Internal control is the processes and procedures established by an organization to assure the accuracy of financial reporting, adherence to laws, and effective operations. The characteristics of internal control are the essential elements that make an internal control system of a company effective in addressing risks, maintaining compliance, and protecting assets. Internal control means management’s policies, procedures, and systems to avoid fraud, identify errors, and achieve operating efficiency. An effective internal control system enables firms to be accurate in their financials and comply with regulations.

What is Internal Control?

Internal Control is the mechanism of an organization’s policies, procedures, and processes to ensure accurate financial reporting, risk management, and regulatory compliance. It assists companies in avoiding fraud, detecting mistakes, and streamlining operations. That tells you that internal controls exist and work at every aspect of an organization, from financial transactions to operational procedures.

Components of Internal Control (COSO Framework)

The Committee of Sponsoring Organizations of the Treadway Commission (COSO) has a framework that identifies five components of internal control:

- Control Environment: A control environment establishes the basis of internal control in a particular organization. These encompass management’s integrity, ethical values, and adherence to compliance. A robust control environment promotes accountability and trust management, which should demonstrate why everyone must follow the procedures (and policies) put in place.

- Risk Assessment: Risk assessment identifies and analyzes potential risks that threaten financial reporting and business operations. It’s a process that assists organizations in prioritizing risks and creating a plan to manage them. Understanding internal and external threats can help companies plan for challenges before they impact operations. This ensures that risks are proactively managed to mitigate their impact.

- Control Activities: These are the policies and procedures to mitigate these risks. Examples of such controls are authorization controls and segregation of duties to reduce the risk of fraud or errors. These activities allow the organization to operate efficiently and by defined guidelines. Control activities protect assets from misuse while ensuring compliance with laws, regulations, and other standards.

- Monitoring Activities: Monitor ongoing evaluations and periodic audits to ensure internal controls work effectively. Periodic reviews aid in detecting where controls require enhancement. They also help check that the organization stays within the framework of its legal regulations and adjusts due to changes. Continuous monitoring ensures that internal controls remain effective over time.

- Information and Communication: Information and communication facilitate the smooth flow of information necessary for decision-making across the organization. Access to accurate, up-to-date data is vital for employees to carry out their roles effectively. Open communication helps the departments to coordinate, solve problems, and increase business productivity. This also encourages transparency, enabling all levels of the organization to make informed decisions.

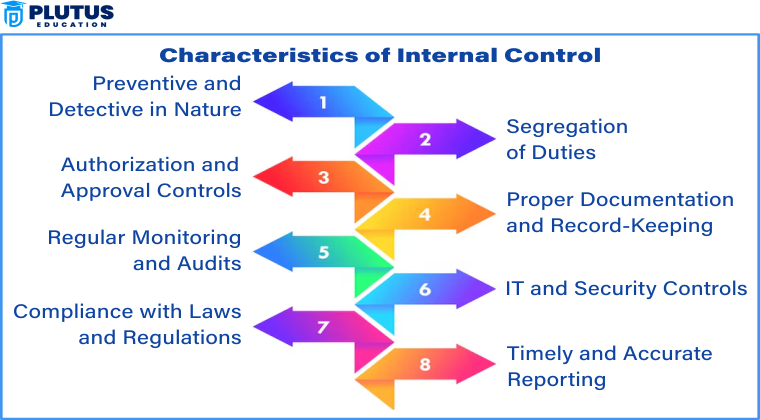

Characteristics of Internal Control

It has to possess certain essentials to make a good internal control system. The following is a list of essential features of internal control:

Preventive and Detective in Nature

Two primary purposes of internal controls are to prevent errors and fraud before they occur (preventive) and to detect errors and fraud when they do occur (detective). Preventive controls might need both a payor and payee approval for large transactions to prevent unauthorized payments, while detective controls are to catch errors or fraud after the fact.

Segregation of Duties

Segregation of duties requires that more than one person must approve all financial transactions; one person prepares the transaction, and another person approves it. Such a practice minimizes the chances of fraud or errors. For instance, in some organizations, there is a separation between payroll processing and payroll approval. This segregation of duty can prevent a single employee from altering accounting records for their own benefit.

Authorization and Approval Controls

The internal control systems require that the proper authority authorizes every financial transaction before it is executed. It helps to avoid unauthorized spending and allows only authorized expenses. For example, if any purchase order that is above ₹50,000 may require a manager’s approval before the order is processed to those who want financial oversight.

Proper Documentation and Record-Keeping

One of the basic points of internal control is documentation for all transactions. That means there is a paper trail for verification and accountability. For instance, businesses need to maintain supplier invoices and bank statements that provide evidence of purchases and paid sums, and these invoices stored in a digital format can be beneficial during audits or just for future reference.

