritise projects?

A) By selecting projects with the shortest payback period

B) By ranking projects using the Profitability Index (PI)

C) By choosing projects that have the highest book value

D) By considering projects with the lowest risk

Ans: B) By ranking projects using the Profitability Index (PI)

Q5: What is a key assumption when using NPV for capital rationing decisions?

A) Cash flows are reinvested at the cost of capital

B) Projects must have an equal lifespan

C) External financing is unlimited

D) Tax benefits are ignored

Ans: A) Cash flows are reinvested at the cost of capital