CAATs or computer assisted audit techniques help auditors analyze financial data, detect fraud, and enforce compliance with regulations. They bring automation to audit processes, cutting down manual efforts while increasing accuracy. The computer-assisted audit techniques allow for the systematic examination of financial records, the identification of risks, and the enhancement of overall audit efficiency.

Traditionally, audits carried out sampling techniques, which may have sometimes resulted in a loss of focus on critical errors or fraudulent activities. The computer-assisted audit techniques allow auditors to analyze entire data sets rather than samples, enhancing accuracy and reliability. Since digital transactions have taken shape, software renaming computer-assisted audit techniques now plays a vital role in dealing with large volumes of financial data.

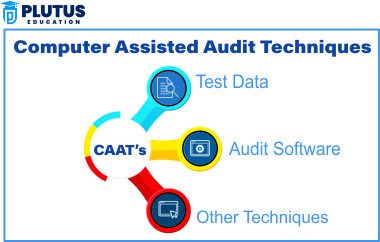

Computer Assisted Audit Technique

Computer-assisted audit techniques are software applications and automated tools that aid auditors in analyzing financial transactions and assessing risks. Computer-assisted audit techniques utilize specialized programs to process large amounts of data, increasing audit efficiency swiftly. They also enable auditors to spot trends indicating fraud or compliance with financial regulation.

Auditors apply these techniques for internal and external audits to achieve accurate and transparent financial reporting by reducing manual processes, thus decreasing human error and increasing audit reliability. The importance of computer-assisted audit techniques is the ability to handle complex managerial-type financial data and produce significant results for decision-making.

Basic Functions of CAAT

CAATS are the techniques for extracting, cleaning, and analyzing financial data from various sources. This ultimately reduces the duration of the audit completion. It solves the problems associated with manual intervention in data entry, which can lead to many human errors in the audit report generation process.

Manipulation of Evidence

Auditors employ fraud detection-CATTs to determine any unusual patterns of behaviour, duplicate transactions or otherwise questionable activities regarding financial transactions. This, therefore, provides a means of detecting fraud as soon as it occurs and equips auditors with a tool to take immediate action when such a thing happens.

Ensure Compliance

CAATs help auditors verify the compliance of financial records with financial regulations by checking the entry of road maps for these rules in corporations’ transactions. So, CAATs mitigate the risks of incurring penalties for economic offences.

Real-Time Monitoring

Some computer-assisted audit techniques software interface copies with company systems perpetually monitor financial activity. Such an undue incidence affords the auditor real-time monitoring of risk exposure.

Risk Assessment

CAATs help the auditors analyse the history of financial data to assess the likely exposures in the future and propose mitigating factors. Thus, they assist further in decision-making and enhancing financial security.

Characteristics of CAATs

Computer-assisted auditing techniques are among the most significant tools in today’s audit environment. These attributes maximize accuracy, speed, and transparency in the auditing process, thereby elevating the value of the entire auditing endeavour. They, therefore, facilitate the automation of complex auditing processes that provide for error detection and the prevention of financial mismanagement by various organizations. The major highlights of computer-assisted auditing techniques are:-

Data Extraction and Analysis

CAATs extract financial data from accounting systems, databases, and spreadsheets so that auditors can focus on analyzing transactions. Eliminating manual collection processes saves time and effort.

Pattern Recognition and Anomaly Detection

The algorithms intend to pick out unusual accounts, such as duplicate payments or unauthorized transactions. They thus facilitate a fraud inquiry before full-fledged losses.

Real-Time Auditing

Some CAATs will continuously monitor financial transactions to issue real-time audit reports. This is a significant feature, as it calls for the immediate recognition of errors and irregularities, minimizing risks.

Flexible Audit Parameters

The CAAT may be purposefully directed at specific financial risks, such as tax compliance or fraud. This affords flexibility in customizing the audit according to the business’s operational requirements.

Integration with Accounting Software

Most CAATs can integrate well with ERP systems, thus facilitating easy access for auditors to view the financial records. This assists in checking the quality of data for audit purposes, which, in turn, adds to its cost-effectiveness.

Examples of Computer-Assisted Audit Techniques

Different computer-assisted audit techniques will be applied for varying reasons within an audit concerning its objectives. These will assist auditors in collecting audit evidence regarding financial information, detecting possible fraud, or ensuring that applicable laws and regulations have indeed been complied with. The characteristics of the CAAT would vary with the level of complexity of the audit or the financial systems of the audited entity. Some common examples of CAATs are:-

- Generalized Audit Software: Gas software permits auditors to extract, analyze, and report financial information from various systems. The software allows auditors to identify inconsistencies and assess financial risks.

- Electronic Working Papers: These digital documents assist the auditor in organizing, storing, and reviewing audit findings, replacing paper-based records with efficiency in audit and environmentally friendly systems.