Regular Monitoring and Audits

When it comes to reducing the chances of fraud, the only thing that really helps is monitoring and conducting audits to ensure the internal control systems are working as they should be. Performing relatively frequent checks allows potential discrepancies or fraud to be detected in a timely manner, assuring the system is operating as intended. Internal auditors may review cash transactions on a monthly basis to determine compliance with internal policies and to identify any anomalies, for example.

IT and Security Controls

As digital transactions increase, internal controls must encompass cybersecurity and IT safeguards. For instance, access to financial software should be locked down based on job functions to prevent unauthorized access. The aim of these IT controls is to protect confidential data and restrict access to financial records and systems to authorized staff only.

Compliance with Laws and Regulations

Robust internal control systems help ensure an organization adheres to all applicable laws and regulations. These encompass things like tax, labor laws, and corporate governance obligations. Ensuring GST & TDS deductions and validating them before salary payments allows the company to comply with tax laws and avoid penalties against non-compliance.

Timely and Accurate Reporting

These reports help ensure financial transactions are reported correctly and promptly to facilitate organizational decision-making. One such process is that management should carefully review the quarterly financial statements to ensure that they have no errors before they are published, for instance, to ensure that the company’s financial reporting is accurate and transparent.

Internal Control Objectives

The internal control framework is underpinned by three objectives: financial reporting, operational efficiency, and compliance with regulations. Here is the internal control objectives detail:

Safeguarding Assets

The purpose of internal controls is to deter the reprehensible use or theft of an organization’s assets. This ensures financial stability by securing and monitoring organizations’ most valuable assets. To track the movement of the inventory and prevent unauthorized access, companies keep CCTV cameras in their warehouses. In addition to that, physical access systems used include employee ID cards that prevent who can physically enter sensitive areas, information, and records, protecting the organization’s assets.

Ensuring Accuracy of Financial Records

Prevent errors in accounting and financial statements. These controls are designed to ensure the accuracy of economic data, a cornerstone of decision-making. Monthly bank reconciliations, for example, help align accounting records with actual bank balances. In addition to saving time, automated accounting software minimizes human error and guarantees that financial reports are always accurate.

Compliance with Laws and Regulations

Internal controls help businesses adhere to corporate laws, tax regulations, and labor laws. This prevents legal fines and keeps the business’s name fresh. For instance, regular audits ensure the timely filing of tax returns, while checks for compliance with labor laws ensure workers’ rights are upheld. Compliance software can prevent future legal issues for businesses by helping them stay abreast of new or changed laws and regulations.

Operational Efficiency

Internal controls save businesses time by automating workflows, minimizing redundancy, and lowering costs. They help to improve processes and lead to increased productivity. To illustrate it better, automating payroll eliminates errors while paying salaries and saves time. Also, by introducing inventory management systems, products are tracked more efficiently, reducing waste and ensuring that supplies are always available when needed.

Risk Identification and Mitigation

Internal controls help organizations assess, monitor, and manage risks associated with fraud, financial misstatements, or operational failures. They are preventive; they help avoid grey swan events before they become black swans and inflict severe damage. Insurance policies, for instance, cover financial losses in the event of – well, accidents. Furthermore, risk management software makes analyzing real-time information about potential threats easier, helping businesses react fast accordingly.

Difference Between Internal Control & Internal Audit

Internal control refers to the processes established within an organization to help manage risks, ensure compliance with regulations, and promote efficiency. Internal control helps ensure fraud prevention and protection of assets, while internal audit assesses how adequate these controls are. To elaborate on the differences and how they operate within an organization, here are brief internal differences between different roles, responsibilities, definitions, and examples.

| Aspect | Internal Control | Internal Audit |

| Definition | A system of rules and procedures to manage risks and safeguard assets. | An independent function that evaluates and reports on internal controls. |

| Purpose | Prevents fraud, ensures financial accuracy, and improves efficiency. | Assesses and ensures the effectiveness of internal controls. |

| Responsibility | Management and employees implement internal controls. | Internal auditors evaluate and recommend improvements. |

| Example | Approving all purchases over ₹50,000 to prevent fraud. | Internal auditors reviewing if approval policies are followed. |

Internal Control FAQs

1. What is the main purpose of internal control?

Internal control aims to provide financial accuracy, avoid fraud, protect assets, and enhance operational effectiveness.

2. What are the five components of internal control?

The five elements are control environment, risk assessment, control activities, information and communication, and monitoring activities.

3. What is the difference between internal check and internal control?

Internal check is a procedure by which work is split between employees to avoid fraud, whereas internal control is a general system comprising policies, procedures, and surveillance.

4. Why is internal control important for a business?

Internal control assists businesses in avoiding fraud, ensuring financial accuracy, enhancing efficiency, and compliance with laws.

5. How is internal control different from internal audit?

Management puts Internal control in place to handle risks, and internal audit reviews and enhances internal controls independently.