- Analyzing regression methods: These tools can handle trends in finance while predicting future performance. Any pattern that is outside the norm must indicate potential fraud or mismanagement.

- Automated Reconciliation Tools: Reconcile different sources like banks or internal accounting systems. The result is a financial statement that helps detect and assures accurate fraud detection.

- Continuous Auditing Systems: These systems monitor all that potentially qualifies in real-time as suspicious activity occurring in a transaction. Continuous auditing permits organizations to detect and prevent fraud.

Classification of CAATs

During the audit, entirely different types of computer-assisted audit techniques serve various purposes. Each type focuses on audit tasks, such as data validation, risk assessment, or fraud detection. Auditors adopt as many of them as possible into their audit process to have the most comprehensive audit result. The major types of CAATs are:-

Test Data Techniques

Auditors enter sample transactions into a company’s accounting system to check that it processes that data correctly. This technique checks that financial systems perform the way they ought to do.

Parallel Simulation

This processes similar financial data in two separate systems for the two results. If there are discrepancies, auditors follow the trail leading to the fraud/error.

Integrated Test Facility

An integrated test facility is a system whereby dummy transactions come into play to verify and validate the existing accounting system without worrying about real transactions. This helps the auditor establish correctness while the system’s operation continues without the routine’s interference.

Embedded Audit Modules

Such programs are used by auditors embedded in financial systems to monitor transactions for economic activity continuously. But they are also meant to raise alerts on suspicious transactions.

Data Mining Tools

Analyse inexhaustibly large datasets to identify patterns and anomalies. Auditors also perform data mining to detect fraudulent transactions and judge finances.

Advantages of Computer-Assisted Audit Techniques

These advantages make CAATs indispensable for improving audit efficiency from the very beginning in analysing accounts by ensuring that audits are completed time efficiently while maintaining financial accountability and compliance.

- Quicker Data Processing: CAATs analyse large amounts of data in just a few seconds, making auditors complete the audit time considerably shorter. All this is done while changing the focus from preparing all records to looking out for financial risks.

- Improved Accuracy: CAATs greatly reduce the possibility of human error in the audit, producing more accurate results. Consequently, this puts more reliability on financial reporting and fulfils the requirements of set regulations.

- Fraud Detection: CAATs detect irregular transactions and fraudulent activities in real time. Companies that are heavy on fraud prevention and asset protection employ these tools.

- Real-Time Monitoring: Some CAATs permit continuous auditing by observing financial transactions. This allows organisations to detect and respond to financial hazards rapidly.

- Better Compliance: Automated compliance checks guarantee that businesses follow their financial obligations. CAATs will backtrack the transaction against regulatory requirements, thus reducing any risks to legal penalties.

Challenges And Limitations

While the advantages of CAATs are significant, the disadvantages of computer-assisted audit techniques include their high implementation costs, technical challenges, and questions concerning data security. Organisations need to know these factors to get the most from CAATs.

- High Implementation Costs: Businesses will need to acquire audit software, specialised IT infrastructure, and training for their staff. These costs may stress small companies.

- Technical Complexity: Auditors require specialised training to apply CAATS. Without proper skills, the auditors may misinterpret the results or fail to detect errors.

- Cybersecurity Risk: Handling a substantial volume of financial data poses a risk of potential intrusions by cybercriminals; therefore, organisations need to implement stringent security controls to protect sensitive data.

- Other Problems Inclined to System Integration: Some CAATs may not be fully compatible with existing financial systems, and such tools may need to be customised to fit the business environment.

- Over-reliance on the Auto-eye: CAATs are sharp tools for increasing efficiency; however, judgment will always remain essential. Results produced by the automated systems will have to be verified by the auditors for the correct conclusions to be drawn.

CAATs FAQs

1. Computer application techniques and audit?

Computer application techniques to audit source software and tools are fed directly into those tools neglected by a target, especially in an integrated form, such as the analysis of financial data for fraud detection and compliance evaluation. Audit conducts this automated procedure with an end product, making it more efficient than a non-automated outcome for most outcomes.

2. How does an audit by a computer have to be?

CAATs extract trends about financial data from different sources and analyze it for irregularity fellows to look further into fraud, analyze risk, and assess compliance with financial regulations,” are the headlines of CAATs used by auditors.

3. What are the types of computer-assisted audit techniques?

Computer-assisted audit techniques include test data, parallel simulation, integrated test facilities, embedded audit modules, and data mining tools.

4. What are the benefits of computer-assisted audit techniques?

The benefits of computer-assisted audit techniques include speed of data analysis, improved fraud detection, real-time monitoring, and better compliance with financial regulations.

5. What are the limitations of computer-assisted audit techniques?

The limitations of computer-assisted audit techniques include high costs, technical complexities, data security risks, and system integration issues.